Nasdaq

Nasdaq 華爾街日報

華爾街日報Taking a Fresh Look at PennyMac Mortgage Investment Trust (PMT)’s Valuation After Its Recent Steady Climb

PennyMac Mortgage Investment Trust (PMT) has been quietly grinding higher, and that steady climb is starting to catch investors attention. With the stock up over the past 3 years, the question is whether this income focused REIT still offers value.

See our latest analysis for PennyMac Mortgage Investment Trust.

Over the past year, PennyMac Mortgage Investment Trust has seen only modest 1 year share price moves around its current 12.5 dollars level, but a solid 3 year total shareholder return above 30 percent suggests long term income and reinvested dividends have quietly rewarded patient holders, which hints that momentum is steady rather than fading.

If that slow and steady profile has you wondering what else is out there, it could be a good time to explore fast growing stocks with high insider ownership for more dynamic ideas.

With earnings growing, a modest discount to analyst targets and a still generous yield, the key debate now is simple: is PennyMac Mortgage Investment Trust undervalued, or is the market already pricing in its future growth potential?

Most Popular Narrative Narrative: 6.9% Undervalued

With PennyMac Mortgage Investment Trust last closing at 12.5 dollars and the most followed narrative pointing to fair value around 13.43 dollars, the story hinges on how profits can grow even as revenue shrinks.

Analysts are assuming PennyMac Mortgage Investment Trust's revenue will decrease by 16.8% annually over the next 3 years.

Analysts assume that profit margins will increase from 10.2% today to 55.0% in 3 years time.

Want to know how shrinking top line forecasts still support a higher value? The narrative leans on a dramatic profit rebound and a sharply lower future earnings multiple. Curious which assumptions make that math add up? Follow the story to see how those moving parts combine into the projected fair value.

Result: Fair Value of $13.43 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, rising funding costs and a potential dividend cut could quickly weaken sentiment, which may pressure book value and challenge the current undervaluation story.

Find out about the key risks to this PennyMac Mortgage Investment Trust narrative.

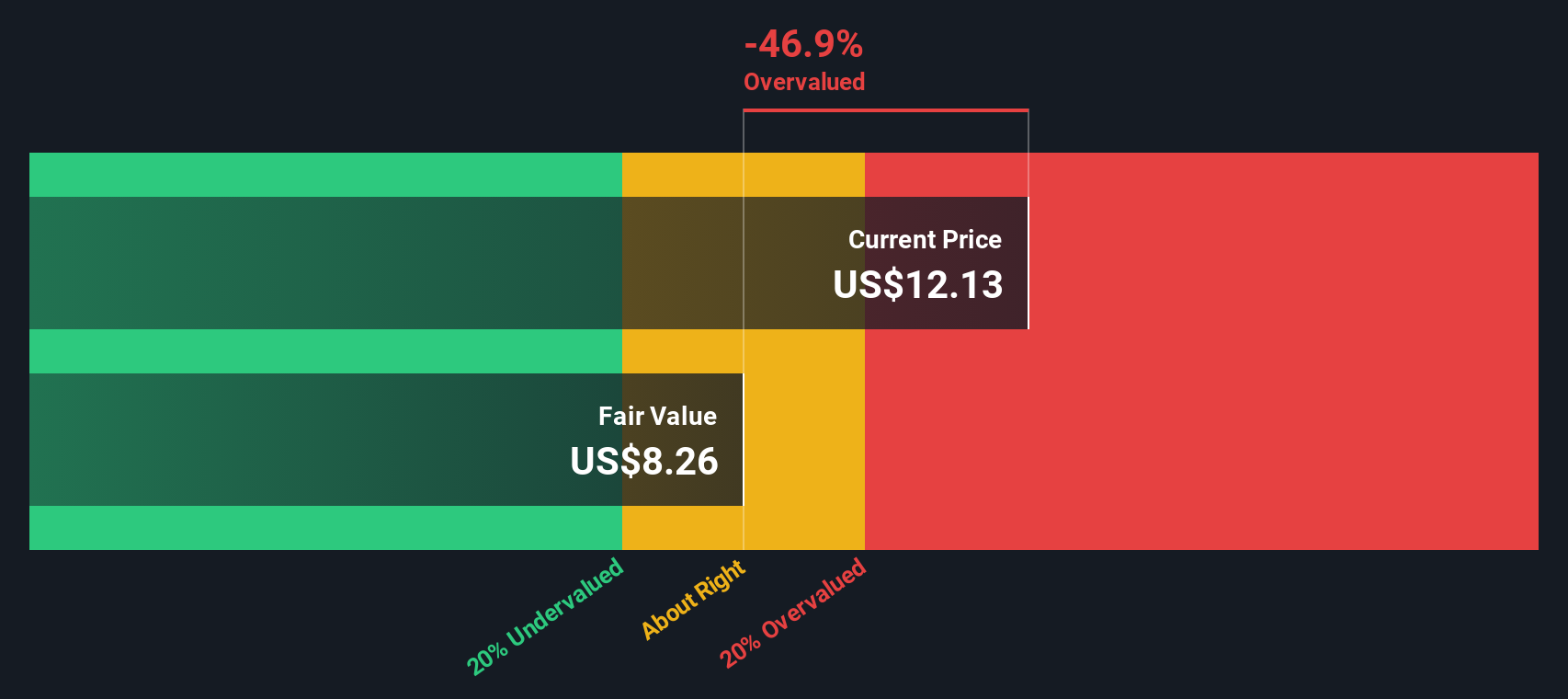

Another View, SWS DCF Flags Overvaluation

While the popular narrative sees PennyMac Mortgage Investment Trust as about 7 percent undervalued, our DCF model tells a different story. At 12.5 dollars versus a fair value of roughly 8 dollars, the stock screens as clearly overvalued, raising the question of which set of assumptions you trust more.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out PennyMac Mortgage Investment Trust for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 915 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own PennyMac Mortgage Investment Trust Narrative

If you see the numbers differently or want to dig into the details yourself, you can quickly build a personalized view in just a few minutes: Do it your way.

A great starting point for your PennyMac Mortgage Investment Trust research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Ready for your next move?

Put your research momentum to work now, or risk watching others capture the upside from fresh ideas surfaced by the Simply Wall Street Screener.

- Capitalize on potential mispricings by scanning these 915 undervalued stocks based on cash flows that look primed for a re rating as the market wakes up.

- Position yourself for the next wave of innovation by targeting these 25 AI penny stocks shaping how businesses and consumers use intelligent technology.

- Focus on steadier income potential by concentrating on these 13 dividend stocks with yields > 3% that may help support long term total returns through market cycles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com