Nasdaq

Nasdaq 華爾街日報

華爾街日報Is Deutsche Börse Fairly Priced After Recent Gains and Capital Markets Expansion Efforts?

- Wondering whether Deutsche Börse is quietly offering value right now, or if the recent noise has already been priced in? Let us unpack what the market is really saying about this stock.

- Despite a modest 1.1% pullback over the last week, the shares are up 6.6% over the past month, while still sitting slightly negative year to date and over the last 12 months, after a strong 39.2% gain over 3 years and 73.3% over 5 years.

- Recent coverage has focused on Deutsche Börse's role in European capital markets, including ongoing efforts to strengthen its clearing and trading infrastructure, as well as strategic initiatives to expand its data and analytics offerings. Together, these developments have helped shape investor expectations around its long term growth and risk profile, which feeds directly into how the stock is being priced.

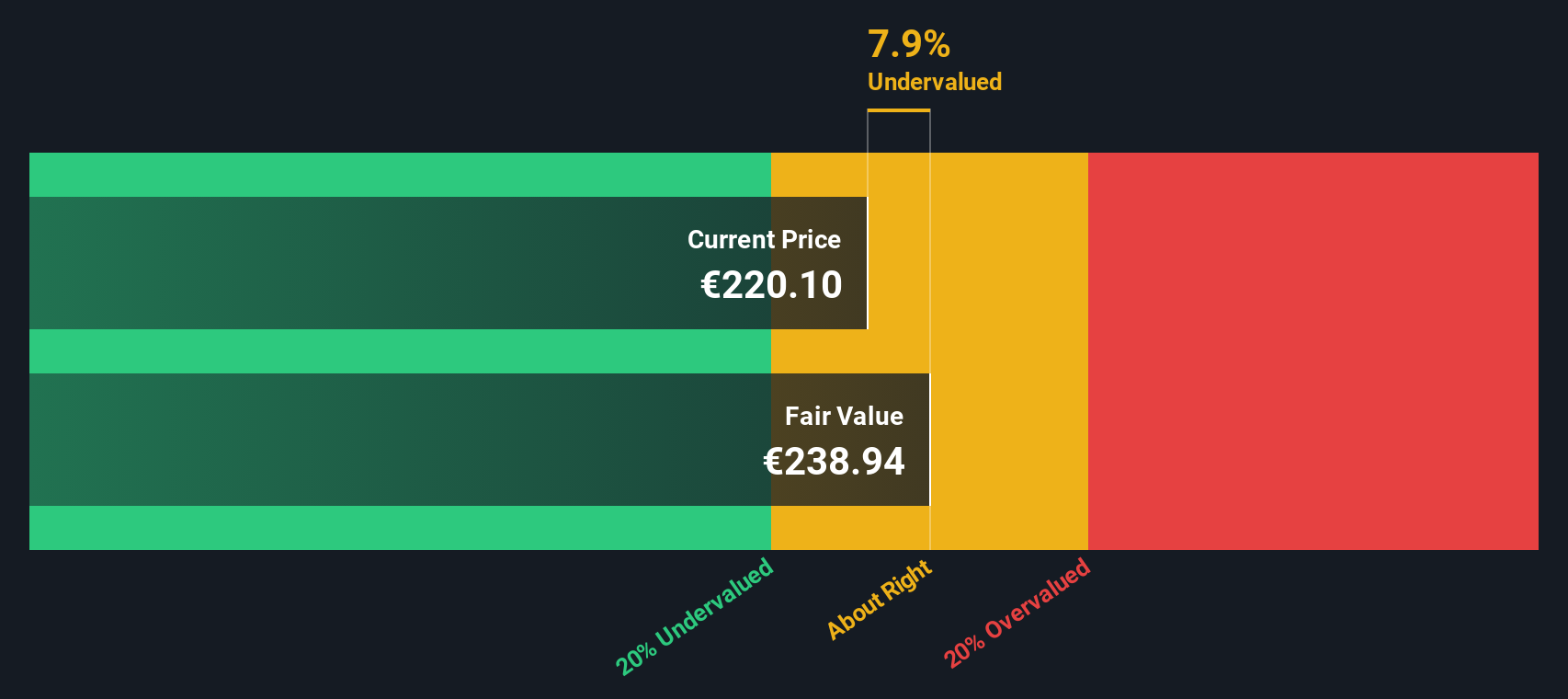

- On our framework of 6 key valuation checks, Deutsche Börse scores a solid 4 out of 6, suggesting the market may be leaving some value on the table. In the next sections we will compare the usual valuation methods, before finishing with a more holistic way to think about what the stock is actually worth.

Find out why Deutsche Börse's -1.9% return over the last year is lagging behind its peers.

Approach 1: Deutsche Börse Excess Returns Analysis

The Excess Returns model looks at how much value Deutsche Börse can create above the minimum return investors require on its equity capital. Instead of focusing on cash flows alone, it compares the company’s profitability on its equity base with its cost of equity, and then projects how long those “excess” profits can be sustained.

For Deutsche Börse, the model uses a Book Value of €58.87 per share and a Stable EPS of €12.32 per share, based on weighted future Return on Equity estimates from 10 analysts. With an Average Return on Equity of 17.12% and a Cost of Equity of €4.51 per share, the company is expected to generate an Excess Return of €7.81 per share. Analysts also see Stable Book Value rising to €71.98 per share, which suggests room for continued compounding of these returns over time.

Together, these inputs translate into an intrinsic value that implies the shares trade at an 8.8% discount. This is close enough to call them roughly fairly valued rather than a deep bargain.

Result: ABOUT RIGHT

Deutsche Börse is fairly valued according to our Excess Returns, but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

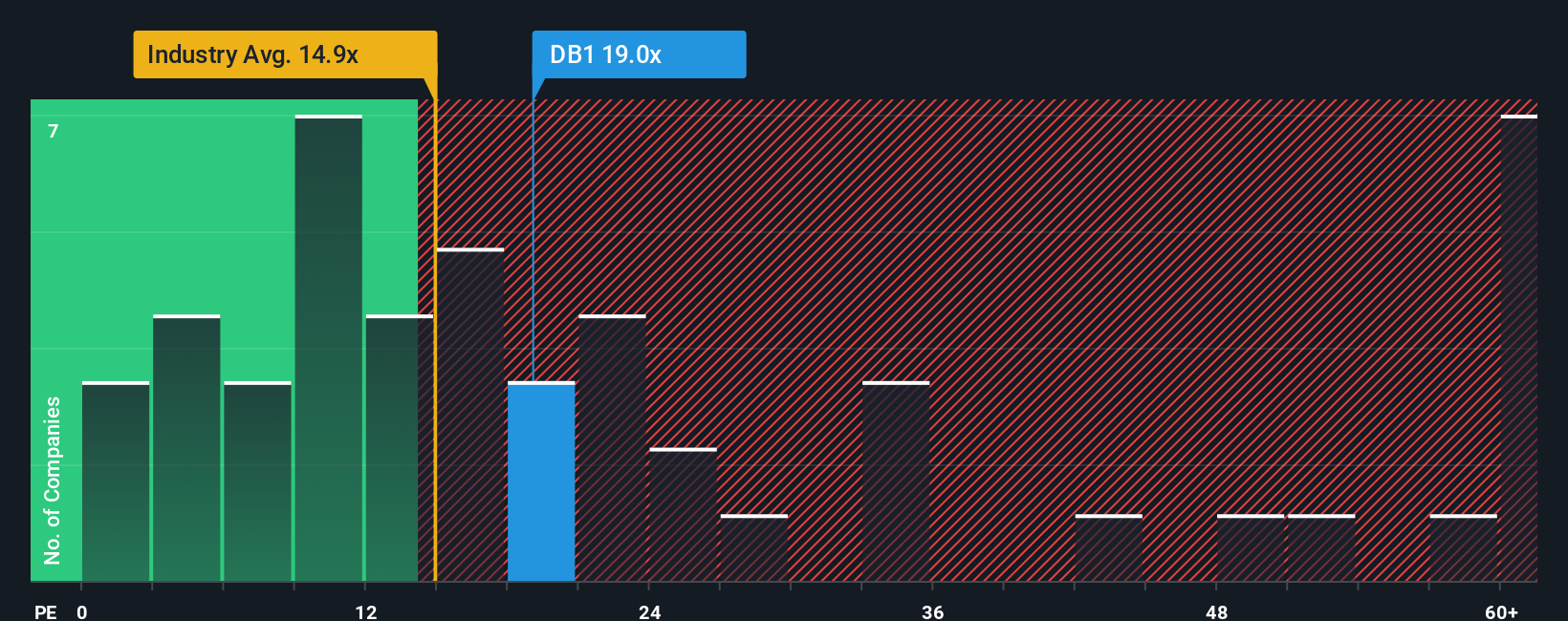

Approach 2: Deutsche Börse Price vs Earnings

For a consistently profitable business like Deutsche Börse, the Price to Earnings (PE) ratio is a useful way to judge whether investors are paying a reasonable price for each euro of earnings. In general, faster growth and lower perceived risk justify a higher PE, while slower growth or greater uncertainty call for a lower, more conservative multiple.

Deutsche Börse currently trades on a PE of 19.75x. That is above the broader Capital Markets industry average of about 14.70x, but slightly below the 21.03x average of its listed peers. To refine this view, Simply Wall St estimates a proprietary Fair Ratio of 20.65x, which reflects the multiple you might expect given Deutsche Börse’s specific earnings growth outlook, margins, market cap and risk profile.

This Fair Ratio is more informative than a simple comparison with peers or the industry, because it adjusts for the company’s own fundamentals and risk, rather than assuming all businesses deserve the same multiple. With the current PE only modestly below the Fair Ratio, Deutsche Börse appears close to fairly valued on this metric.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1463 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Deutsche Börse Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. These are simple stories you create about Deutsche Börse that tie your view of its business, future revenue, earnings and margins to a financial forecast, a fair value, and ultimately a clear buy or sell decision. All of this is available within an easy to use tool on Simply Wall St’s Community page that millions of investors already use. Each Narrative is dynamically updated as new news or earnings arrive. For example, one investor might build a bullish Deutsche Börse Narrative around successful execution of the Allfunds deal, stronger data and SaaS growth, and assign a fair value closer to the optimistic €309 target. Another investor might focus on regulatory, cost and leadership risks and land nearer the cautious €225 target. Both can then compare their own Fair Value to the current share price to decide whether it is time to buy, hold or sell.

Do you think there's more to the story for Deutsche Börse? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com