Nasdaq

Nasdaq 華爾街日報

華爾街日報We Discuss Why InterCure Ltd.'s (TLV:INCR) CEO Compensation May Be Closely Reviewed

Key Insights

- InterCure's Annual General Meeting to take place on 30th of December

- Total pay for CEO Alex Rabinovich includes ₪732.0k salary

- The total compensation is similar to the average for the industry

- InterCure's three-year loss to shareholders was 70% while its EPS was down 92% over the past three years

The results at InterCure Ltd. (TLV:INCR) have been quite disappointing recently and CEO Alex Rabinovich bears some responsibility for this. At the upcoming AGM on 30th of December, shareholders can hear from the board including their plans for turning around performance. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. From our analysis, we think CEO compensation may need a review in light of the recent performance.

Check out our latest analysis for InterCure

How Does Total Compensation For Alex Rabinovich Compare With Other Companies In The Industry?

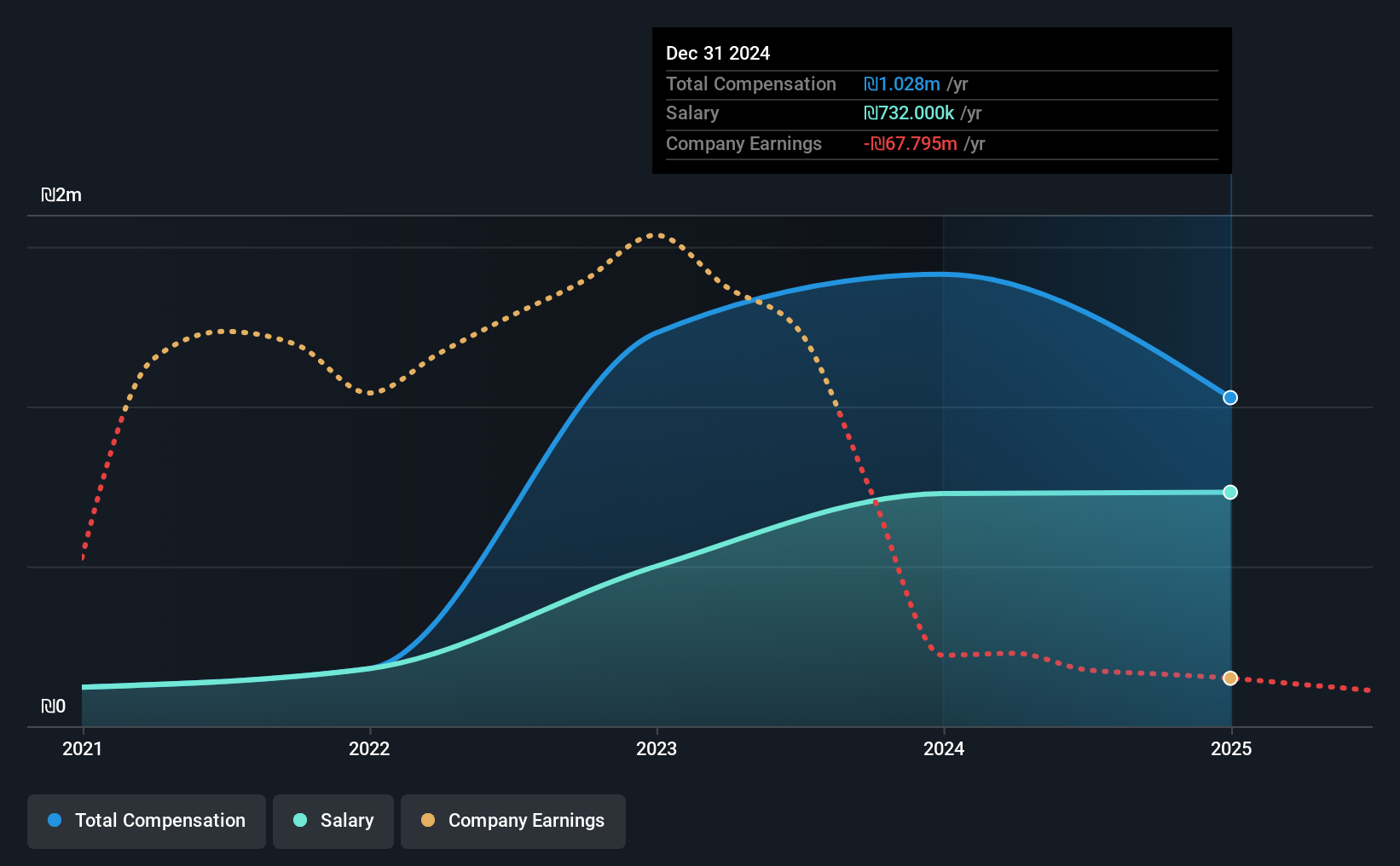

Our data indicates that InterCure Ltd. has a market capitalization of ₪209m, and total annual CEO compensation was reported as ₪1.0m for the year to December 2024. Notably, that's a decrease of 27% over the year before. In particular, the salary of ₪732.0k, makes up a huge portion of the total compensation being paid to the CEO.

On comparing similar-sized companies in the Israel Pharmaceuticals industry with market capitalizations below ₪637m, we found that the median total CEO compensation was ₪1.0m. This suggests that InterCure remunerates its CEO largely in line with the industry average. Moreover, Alex Rabinovich also holds ₪54m worth of InterCure stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | ₪732k | ₪728k | 71% |

| Other | ₪296k | ₪686k | 29% |

| Total Compensation | ₪1.0m | ₪1.4m | 100% |

On an industry level, roughly 71% of total compensation represents salary and 29% is other remuneration. InterCure is largely mirroring the industry average when it comes to the share a salary enjoys in overall compensation. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at InterCure Ltd.'s Growth Numbers

Over the last three years, InterCure Ltd. has shrunk its earnings per share by 92% per year. Its revenue is down 11% over the previous year.

The decline in EPS is a bit concerning. And the fact that revenue is down year on year arguably paints an ugly picture. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has InterCure Ltd. Been A Good Investment?

With a total shareholder return of -70% over three years, InterCure Ltd. shareholders would by and large be disappointed. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

In Summary...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, management will get a chance to explain how they plan to get the business back on track and address the concerns from investors.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. That's why we did our research, and identified 4 warning signs for InterCure (of which 1 shouldn't be ignored!) that you should know about in order to have a holistic understanding of the stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.