Nasdaq

Nasdaq 華爾街日報

華爾街日報Earnings Tell The Story For Asahi Intelligence Service Co., Ltd. (TSE:9799) As Its Stock Soars 26%

Asahi Intelligence Service Co., Ltd. (TSE:9799) shares have continued their recent momentum with a 26% gain in the last month alone. The last 30 days bring the annual gain to a very sharp 49%.

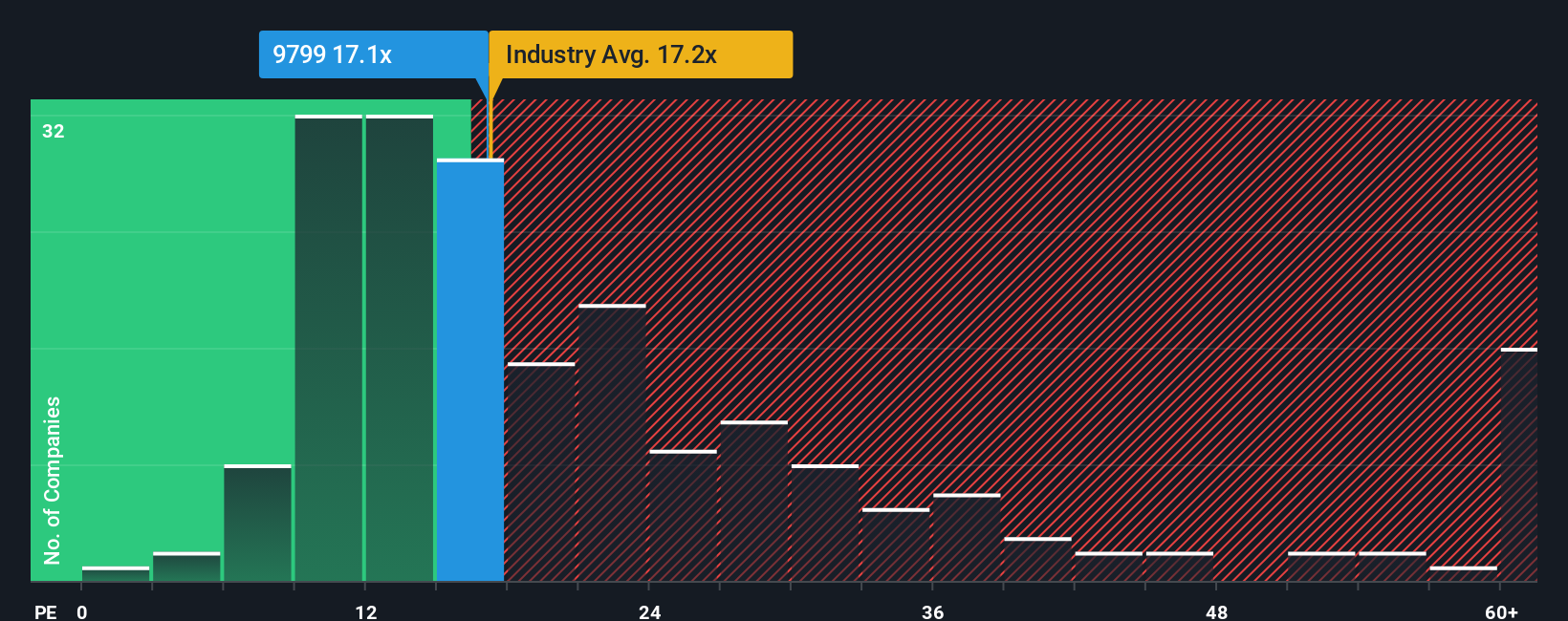

Following the firm bounce in price, Asahi Intelligence Service's price-to-earnings (or "P/E") ratio of 17.1x might make it look like a sell right now compared to the market in Japan, where around half of the companies have P/E ratios below 14x and even P/E's below 10x are quite common. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

For example, consider that Asahi Intelligence Service's financial performance has been poor lately as its earnings have been in decline. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Asahi Intelligence Service

Does Growth Match The High P/E?

In order to justify its P/E ratio, Asahi Intelligence Service would need to produce impressive growth in excess of the market.

Retrospectively, the last year delivered a frustrating 33% decrease to the company's bottom line. However, a few very strong years before that means that it was still able to grow EPS by an impressive 43% in total over the last three years. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 8.9% shows it's noticeably more attractive on an annualised basis.

In light of this, it's understandable that Asahi Intelligence Service's P/E sits above the majority of other companies. Presumably shareholders aren't keen to offload something they believe will continue to outmanoeuvre the bourse.

The Bottom Line On Asahi Intelligence Service's P/E

The large bounce in Asahi Intelligence Service's shares has lifted the company's P/E to a fairly high level. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Asahi Intelligence Service maintains its high P/E on the strength of its recent three-year growth being higher than the wider market forecast, as expected. Right now shareholders are comfortable with the P/E as they are quite confident earnings aren't under threat. Unless the recent medium-term conditions change, they will continue to provide strong support to the share price.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Asahi Intelligence Service with six simple checks.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.