Nasdaq

Nasdaq 華爾街日報

華爾街日報Is It Too Late To Consider Baidu After Its 49.2% Rebound In 2025?

- If you are wondering whether Baidu is still a bargain after its recent run, or if you have already missed the upside, this breakdown will walk through what the current price is actually implying about its future.

- After a strong rebound with shares up 3.2% over the last week, 3.5% over the past month, and a 49.2% gain year to date, investors are clearly rethinking Baidu's prospects despite a still negative 43.8% return over five years.

- Recent headlines have focused on Baidu's push to commercialize its Ernie AI ecosystem and deepen its role in China's autonomous driving and cloud infrastructure. This has helped shift sentiment toward a more growth oriented narrative. At the same time, ongoing regulatory scrutiny of Chinese tech and competition in AI and search continue to shape how much risk investors are willing to price in.

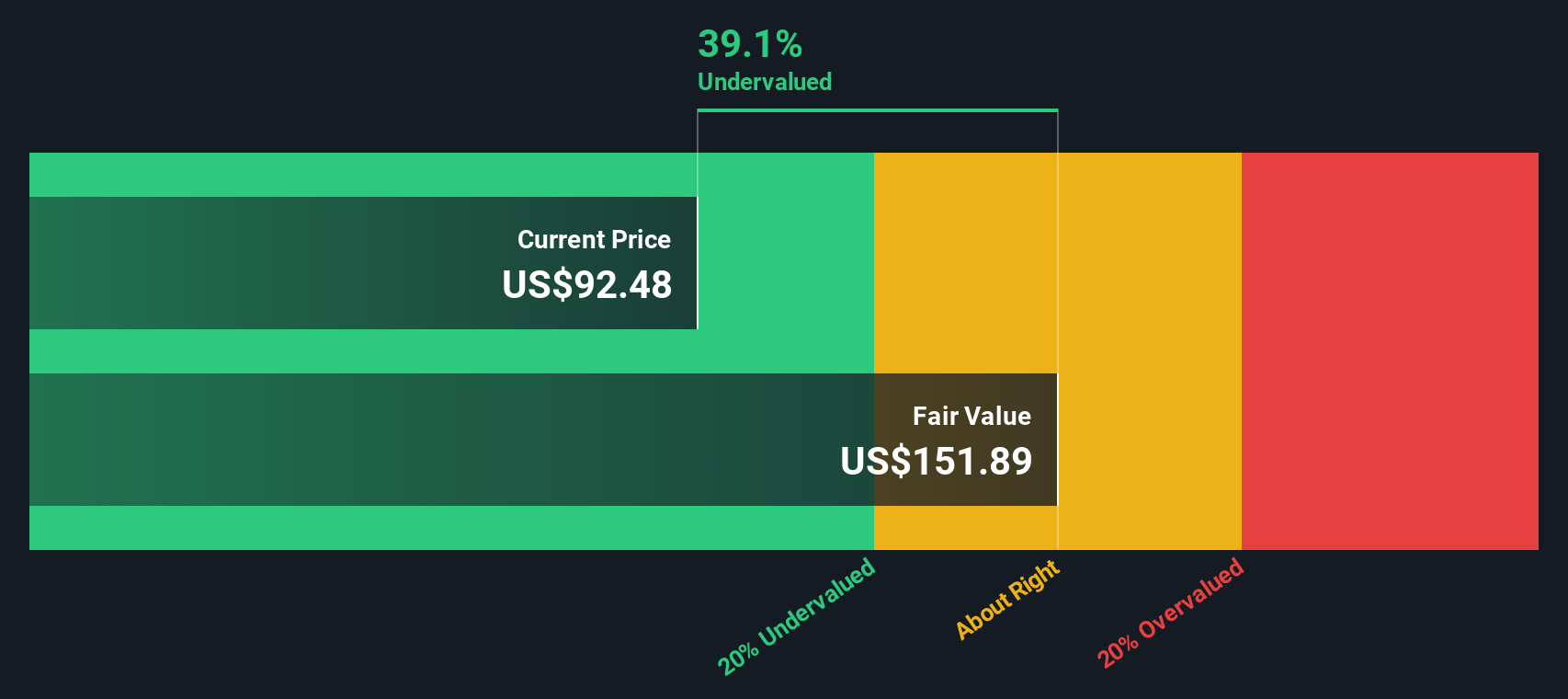

- Right now, Baidu scores just 1/6 on our valuation checks, suggesting that the market may not see it as obviously cheap. However, that headline number does not tell the full story. Next, we will unpack different valuation methods and then return at the end to a more intuitive way to think about what Baidu might really be worth.

Baidu scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Baidu Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and discounting those cash flows back to today.

For Baidu, the latest twelve month free cash flow is negative at about CN¥13.7 Billion, reflecting heavy investment and uneven cash generation. Analysts then forecast a rebound, with free cash flow expected to reach roughly CN¥18.3 Billion in 2035. Estimates out to five years come from analyst models. Later years are extrapolated by Simply Wall St to smooth growth as the business matures.

When all these projected cash flows are converted into today’s money, the DCF model arrives at an intrinsic value of about $100.52 per share. Compared with the current share price, this implies Baidu is roughly 22.7% overvalued on this cash flow view. This suggests the market is already pricing in a fairly optimistic recovery path.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Baidu may be overvalued by 22.7%. Discover 905 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Baidu Price vs Earnings

For profitable companies like Baidu, the price to earnings ratio is a useful snapshot of how much investors are willing to pay today for each dollar of current profits. It naturally blends expectations for future growth with perceived risk, since faster growing and safer businesses usually justify higher PE multiples.

Baidu currently trades on a PE of about 35.4x. That is more than double the broader Interactive Media and Services industry average of around 16.7x, but still at a discount to its higher growth peer group, which averages roughly 59.7x. To refine this further, Simply Wall St calculates a Fair Ratio, the PE that might reasonably be expected for Baidu given its specific mix of earnings growth, margins, size, industry and risk profile. For Baidu, that Fair Ratio is estimated at 32.8x.

This Fair Ratio is more informative than a simple comparison with peers or the industry, because it adjusts for Baidu’s own fundamentals and risk rather than assuming it should look like the average company. With the current PE of 35.4x sitting modestly above the 32.8x Fair Ratio, the stock screens as slightly overvalued on this metric.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1459 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Baidu Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework on Simply Wall St's Community page where you connect your view of Baidu's story with your assumptions for future revenue, earnings and margins. These then roll into a financial forecast, a fair value estimate and a clear buy or sell signal by comparing that fair value to today’s price. All of this automatically updates as new news or earnings land. For Baidu, one investor might build a bullish Narrative around rapid AI cloud adoption, global robotaxi scaling and a fair value closer to the upper analyst range near $146. A more cautious investor might focus on monetization delays, competitive pressure and regulatory risk and land nearer the low end around $71 instead. Yet both are using the same easy, dynamic tool to turn their story into numbers they can act on.

Do you think there's more to the story for Baidu? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com