Nasdaq

Nasdaq 華爾街日報

華爾街日報Is PETRONAS Chemicals Group Berhad (KLSE:PCHEM) A Risky Investment?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, PETRONAS Chemicals Group Berhad (KLSE:PCHEM) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

What Is PETRONAS Chemicals Group Berhad's Debt?

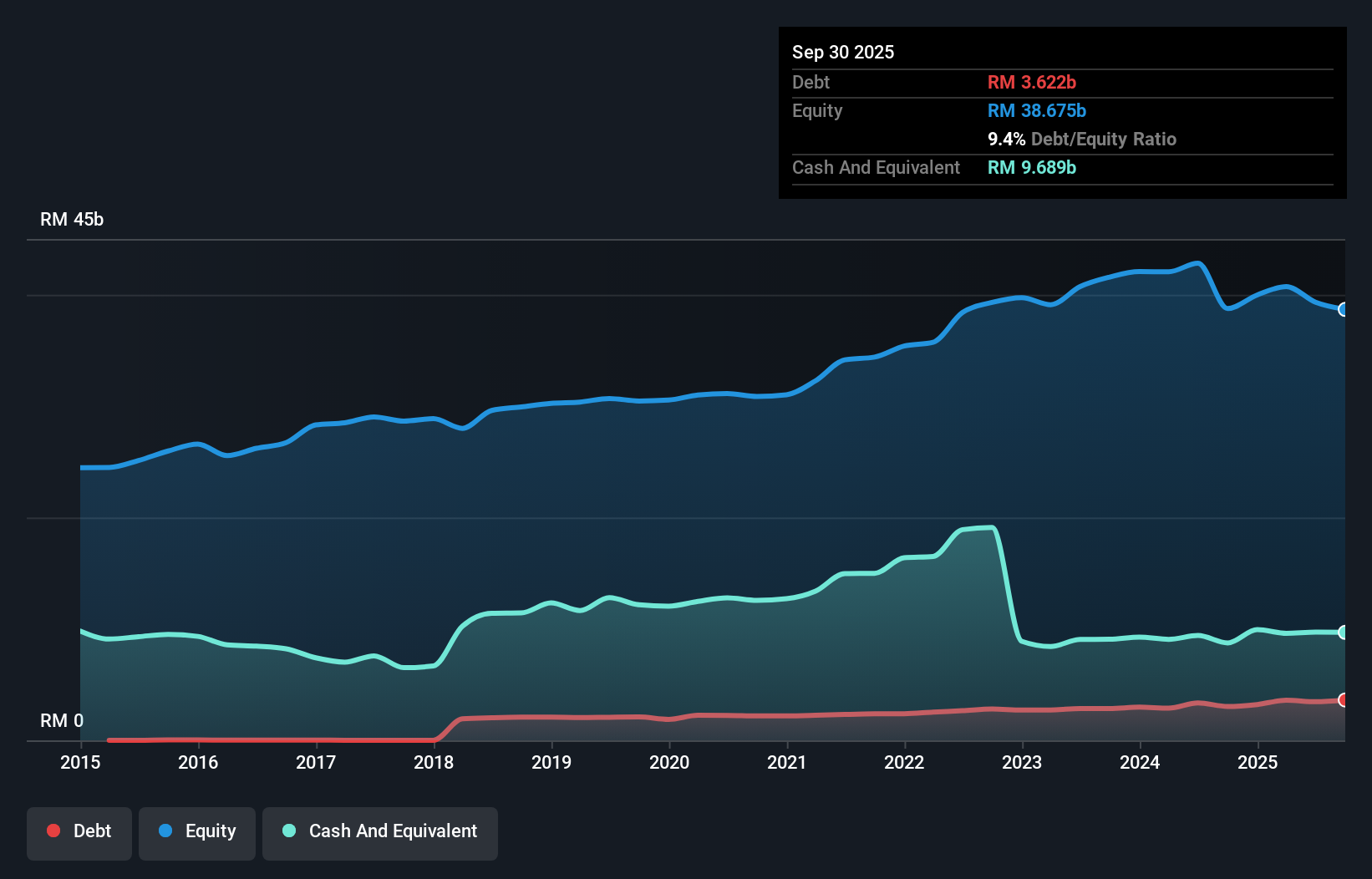

You can click the graphic below for the historical numbers, but it shows that as of September 2025 PETRONAS Chemicals Group Berhad had RM3.62b of debt, an increase on RM3.04b, over one year. However, its balance sheet shows it holds RM9.69b in cash, so it actually has RM6.07b net cash.

How Strong Is PETRONAS Chemicals Group Berhad's Balance Sheet?

The latest balance sheet data shows that PETRONAS Chemicals Group Berhad had liabilities of RM11.7b due within a year, and liabilities of RM8.55b falling due after that. Offsetting this, it had RM9.69b in cash and RM4.23b in receivables that were due within 12 months. So its liabilities total RM6.37b more than the combination of its cash and short-term receivables.

PETRONAS Chemicals Group Berhad has a market capitalization of RM28.5b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. Despite its noteworthy liabilities, PETRONAS Chemicals Group Berhad boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if PETRONAS Chemicals Group Berhad can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

See our latest analysis for PETRONAS Chemicals Group Berhad

In the last year PETRONAS Chemicals Group Berhad had a loss before interest and tax, and actually shrunk its revenue by 6.9%, to RM28b. That's not what we would hope to see.

So How Risky Is PETRONAS Chemicals Group Berhad?

While PETRONAS Chemicals Group Berhad lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow RM1.5b. So taking that on face value, and considering the net cash situation, we don't think that the stock is too risky in the near term. Until we see some positive EBIT, we're a bit cautious of the stock, not least because of the rather modest revenue growth. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 1 warning sign for PETRONAS Chemicals Group Berhad you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.