Nasdaq

Nasdaq 華爾街日報

華爾街日報Have Primoris Services Insiders Been Selling Stock?

Some Primoris Services Corporation (NYSE:PRIM) shareholders may be a little concerned to see that the Independent Director, John Schauerman, recently sold a substantial US$1.1m worth of stock at a price of US$136 per share. However, it's crucial to note that they remain very much invested in the stock and that sale only reduced their holding by 9.0%.

The Last 12 Months Of Insider Transactions At Primoris Services

In the last twelve months, the biggest single sale by an insider was when the insider, Thomas McCormick, sold US$3.9m worth of shares at a price of US$64.55 per share. That means that even when the share price was below the current price of US$128, an insider wanted to cash in some shares. We generally consider it a negative if insiders have been selling, especially if they did so below the current price, because it implies that they considered a lower price to be reasonable. Please do note, however, that sellers may have a variety of reasons for selling, so we don't know for sure what they think of the stock price. This single sale was 57% of Thomas McCormick's stake.

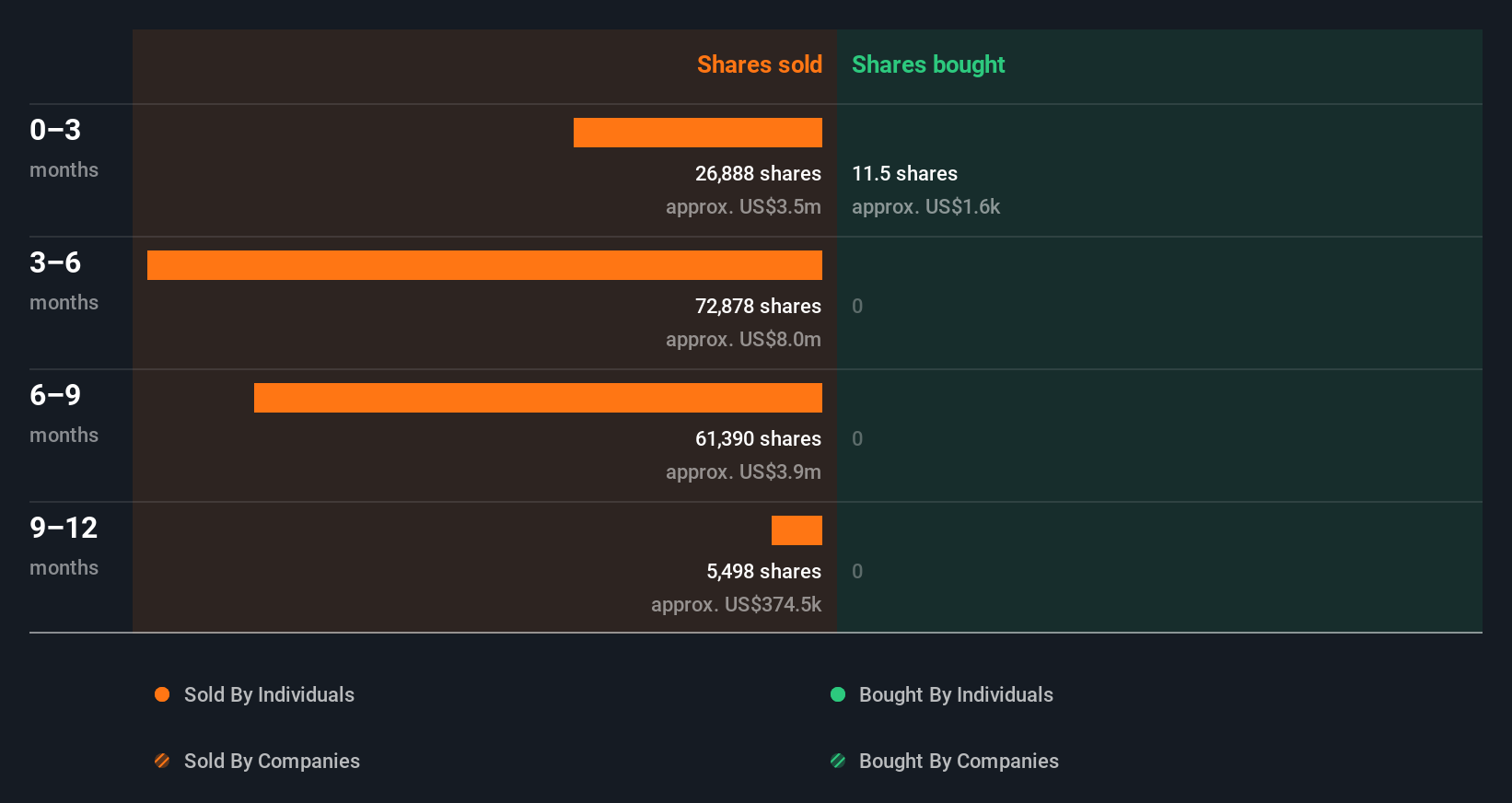

In total, Primoris Services insiders sold more than they bought over the last year. You can see the insider transactions (by companies and individuals) over the last year depicted in the chart below. If you click on the chart, you can see all the individual transactions, including the share price, individual, and the date!

View our latest analysis for Primoris Services

If you like to buy stocks that insiders are buying, rather than selling, then you might just love this free list of companies. (Hint: Most of them are flying under the radar).

Insider Ownership Of Primoris Services

Another way to test the alignment between the leaders of a company and other shareholders is to look at how many shares they own. I reckon it's a good sign if insiders own a significant number of shares in the company. Primoris Services insiders own about US$61m worth of shares. That equates to 0.9% of the company. This level of insider ownership is good but just short of being particularly stand-out. It certainly does suggest a reasonable degree of alignment.

What Might The Insider Transactions At Primoris Services Tell Us?

The stark truth for Primoris Services is that there has been more insider selling than insider buying in the last three months. Zooming out, the longer term picture doesn't give us much comfort. But since Primoris Services is profitable and growing, we're not too worried by this. While insiders do own shares, they don't own a heap, and they have been selling. We'd practice some caution before buying! So these insider transactions can help us build a thesis about the stock, but it's also worthwhile knowing the risks facing this company. In terms of investment risks, we've identified 1 warning sign with Primoris Services and understanding this should be part of your investment process.

Of course Primoris Services may not be the best stock to buy. So you may wish to see this free collection of high quality companies.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions of direct interests only, but not derivative transactions or indirect interests.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.