Nasdaq

Nasdaq 華爾街日報

華爾街日報Is It Too Late To Consider BeOne Medicines After Its 2025 Oncology Pipeline Surge?

- Wondering if BeOne Medicines is still a smart buy after its big run up, or if the easy money has already been made? Here is a closer look at what the current share price implies about its long term potential.

- The stock has been volatile lately, slipping 6.3% over the last month but still up 1.9% in the past week, and 69.4% year to date and 71.6% over the past year. This suggests the market is rapidly updating its view of the company.

- Recent headlines around BeOne Medicines have centered on progress in its oncology pipeline and growing interest from institutional investors, both of which have helped fuel that multi year share price performance. At the same time, concerns about the broader biotech funding environment have kept sentiment from getting too euphoric, adding nuance to the recent price swings.

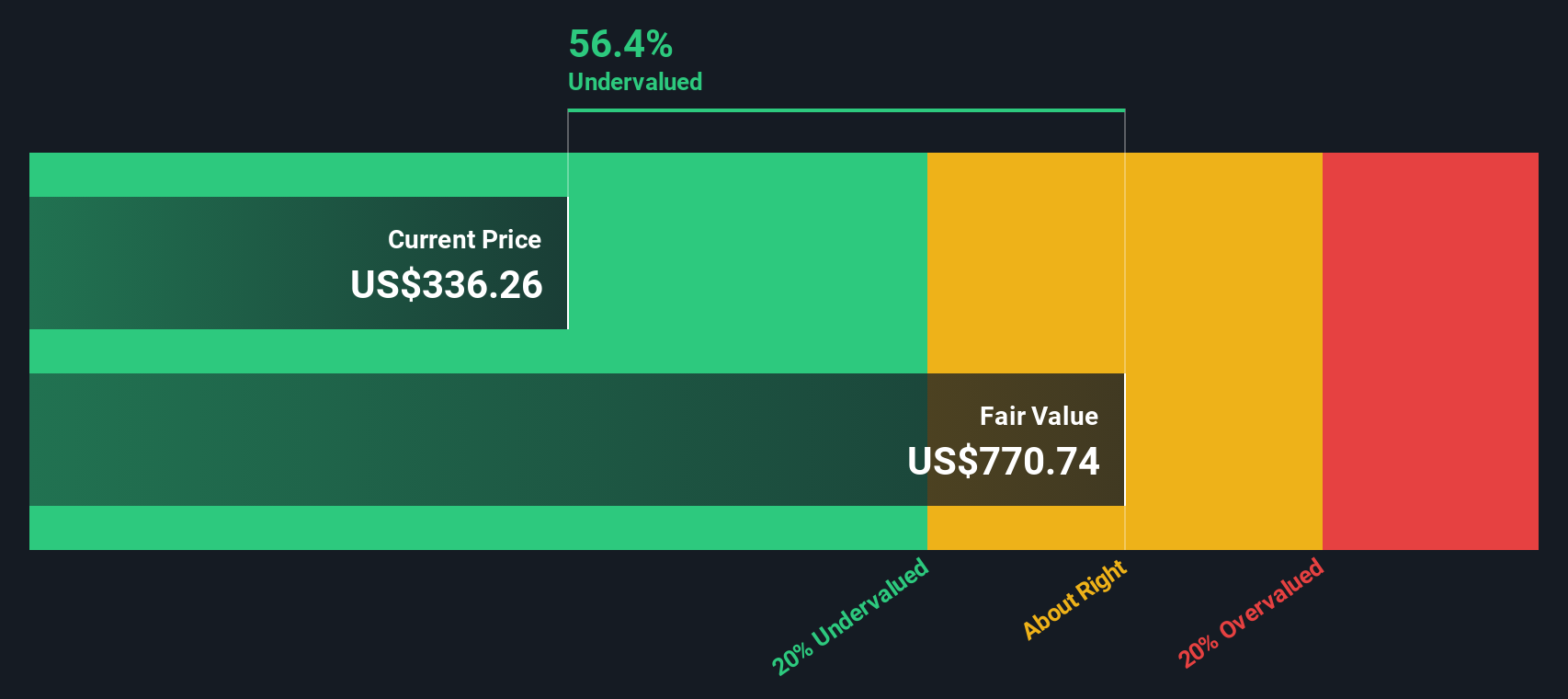

- Within that backdrop, BeOne Medicines currently scores a perfect 6 out of 6 on our valuation checks, pointing to potential undervaluation even after a big rally. Next we will unpack what different valuation approaches say about the stock while hinting at a more complete way to think about value by the end of this article.

Approach 1: BeOne Medicines Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and discounting those cash flows back to today in dollar terms.

For BeOne Medicines, the model starts with last twelve month Free Cash Flow of about $66.3 million and uses analyst forecasts and then Simply Wall St extrapolations to project growth. By 2029, Free Cash Flow is expected to reach roughly $2.3 billion, with further gains implied through 2035 as the oncology pipeline matures and scales.

Using a two-stage Free Cash Flow to Equity approach, these future cash flows are discounted back to arrive at an intrinsic value of about $740.01 per share. Compared with the current market price, this implies the shares are trading at a 57.9% discount to estimated fair value, which indicates potential upside if the cash flow trajectory is achieved.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests BeOne Medicines is undervalued by 57.9%. Track this in your watchlist or portfolio, or discover 904 more undervalued stocks based on cash flows.

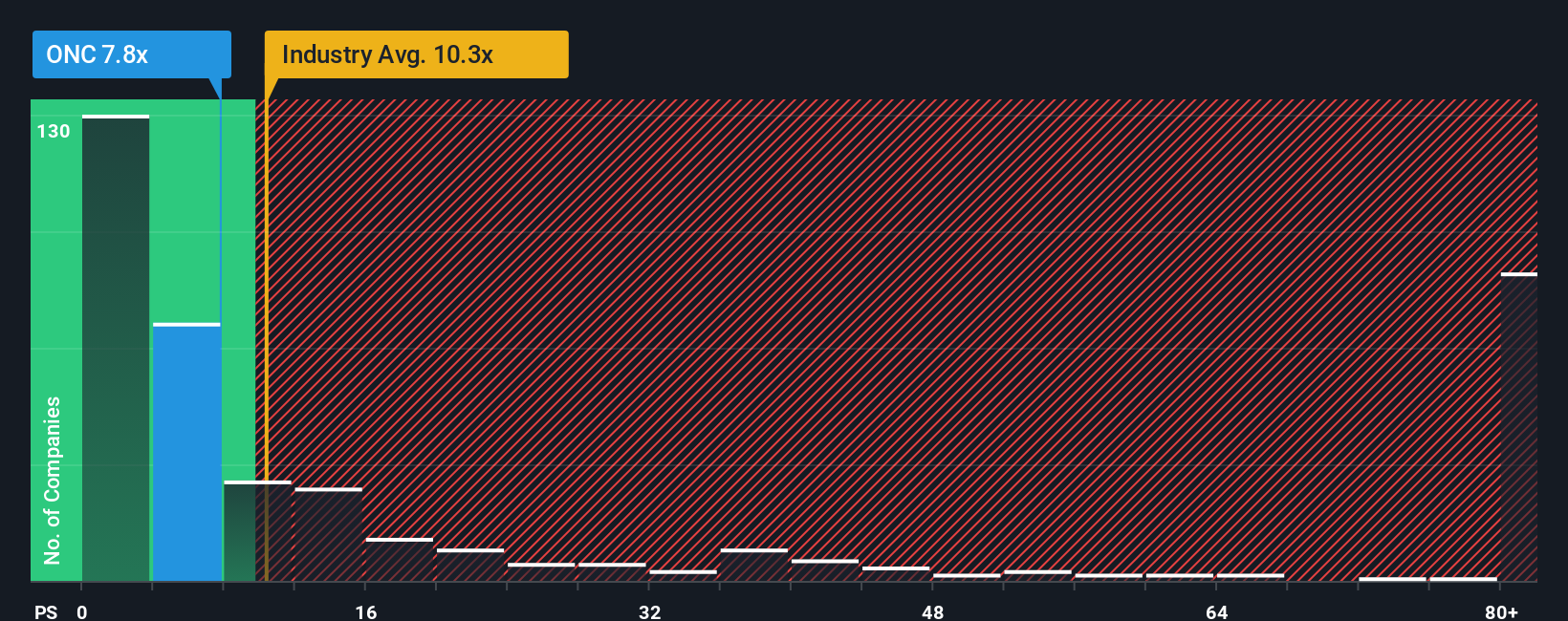

Approach 2: BeOne Medicines Price vs Sales

For profitable, growing biotechs like BeOne Medicines, the Price to Sales, or P S, ratio is a useful way to gauge how much investors are paying for each dollar of current revenue, especially when earnings are still being reinvested heavily back into the business.

In general, faster revenue growth and lower business risk justify a higher P S multiple, while slower growth or greater uncertainty should translate into a lower, more conservative multiple. Today BeOne Medicines trades on a P S ratio of about 6.94x. This is below both the broader Biotechs industry average of roughly 12.37x and the peer group average of around 20.16x. This suggests the market is not assigning a premium despite its strong narrative.

Simply Wall St’s Fair Ratio framework estimates what a more appropriate P S multiple should be, given BeOne Medicines specific growth outlook, risk profile, profit margins, industry positioning and market cap. That Fair Ratio comes out at about 10.73x, which is more tailored than a simple comparison with peers or sector averages. Since the Fair Ratio sits meaningfully above the current 6.94x, the shares appear undervalued on this metric as well.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1460 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your BeOne Medicines Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your story about BeOne Medicines with specific assumptions for its future revenue, earnings, margins and, ultimately, its fair value.

A Narrative on Simply Wall St is your own, clearly defined perspective on a company that links what you believe about its products, pipeline, competition and risks to a structured financial forecast, and then to an explicit estimate of fair value per share.

These Narratives live in the Community section of the Simply Wall St platform, where millions of investors can easily create, compare and refine different scenarios, then decide whether to buy, hold or sell by comparing each Narrative’s Fair Value with the current market price.

Narratives are dynamic, automatically updating as new earnings, trial results or regulatory news emerge. As a result, the fair value you see for BeOne Medicines can quickly shift from more cautious views closer to 250 dollars per share to optimistic perspectives closer to 563 dollars per share, reflecting how different investors weigh the same information in very different ways.

Do you think there's more to the story for BeOne Medicines? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com