Nasdaq

Nasdaq 華爾街日報

華爾街日報Is Sherwin-Williams Still a Buy After Its 115,000% Run?

Key Points

The paint company has a storied history, but it's now facing a "very challenging environment."

It grew earnings and revenue by 3.3% and 3.2% year over year last quarter, respectively.

The company's most recent dividend hike, its 47th in as many years, points to a solid outlook.

In the second quarter of its fiscal 1965, just after its initial public offering the year before, paint maker Sherwin-Williams (NYSE: SHW) reported net income of $1.06 million. Sixty years later, in Q2 2025, it reported net income of $754.7 million. Even when you account for the inflation seen in that time, that's a roughly 7,200% rise in net income.

Yet, Sherwin-Williams shares have risen far faster, notching 115,000% gains since 1985, the first year its share price data is readily available. What explains the stratospheric gains of a paint-maker stock over the last 40 years?

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Part of it is its sterling dividend history, as it has increased its dividend for 47 years and counting. But the main reason is share buybacks. The company has aggressively repurchased shares over the years, an inherently shareholder-friendly practice that boosts earnings per share and ultimately share price. In the last decade alone, Sherwin-Williams has bought back over 53 million shares, which is over 20% of the shares left outstanding.

Still, Sherwin-Williams shares are down about 4% year to date amid the S&P 500's 15% rise, and in last October's earnings call, CEO Heidi Petz acknowledged "a very challenging environment will persist through the first half of the year and most likely beyond that." This admission followed news in September that the company was temporarily halting its 401(k) match for employees.

Given all that, should investors avoid Sherwin-Williams despite its storied history? Here's what the numbers tell us.

Awaiting the "magic 6% number"

Sherwin-Williams is in a cyclical business. People can put off buying that coat of paint when they're feeling pinched, and a slower housing market with falling construction further dampens demand. America's souring economic mood, combined with flat home sales nationwide, has caused the "very challenging environment" Petz alluded to.

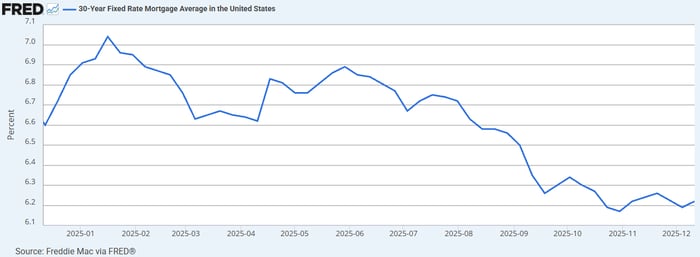

The good news is that interest rates are falling, and so is the 30-year fixed rate mortgage average. In her earnings call, Petz was asked how much farther it needs to fall to catalyze demand in Sherwin-Williams' Paint Stores segment. Petz replied that "6% seems to be the magic number," adding, "we are all hoping that the Fed makes some shifts here in the future."

As you can see, the 30-year fixed mortgage average is hovering tantalizingly close to the "magic number." With the Federal Reserve's announcement of a third rate cut earlier this month, it would likely take just another 25-basis point cut to bring it below the 6% threshold that Petz laid out.

Data source: Freddie Mac via FRED®

The next Federal Open Monetary Committee meeting, in which the Federal Reserve announces its next decision on interest rates, is scheduled for this coming Jan. 27-28. So Sherwin-Williams will have to wait five more weeks for more interest rate relief, if the Fed indeed does cut.

But it seems clear that it will. November's jobs report showing only 64,000 jobs added for the month should cement Fed Chair Jerome Powell's fear that the labor market is in need of some juice. That's doubly true since Powell has openly theorized that, as bad as recent jobs numbers have been, they may actually be overstating jobs added by as much as 60,000 a month.

It will take some time for lower rates to be felt in Sherwin-Williams' balance sheet, of course. In the meantime, these medium-to-high interest rates and flat housing market put last quarter's earnings and revenue growth of 3.3% and 3.2% in context.

Image source: Getty Images.

As for the pause on the 401(k) match, it sounds like an ominous sign at first. But there is precedent for the move, with Sherwin-Williams pausing its 401(k) match during the 2009 financial crisis and again during the COVID-19 pandemic. The company's shares are up more than 1,700% since mid-2009, to give you an idea of what the 401(k) policy says about the stock.

Dividends don't lie

Sherwin-Williams is on the cusp of a milestone only one in 1,000 companies have achieved: Dividend King status. Out of around 53,000 publicly traded companies in the world, just 55 have raised their dividend each year for 50 years. Sherwin-Williams just capped its 47th dividend hike, and the increase wasn't token, either. Its 10.5% dividend increase was just the latest in a string of robust hikes. Over the last five years, it's raised its dividend by 44%.

The current dividend yield of 1% may not be life-changing. But management will certainly covet Dividend King status, and I believe they won't be content to cross the finish line with nominal increases that lag inflation. This company's record of dividend growth is strong enough that a 1% yield could compound in a hurry.

Sherwin-Williams' rough patch might last for six months or longer, as its CEO has stated. But I believe this is a stock to hold for decades.

William Dahl has no position in any of the stocks mentioned. The Motley Fool recommends Sherwin-Williams. The Motley Fool has a disclosure policy.