Nasdaq

Nasdaq 華爾街日報

華爾街日報CITIC Construction Investment: Demand for high-speed optical modules continues to rise, and scale-up is expected to open up new market space

The Zhitong Finance App learned that CITIC Construction Investment Securities released a research report saying that with the rapid upgrading and iteration of GPUs and ASICs, computing power performance continues to improve, while demand for data transmission has also increased dramatically. In AI data centers, more and more customers tend to choose network hardware with greater bandwidth. The larger the bandwidth, the lower the cost per bit of transmission, lower power consumption, and smaller size. The high growth rate of 800G optical modules can already reflect AI's urgent need for bandwidth. In 2026, demand for 800G optical modules is expected to continue to grow rapidly, and the 1.6T shipment scale will also increase dramatically, and the development of 3.2T optical modules will officially begin. We continue to focus on recommending the optical module/optical device/optical chip sector. First, leading optical module companies; second, optical module companies that are expected to achieve market and customer breakthroughs; third, upstream optical chip/laser and optical device companies; and fourth, some companies that have entered this field through acquisitions.

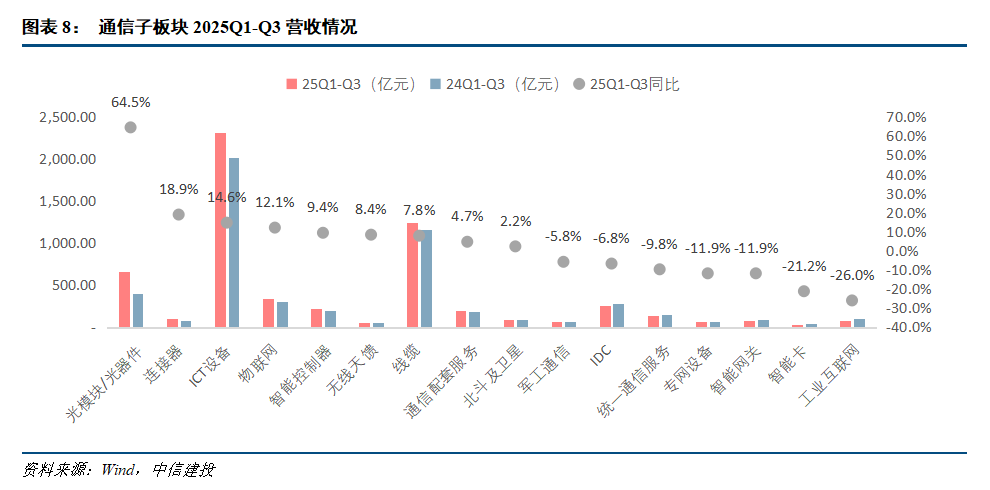

The optical module/optical device and connector sector had the best overall performance in the first three quarters of 2025

According to the CITIC Construction Investment Communications Team's division of the communications industry's various sub-sectors, the top three year-on-year revenue growth in 2025Q1-Q3 are: optical devices/optical modules (66.2 billion yuan, up 65% year on year), connectors (10 billion yuan, up 19% year on year), and ICT equipment (231.3 billion yuan, up 15% year on year), and ICT equipment (231.3 billion yuan, up 15% year over year), all driven by AI. The top three revenue growth rates for 2025Q1-Q3 are: industrial internet (7.8 billion yuan, down 26% year on year), smart cards (3.1 billion yuan, down 21% year on year), and smart gateway (8.3 billion yuan, down 12% year on year).

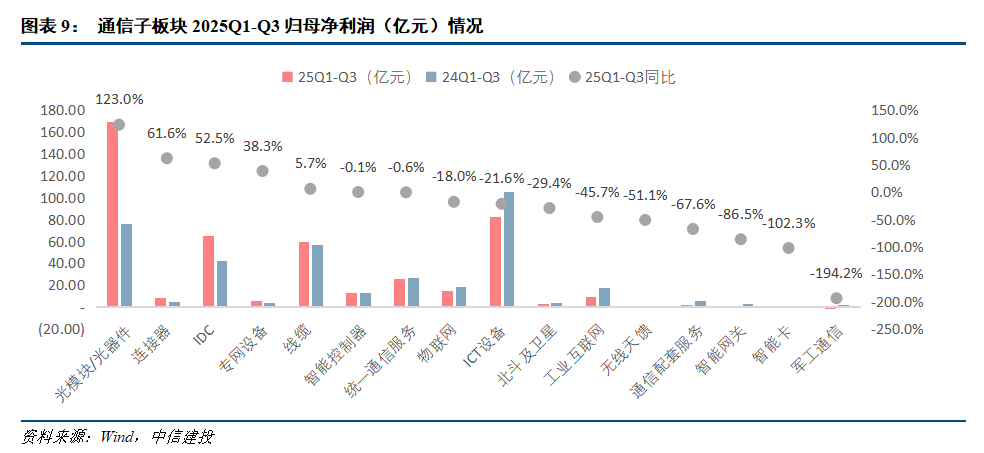

Among the various sub-sectors, the top three year-on-year net profit growth rates for 2025Q1-Q3 were: optical devices/optical modules (16.94 billion yuan, up 123% year on year), connectors (820 million yuan, up 62% year on year), and IDC (6.50 billion yuan, up 52% year on year. Overall, there are signs of improvement, which is also related to Runze Technology's large investment income). Net profit attributable to mother in 2025Q1-Q3 followed the year-on-year growth rate: military communications (-160 million yuan, down 194% year on year), smart cards (-0.02 billion yuan, down 102% year on year), and smart gateway (40 million yuan, down 86% year on year).

Among the net profit of the communications sub-sector in the first three quarters of 2025, optical devices/optical modules and connectors performed well. Mainly, demand for AI was strong, and demand for optical modules and copper cables increased significantly; military communications, smart cards, and smart gateway sectors declined significantly, mainly affected by cyclical fluctuations in downstream demand.

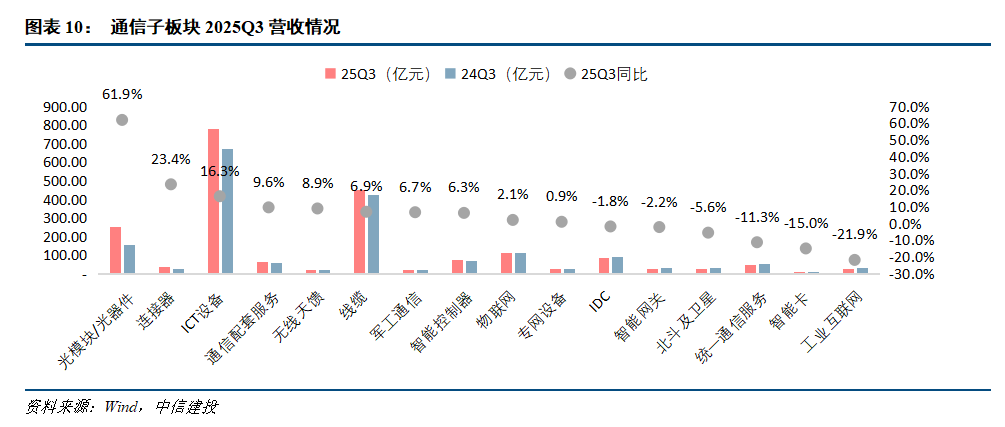

The top three sub-sectors with year-on-year revenue growth in 2025Q3 were: optical modules/optical devices (25.5 billion yuan, up 62% year on year), connectors (3.6 billion yuan, up 23% year on year), and ICT equipment (78.3 billion yuan, up 16% year on year). The top three revenue growth rates in 2025Q3 are: industrial Internet (2.5 billion yuan, down 22% year on year), smart cards (1 billion yuan, down 15% year on year), and unified communications services (4.6 billion yuan, down 11% year on year).

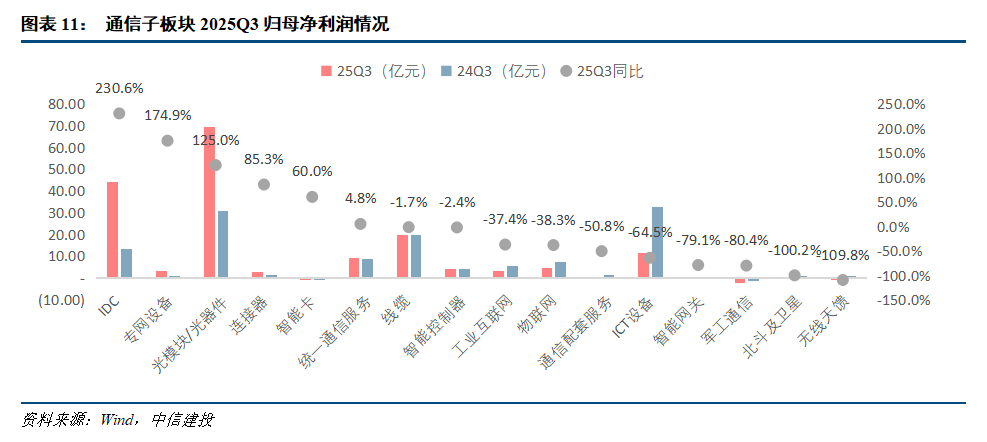

2025Q3, a sector with outstanding year-on-year net profit performance: IDC (4.43 billion yuan, up 231% year on year, related to Runze Technology's unusual increase), private network equipment (330 million yuan, up 175% year on year), and optical modules/optical devices (6.95 billion yuan, up 125% year on year). Net profit attributable to mother in 2025Q3 came in third place after the year-on-year growth rate: Wireless Tianfu (-0.04 billion yuan, down 110% year on year), Beidou and Satellite (-502 billion yuan, down 100% year on year), and military communications (-200 million yuan, down 80% year on year). The high growth rate in some areas is mainly related to the base figure. It is recommended to focus on the absolute value of revenue and profit at the same time.

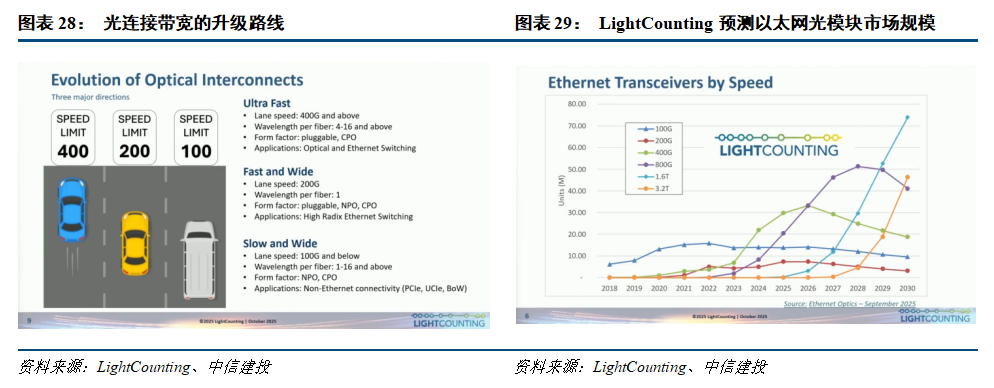

Optical modules: Demand for high-speed optical modules continues to rise, and scale-up is expected to open up new market space

With the rapid upgrading and iteration of GPUs and ASICs, computing power performance continues to improve, while demand for data transmission has also increased dramatically. In AI data centers, more and more customers tend to choose network hardware with greater bandwidth. The larger the bandwidth, the lower the cost per bit of transmission, lower power consumption, and smaller size. The high growth rate of 800G optical modules can already reflect AI's urgent need for bandwidth. CITIC Construction Investment Securities believes that in 2026, demand for 800G optical modules is expected to continue to grow rapidly, while the 1.6T shipment scale will also increase dramatically, and the development of 3.2T optical modules will officially begin.

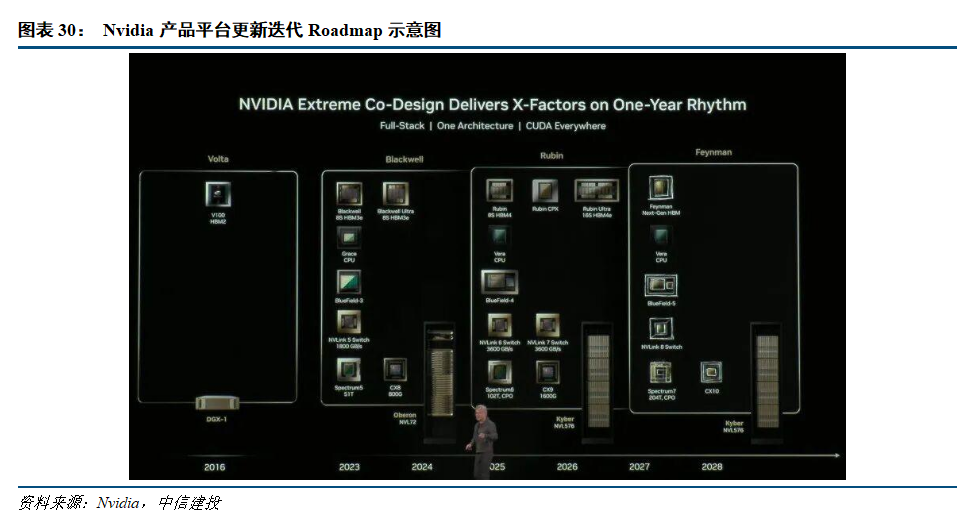

Judging from Nvidia's GPU roadmap, the company's product upgrade cycle has been reduced to a 1-year generation pace, while the speed and bandwidth are constantly increasing. From 2023-2024, the company launched the Blackwell platform with 1800Gb/s NVLink 5 switches, 800G CX8 network cards, and 51T Spectrum5 Ethernet switches; to 2025-2026, the Rubin platform with 3600Gb/s NVLink 6 and NVLink7 switches, 102T Spectrum 6 CPO switches, and 1600Gbps CX9 network cards; to 2027-2028 Feynman platform with NVLink8 switch, 204T Spectrum 7 CPO switch, and CX10 network card.

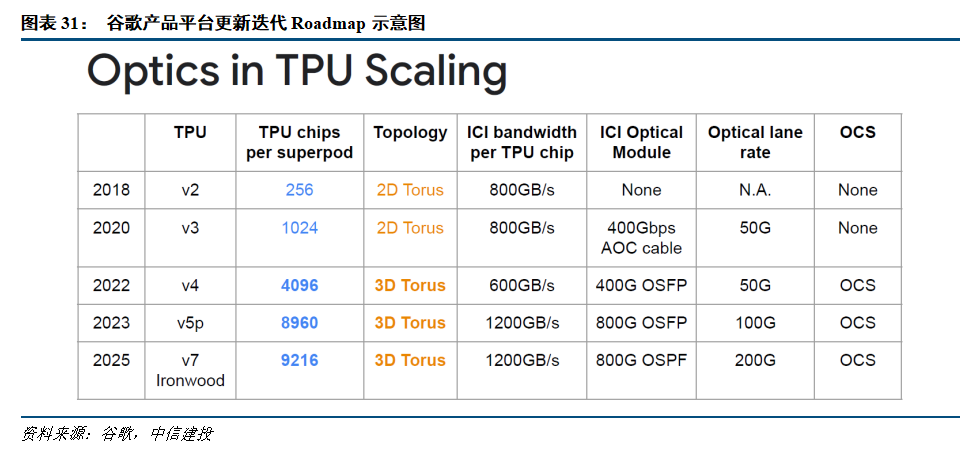

Judging from Google's TPU product evolution chart, ICI's bandwidth continued to grow from the V2 product in 2018 to the launch of the V7 Ironwood in 2025. The TPU V2 product uses a 2D Torus architecture. A single superpod has 256 chips, and the ICi bandwidth is 800Gb/s; the Ironwood chip uses the 3D Torus network topology, with an ICi bandwidth of 1200 Gb/s, and an 800G OSPF optical module. The single optical channel rate reaches 200Gbps, and is also connected through OCS.

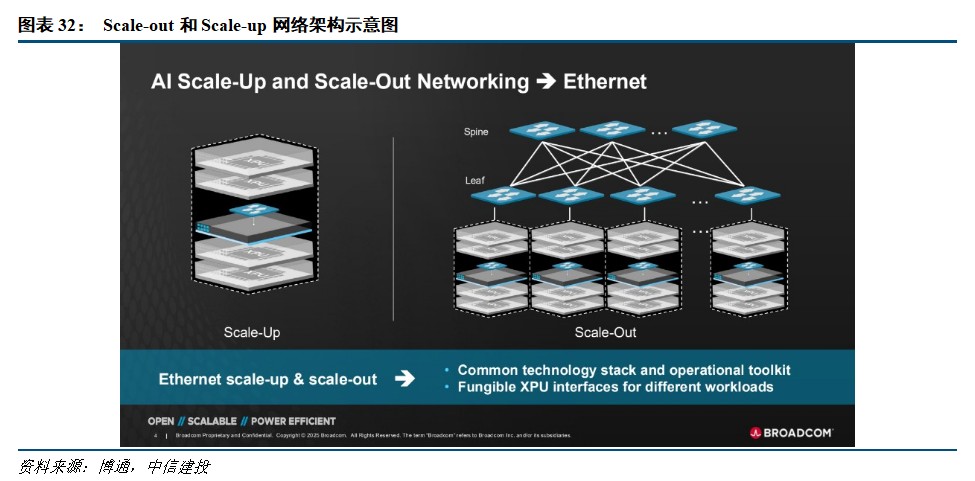

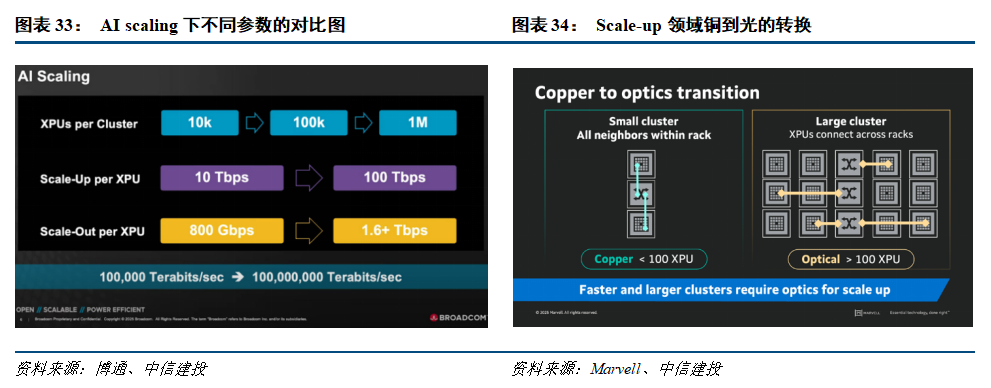

Currently, the main demand for optical modules in the industry comes from scale-out networks. Scale-out generally refers to horizontal scaling, that is, increasing the overall processing capacity by increasing the number of computing nodes to meet the challenges of high concurrency or large data volumes. Currently, most of the large clusters that have been built are over 10,000 cards, and can reach up to hundreds of thousands of cards, so the importance of scale-out is highlighted. In addition to scale-out networks, future optical module requirements for scale-up networks will be very broad. Scale-up generally refers to vertical scaling, that is, enhancing computing power by increasing the number of GPUs/XPUs in a single compute node. Initially, it was mainly an eight-card server product. As the scale-up domain gradually increased to 36/64/72, the single-node product model changed to a rack level.

Judging from the current XPU products in the industry, the scale-up bandwidth is significantly greater than the scale-out. Judging from the comparison of NV GPUs and ASIC technical parameters of various companies, the average scale-up bandwidth of an XPU is 10 Tbps, the scale-out bandwidth is 800 Gbps, and the bandwidth ratio of scale-up to scale-out is 12.5. According to the interview records of Broadcom CEO Hock, the company believes that the market space for scale-up is 5 to 10 times that of scale-out. CITIC Construction Investment Securities believes that this refers to network hardware, including switches, optical modules, copper cables, and PCBs. As a result, all sub-sectors of the network sector are expected to benefit.

As the scale-up domain gradually increases and the signal transmission bandwidth continues to increase, the transmission distance of electrical signals in metal media is greatly limited. At the same time, the transmission process also generates a large amount of heat, which consumes more power, affecting the performance of GPUs and switch chips. Therefore, optical interconnection is likely to become the mainstream solution in the scale-up field in the future, which can solve bottlenecks such as distance and bandwidth. In addition to solutions such as OIO for optical connectivity, Google, Meta, and Huawei have now begun using optical modules to build scale-up networks. Based on the analysis of mainstream network architectures in the industry, the demand for optical modules driven by scale-up is broad. Among them, Nvidia's Blackwell platform has a bandwidth of 7.2 Tbps, which is 9 times the scale-out bandwidth, so as the scale-up domain continues to expand, if a two-tier fat-tree architecture is used, the ratio of a single GPU to an 800G optical module will reach 1:36, and there is plenty of room for incremental growth.

Judging from the network architectures of overseas CSP manufacturers, if all optical modules are used in the scale-up field in the future, the market space is very large, which is probably 5-8 times the current one. For example, AMD's MI400 series products have scale-up and scale-out bandwidths above the industry average, and the optical module ratio is also high. CITIC Construction Investment Securities continues to focus on recommending the optical module/optical device/optical chip sector. First, leading optical module companies; second, optical module companies that are expected to achieve market and customer breakthroughs; third, upstream optical chip/laser and optical device companies; and fourth, some companies that have entered this field through acquisitions.