Nasdaq

Nasdaq 華爾街日報

華爾街日報Is It Too Late To Consider Invesco After Its 53% Year To Date Surge?

- If you are wondering whether Invesco is still a smart buy after its big run or if you are showing up late to the party, this breakdown will help you assess whether the current price really makes sense.

- The stock has climbed 2.8% over the last week, 17.8% in the past month, and is now up 53.0% year to date and 62.7% over the last year, with longer term gains of 69.4% over 3 years and 88.8% over 5 years reshaping how investors view its risk and reward profile.

- Much of this move reflects shifting sentiment across the asset management space, as investors reassess which players are best positioned if markets stay resilient and cash continues to flow back into funds. At the same time, ongoing debates around fees, passive versus active products, and competitive pressure from low cost giants are limiting how optimistic the market is willing to be about Invesco.

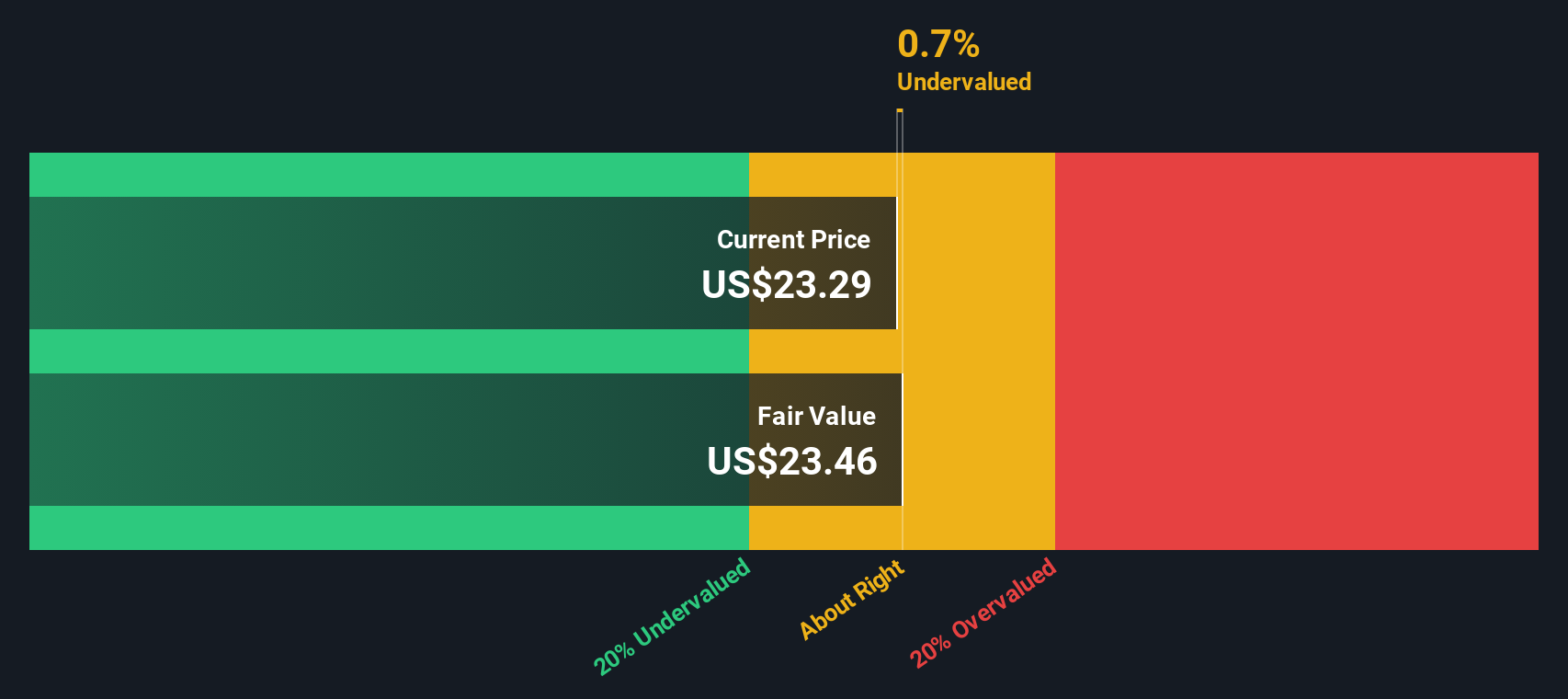

- Despite the strong share price performance, Invesco only scores a 2/6 valuation check score, suggesting it screens as undervalued on just a couple of metrics. Next, we will unpack those traditional valuation approaches and, by the end, explore a more holistic way to think about what this business may be worth.

Invesco scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Invesco Excess Returns Analysis

The Excess Returns model asks whether Invesco is earning enough on shareholder capital, after its cost of equity, to justify the current share price. It compares the return generated on the company’s equity base with what investors demand as compensation for risk.

For Invesco, the starting point is a Book Value of $24.70 per share and a Stable EPS estimate of $1.81 per share, based on the median return on equity from the past 5 years. Against this, the Cost of Equity is $3.02 per share, which implies an Excess Return of -$1.22 per share, meaning projected earnings fall short of the required return. The model also uses a Stable Book Value of $35.92 per share, derived from weighted future Book Value estimates from two analysts, alongside an Average Return on Equity of 5.03%.

When these inputs are combined, the Excess Returns framework arrives at an intrinsic value that is 119.1% below the current share price, implying the stock is materially overvalued on this basis.

Result: OVERVALUED

Our Excess Returns analysis suggests Invesco may be overvalued by 119.1%. Discover 912 undervalued stocks or create your own screener to find better value opportunities.

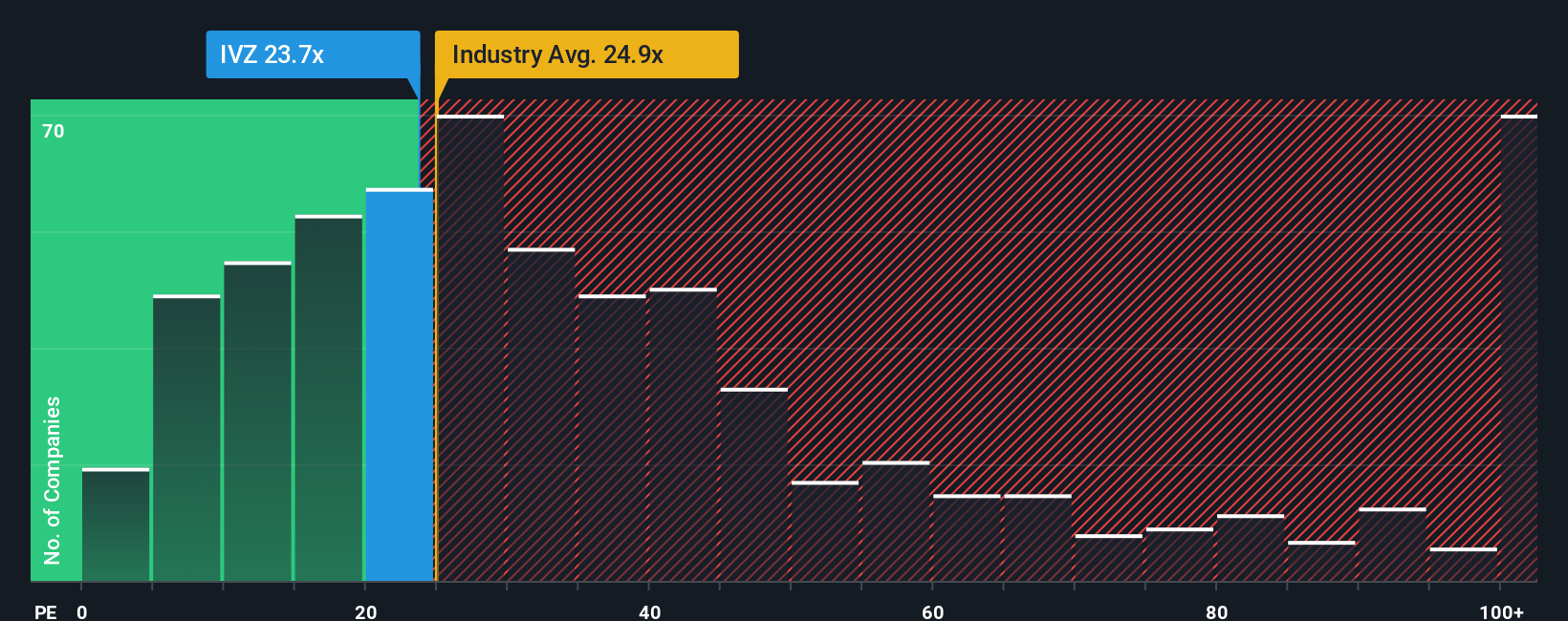

Approach 2: Invesco Price vs Earnings

For a profitable company like Invesco, the price to earnings, or PE, multiple is a useful way to gauge whether investors are paying a reasonable price for each dollar of earnings. In general, faster growth and lower risk justify a higher PE, while slower growth, more cyclical earnings or higher risk usually warrant a lower, more conservative multiple.

Invesco currently trades on a PE of 18.0x, which is slightly above the Capital Markets peer average of 17.3x, but well below the broader industry average of 25.1x. To move beyond simple comparisons, Simply Wall St calculates a “Fair Ratio” of 19.2x for Invesco, which reflects what investors might reasonably pay given its earnings growth outlook, profitability, size and risk profile.

This Fair Ratio is more informative than a basic peer or industry comparison because it adjusts for company specific drivers such as growth, risks, profit margin, industry dynamics and market cap, rather than assuming all firms deserve the same multiple. With the current PE of 18.0x sitting below the Fair Ratio of 19.2x, the shares appear modestly undervalued on this earnings based lens.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1463 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Invesco Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. These are simple stories you build around a company that connect your view of its future (revenue, earnings and margins) to a financial forecast and then to a fair value. All of this happens within an easy tool on Simply Wall St’s Community page that millions of investors use to compare their own fair value to the current price, see how their buy or sell decision stacks up against others, and watch that view update dynamically as new news or earnings land. For example, one Invesco narrative might lean bullish and land near the higher fair value of about $29.00 by assuming successful ETF growth, margin leverage and QQQ restructuring. A more cautious investor could anchor closer to the lower end near $17.00 by stressing fee pressure, competition and execution risk. Narratives make these differing perspectives transparent, quantified and directly comparable to today’s share price.

Do you think there's more to the story for Invesco? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com