Nasdaq

Nasdaq 華爾街日報

華爾街日報Will ATI’s New CFO Shape a Different Balance Between Growth and Discipline for ATI (ATI)?

- Earlier this month, ATI Inc. announced that longtime finance leader James Robert "Rob" Foster will become Senior Vice President, Finance and Chief Financial Officer on January 1, 2026, succeeding current CFO Don Newman, who will transition to a strategic advisory role before his planned retirement in March 2026.

- Foster’s blend of deep operational experience in specialty alloys and prior leadership of ATI’s global finance, capital deployment, and supply chain functions positions him to directly influence how the company balances growth investments with financial discipline.

- We’ll now examine how Foster’s combination of operational and finance experience may influence ATI’s investment narrative and forward-looking risk-reward profile.

Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

ATI Investment Narrative Recap

To own ATI, you generally need to believe in its role as a key supplier of advanced alloys to commercial aerospace, defense, and energy, while managing capital intensive growth and concentrated OEM exposure. The Rob Foster CFO appointment looks incremental rather than transformational in the short term, so it does not materially change the near term focus on executing long term aerospace contracts versus the ongoing risk of heavy capex and balance sheet pressure.

Among recent developments, ATI’s June 2025 refinancing that put a US$200,000,000 term loan and US$600,000,000 revolving facility in place stands out in light of Foster’s new role. His background overseeing capital projects and supply chain ties directly into how ATI uses this expanded liquidity to fund capacity investments and efficiency gains, which feeds back into both its growth catalysts in aerospace and the risk of elevated leverage if returns on these projects fall short.

But against that backdrop of strong aerospace demand, investors should still be alert to how ATI’s ongoing capital expenditure needs could...

Read the full narrative on ATI (it's free!)

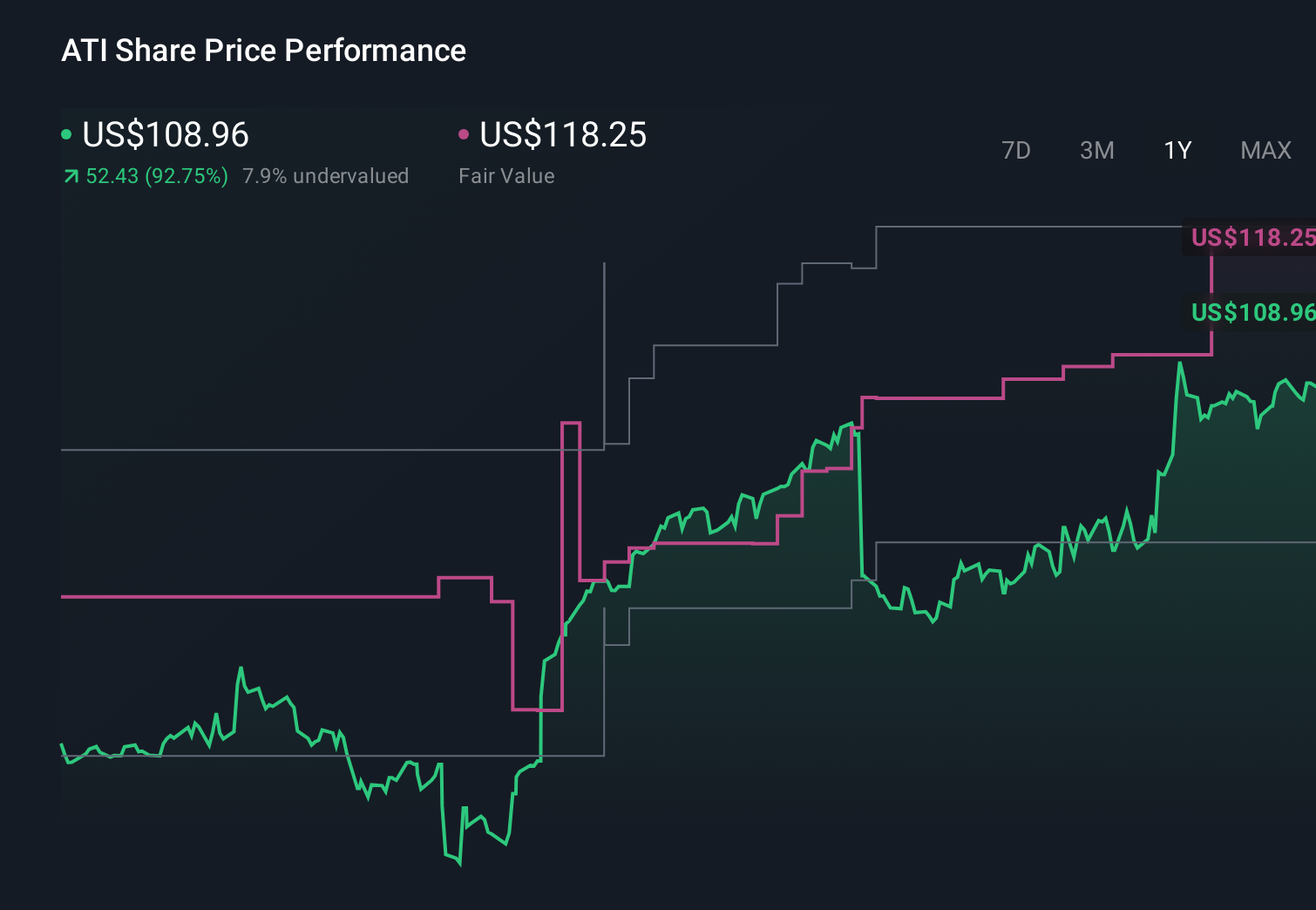

ATI's narrative projects $5.5 billion revenue and $635.6 million earnings by 2028.

Uncover how ATI's forecasts yield a $118.25 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community currently value ATI between US$62.68 and US$118.25 per share, reflecting a wide spread of expectations. When you weigh those views against ATI’s dependence on large aerospace OEMs and capital heavy growth, it becomes clear why examining several alternative viewpoints on the company’s prospects is so important.

Explore 5 other fair value estimates on ATI - why the stock might be worth as much as $118.25!

Build Your Own ATI Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your ATI research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free ATI research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ATI's overall financial health at a glance.

Looking For Alternative Opportunities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Rare earth metals are the new gold rush. Find out which 34 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com