Nasdaq

Nasdaq 華爾街日報

華爾街日報Will Preserved 10% Utility Returns in California Change Sempra's (SRE) Investment Narrative?

- Earlier in 2025, the California Public Utilities Commission voted 4–1 to let San Diego Gas & Electric and Southern California Gas, owned by Sempra, keep allowed profit margins around 10% for 2026, despite pressure from consumer advocates for much lower levels.

- This decision shores up visibility on future returns for Sempra’s California utilities while highlighting ongoing political tension over energy affordability and utility profitability.

- We’ll now examine how securing roughly 10% allowed returns in California could influence Sempra’s broader investment narrative and future earnings profile.

Find companies with promising cash flow potential yet trading below their fair value.

Sempra Investment Narrative Recap

To own Sempra, you need to be comfortable with a regulated utility story that leans heavily on predictable returns from California and Texas, plus LNG growth. The CPUC decision to keep allowed returns near 10% materially supports Sempra’s near term earnings visibility in California, while the biggest risk remains potential future regulatory or legislative shifts that could again revisit those allowed returns or impose new affordability constraints.

Alongside this decision, Sempra’s recent reaffirmation of its long term earnings growth targets through 2029 connects directly to the same theme: a growing regulated rate base and LNG cash flows funding dividend stability and capital plans. How well California regulators continue to balance customer costs with utility profitability will be crucial to whether those growth ambitions and capital recycling efforts translate into the earnings profile shareholders expect.

But while the decision supports Sempra’s current earnings visibility, investors should be aware that California’s regulatory and political backdrop could still...

Read the full narrative on Sempra (it's free!)

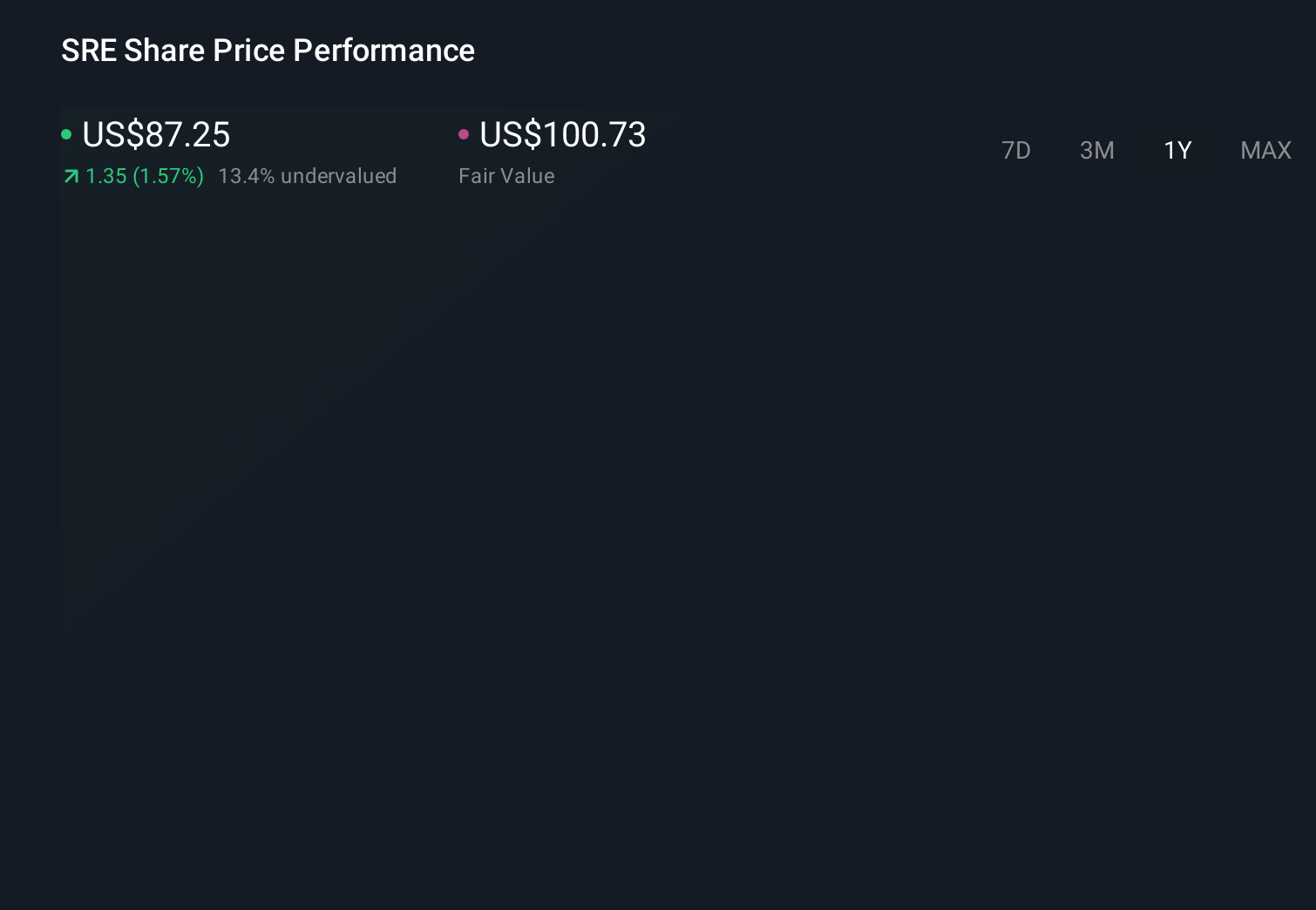

Sempra's narrative projects $16.6 billion revenue and $3.8 billion earnings by 2028.

Uncover how Sempra's forecasts yield a $100.13 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members see Sempra’s fair value between US$80.34 and US$100.13 across 3 independent views, highlighting how far opinions can differ. Against that backdrop, the recent CPUC decision on roughly 10% allowed returns shows why many investors watch California regulation so closely when thinking about Sempra’s future performance.

Explore 3 other fair value estimates on Sempra - why the stock might be worth 8% less than the current price!

Build Your Own Sempra Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Sempra research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

- Our free Sempra research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sempra's overall financial health at a glance.

Contemplating Other Strategies?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- We've found 13 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com