Nasdaq

Nasdaq 華爾街日報

華爾街日報Earnings Not Telling The Story For Sundaram Finance Limited (NSE:SUNDARMFIN)

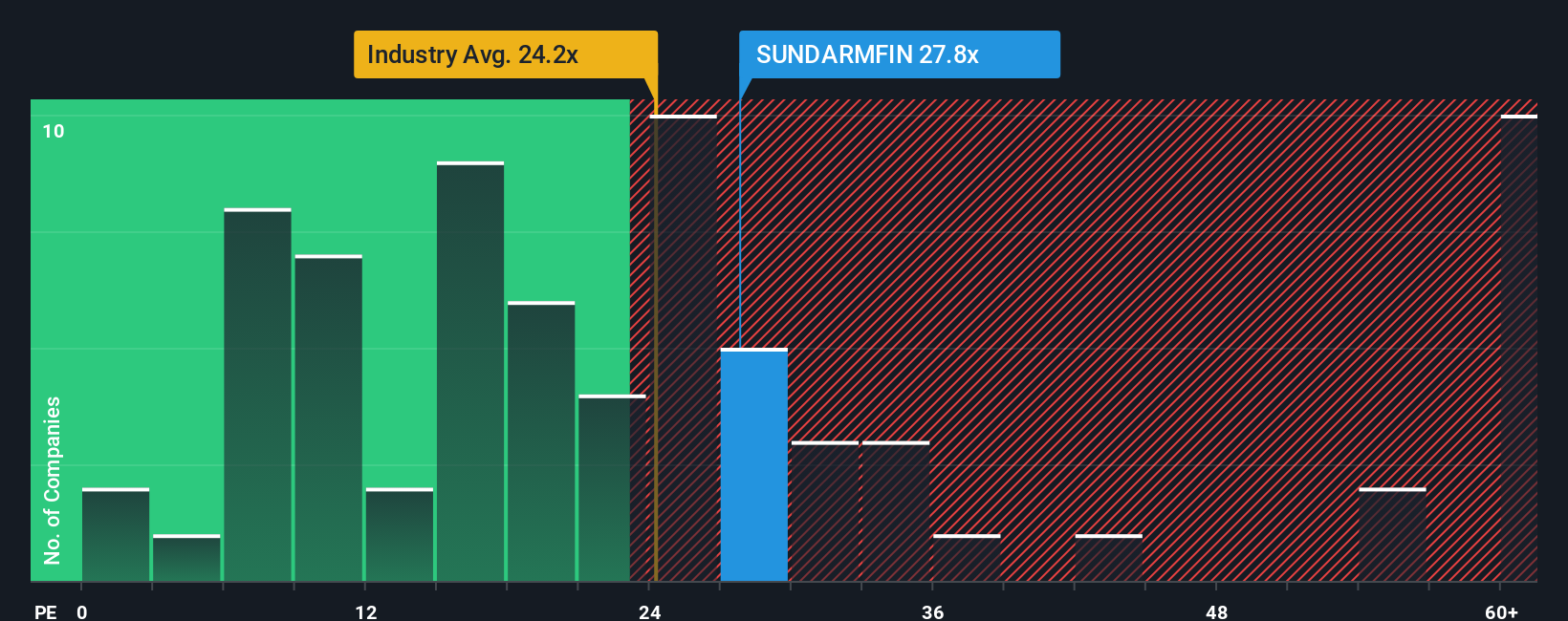

There wouldn't be many who think Sundaram Finance Limited's (NSE:SUNDARMFIN) price-to-earnings (or "P/E") ratio of 27.8x is worth a mention when the median P/E in India is similar at about 25x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Recent times have been advantageous for Sundaram Finance as its earnings have been rising faster than most other companies. It might be that many expect the strong earnings performance to wane, which has kept the P/E from rising. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

View our latest analysis for Sundaram Finance

Does Growth Match The P/E?

The only time you'd be comfortable seeing a P/E like Sundaram Finance's is when the company's growth is tracking the market closely.

Retrospectively, the last year delivered an exceptional 26% gain to the company's bottom line. The latest three year period has also seen an excellent 66% overall rise in EPS, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 12% each year during the coming three years according to the nine analysts following the company. Meanwhile, the rest of the market is forecast to expand by 20% each year, which is noticeably more attractive.

In light of this, it's curious that Sundaram Finance's P/E sits in line with the majority of other companies. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Final Word

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Sundaram Finance currently trades on a higher than expected P/E since its forecast growth is lower than the wider market. Right now we are uncomfortable with the P/E as the predicted future earnings aren't likely to support a more positive sentiment for long. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

There are also other vital risk factors to consider and we've discovered 2 warning signs for Sundaram Finance (1 doesn't sit too well with us!) that you should be aware of before investing here.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.