Nasdaq

Nasdaq 華爾街日報

華爾街日報Texas Pacific Land Stock: Is TPL Underperforming the Energy Sector?

Texas Pacific Land Corporation (TPL), headquartered in Dallas, Texas, owns and manages tracts of land and resources, and water services and operations businesses in Texas. Valued at $19.3 billion by market cap, the company’s income is derived from land sales, oil and gas royalties, grazing leases, and interest.

Companies worth $10 billion or more are generally described as “large-cap stocks,” and TPL perfectly fits that description, with its market cap exceeding this mark, underscoring its size, influence, and dominance within the oil & gas E&P industry. TPL's 873,000 surface acres and 199,000 net royalty acres in the Permian Basin drive revenue through oil and gas royalties, easements, and land sales, giving it a competitive edge in scale and development potential.

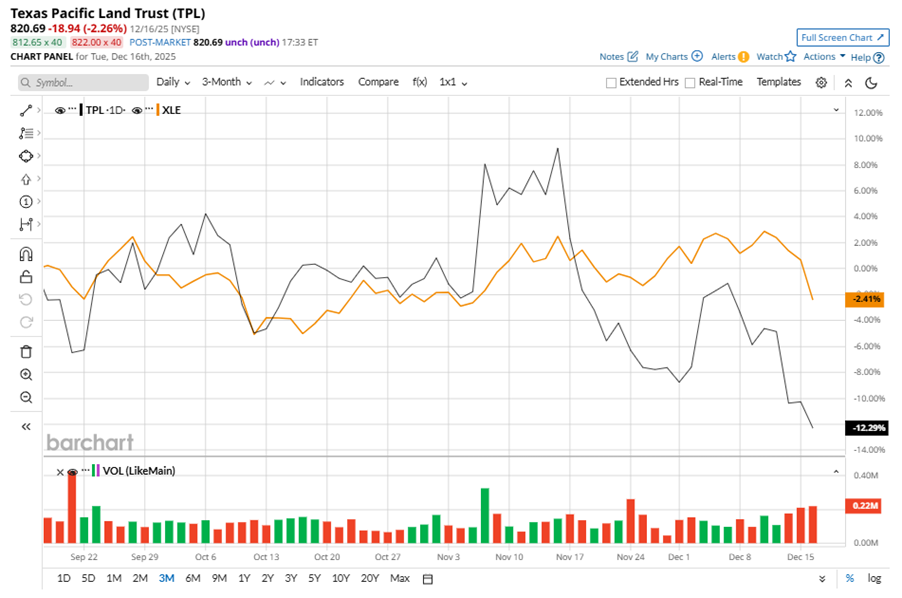

Despite its notable strength, TPL slipped 43.9% from its 52-week high of $1,462.78, achieved on Mar. 3. Over the past three months, TPL stock declined 12.3%, underperforming the Energy Select Sector SPDR Fund’s (XLE) 2.4% losses during the same time frame.

In the longer term, shares of TPL dipped 24.9% on a six-month basis and fell 32.5% over the past 52 weeks, underperforming XLE’s six-month marginal dip and slight returns over the last year.

To confirm the bearish trend, TPL has been trading below its 50-day and 200-day moving averages since late May, with some fluctuations.

On Nov. 5, TPL reported its Q3 results, and its shares closed up more than 10% in the following trading session. The company’s revenue was $203.1 million, up 8.3% from the previous quarter. Its EPS grew 4.4% from the prior quarter to $5.27.

In the competitive arena of oil & gas E&P, APA Corporation (APA) has taken the lead over TPL, showing resilience with a 16.9% uptick on a six-month basis and 9.2% gains over the past 52 weeks.

Wall Street analysts are reasonably bullish on TPL’s prospects. The stock has a consensus “Moderate Buy” rating from the two analysts covering it, and the mean price target of $842.50 suggests a potential upside of 2.7% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.