Nasdaq

Nasdaq 華爾街日報

華爾街日報Is Coterra Energy Now a Long Term Opportunity After Recent Share Price Weakness?

- If you are wondering whether Coterra Energy at around $25.52 is a bargain or a value trap, you are not alone. This stock sits right where many long term investors start to lean in.

- Despite being down around 2.9% over the last week, 0.9% over the past month, and 2.4% year to date, Coterra has still delivered roughly 9.8% over 1 year, 13.4% over 3 years, and 100.6% over 5 years. This pattern hints at cyclical swings on top of a solid long term uptrend.

- Recent moves have been shaped by shifting sentiment around commodity prices and policy headlines that keep volatility elevated across the energy space. At the same time, investors continue to weigh Coterra's disciplined capital returns and portfolio mix against broader concerns about long term fossil fuel demand and regulatory pressure.

- On our framework, Coterra scores a full 6 out of 6 on undervaluation checks. This makes it worth unpacking how different valuation methods line up today, and later, we will look at a more nuanced way to decide what that score really means for your own strategy.

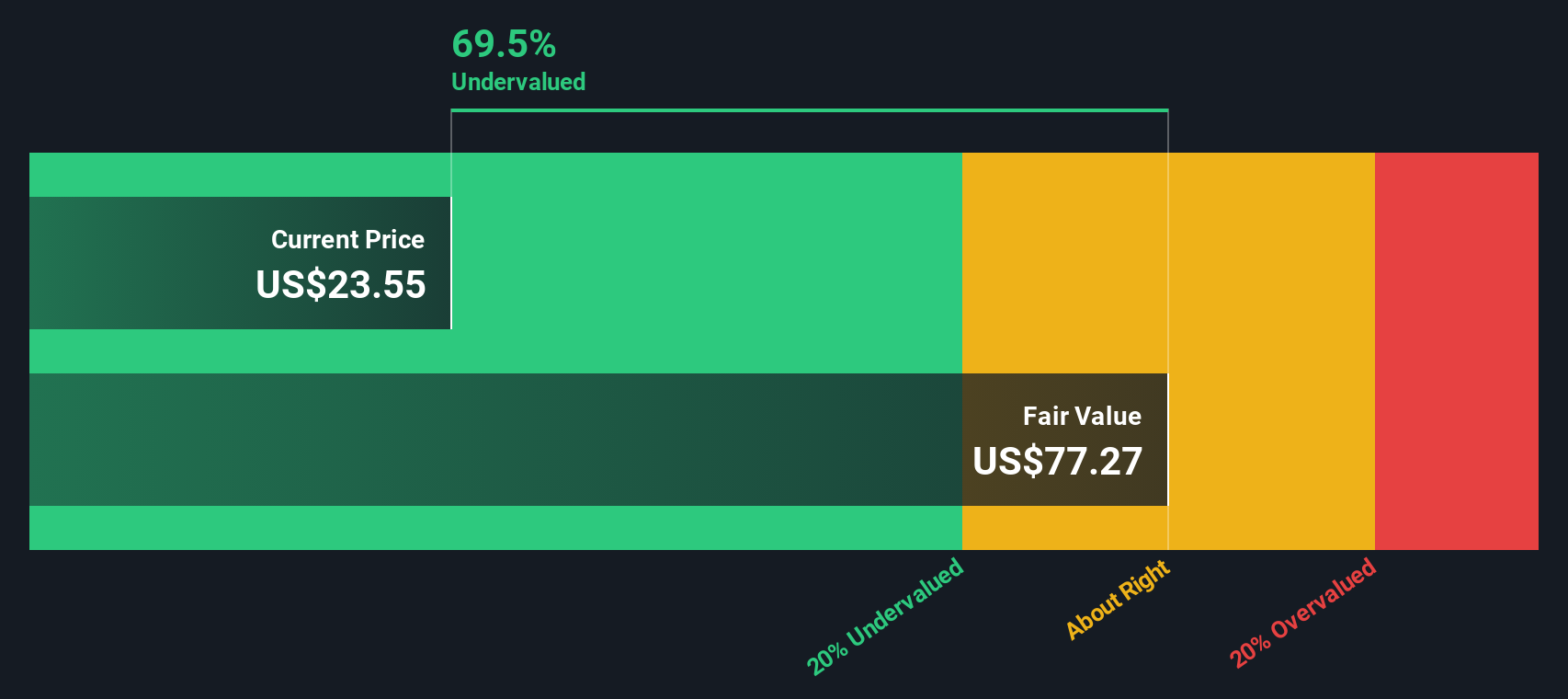

Approach 1: Coterra Energy Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth today by projecting its future cash flows and discounting them back to a present value. For Coterra Energy, the model used is a 2 Stage Free Cash Flow to Equity approach, focused on the cash available to shareholders.

Coterra generated trailing twelve month free cash flow of about $1.40 billion, and analyst projections, combined with extrapolations by Simply Wall St, indicate free cash flow could rise to around $3.88 billion by 2035. The path between now and then is not linear; however, the ten year curve of projections suggests expansion of the cash flow base as new projects and efficiencies come through.

When these projected cash flows are discounted back to today, the model produces an intrinsic value estimate of roughly $102.39 per share. Compared to the recent share price near $25.52, the DCF output indicates the stock may be about 75.1% undervalued, which would imply a wide margin of safety if the cash flow trajectory proves accurate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Coterra Energy is undervalued by 75.1%. Track this in your watchlist or portfolio, or discover 898 more undervalued stocks based on cash flows.

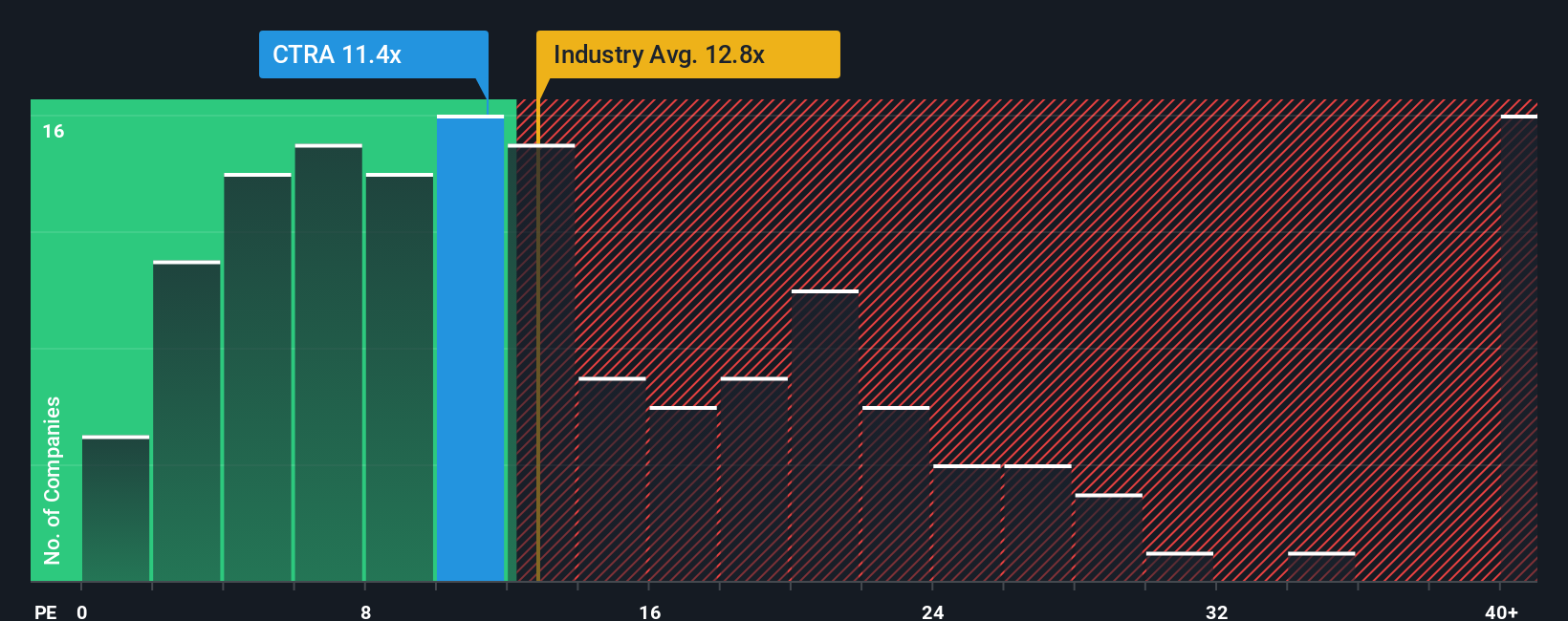

Approach 2: Coterra Energy Price vs Earnings

For profitable companies like Coterra, the price to earnings, or PE, ratio is a useful yardstick because it links what investors are paying directly to the earnings the business is already generating today. A higher PE can be justified when the market expects stronger growth or sees lower risk, while slower growth or higher uncertainty usually deserve a lower, more conservative PE.

Coterra currently trades on a PE of about 11.8x, slightly below the Oil and Gas industry average of roughly 12.9x and well below its broader peer group average of around 30.6x. At first glance, that discount might suggest the market is either underestimating Coterra's earnings power or pricing in more risk than for many peers.

Simply Wall St's Fair Ratio framework goes a step further by estimating what PE Coterra should trade on given its earnings growth outlook, profitability, industry position, market cap and specific risk profile. This produces a Fair PE Ratio of about 19.1x, which is more tailored than a simple comparison with peers or the sector, as it adjusts for Coterra's own fundamentals. With the current PE of 11.8x sitting notably below this 19.1x Fair Ratio, the multiple based view points to Coterra being undervalued.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1458 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Coterra Energy Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to attach your story about Coterra Energy to hard numbers like fair value, future revenue, earnings and margins, so that the company’s story flows into a financial forecast and then into a clear fair value estimate that you can easily compare with today’s share price to decide whether to buy, hold, or sell.

On Simply Wall St’s Community page, Narratives are an accessible tool used by millions of investors, updating dynamically as new information such as earnings or major news drops. This helps ensure your view of Coterra never goes stale and you can quickly see how the latest developments might shift your expected cash flows or risk profile and therefore your estimate of what the shares are really worth.

For example, one Coterra Narrative might lean on strong LNG contracts, high margin Permian projects and robust efficiency gains to support a fair value near the upper end of community views. Another, more cautious Narrative might emphasize natural gas price volatility, regulatory risk and inventory uncertainty to anchor a fair value close to the lower end. Both perspectives can coexist transparently so you can judge which story, and which number, fits your own outlook.

Do you think there's more to the story for Coterra Energy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com