Nasdaq

Nasdaq 華爾街日報

華爾街日報CITIC Securities: The maturity of fixed deposits may become an important variable. Bank fundamentals and capital are expected to benefit in both directions

The Zhitong Finance App learned that CITIC Securities released a research report stating that the entire society's fixed deposit scale for 2 years or more due in 2026 may reach 45 trillion yuan. With the migration of time deposit funds, banking fundamentals and investment capital will benefit in both directions. For banks, on the one hand, fundamental benefits; on the one hand, the reduction in the share of long-term deposits has a debt cost saving effect; on the other hand, valuation benefits. The entry into the market of absolute yield incremental capital driven by deposit moving is conducive to a stable return industry. The bank continues to be optimistic about the stable return asset attributes of the banking sector in the next stage.

CITIC Securities's main views are as follows:

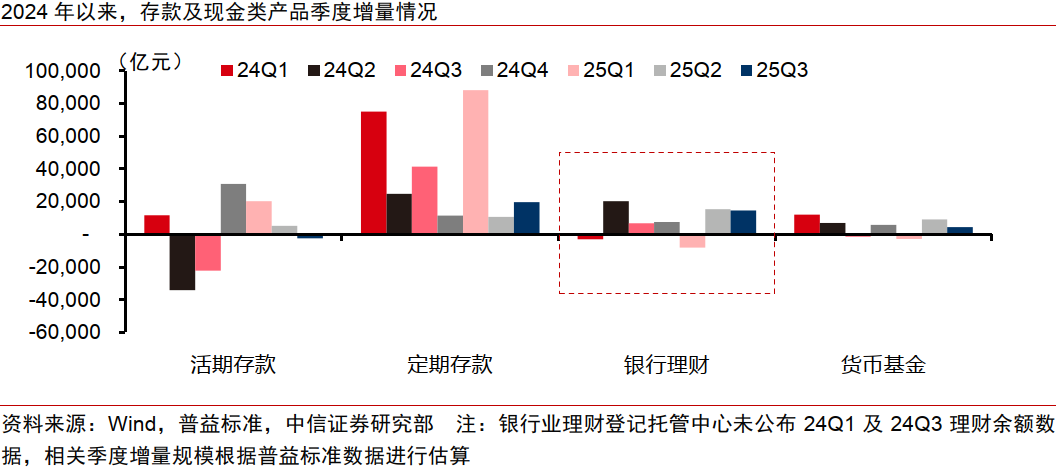

The origin of the report: The concentrated maturity of bank term deposits in 2026 may become an important variable affecting the performance of financial products and financial markets next year.

Factors influencing fixed deposit: Highly correlated with revenue expectations and yield ratio. Take a look at the replay:

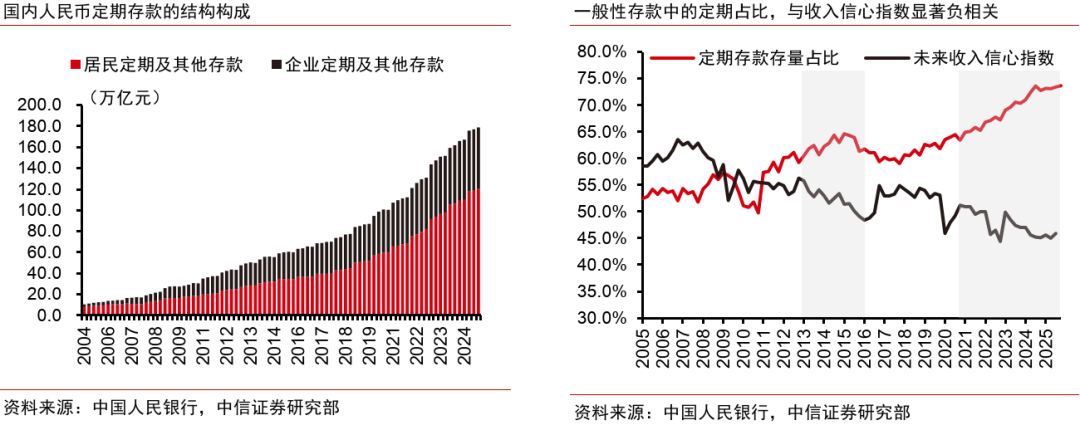

1) The share of time deposits in the whole society is significantly negatively correlated with the future income confidence index. During the period when the income confidence index declined in the future (such as 2013-2016, 2021 to now), the share of time deposit stocks in the whole society showed an upward trend.

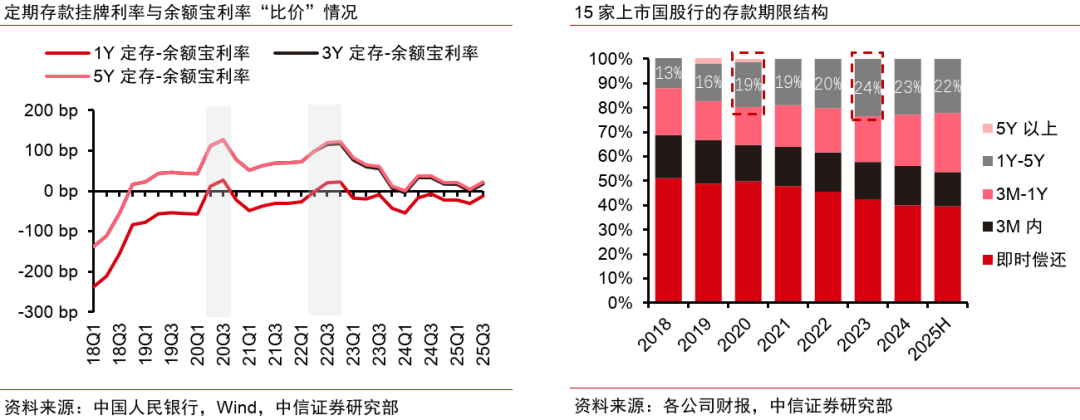

2) The term structure of time deposits is closely related to the “price comparison relationship” of various types of deposits. In 2020 and 2023, when the difference between long-term term deposits (3 years, 5 years) and balance benefits was high, the share of China Stock Bank deposits with a remaining term of 1 to 5 years (mainly 3-year deposit types) increased significantly.

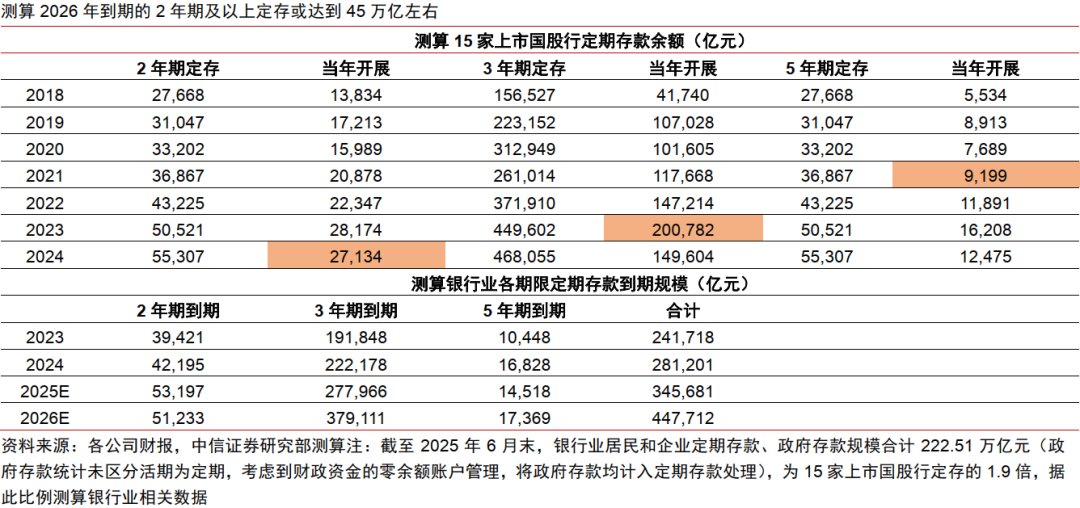

According to estimates, the amount of medium- to long-term fixed deposits due in 2026 may reach 45 trillion yuan.

According to deposit maturity distribution data published by 15 stock banks in listed countries, the bank estimates the new development of time deposits for each year and period in the past. The conclusions are as follows:

1) The maturity amounts of medium- and long-term fixed deposits in 2025 and 2026 were 35 trillion yuan and 45 trillion yuan respectively, which is significantly higher than the maturity scale of 20-30 trillion yuan in previous years;

2) The three-year fixed deposit will be carried out intensively in 2023, and the amount due in 2026 may reach 38 trillion yuan;

3) Some regional banks account for a higher proportion of long-term limited deposit maturities than the industry: In comparison, retail specialty banks and banks that have continued to promote pricing management in recent years account for a lower share of medium- to long-term deposits, and some urban commercial banks in the central and western regions account for a relatively high proportion of medium- to long-term deposits.

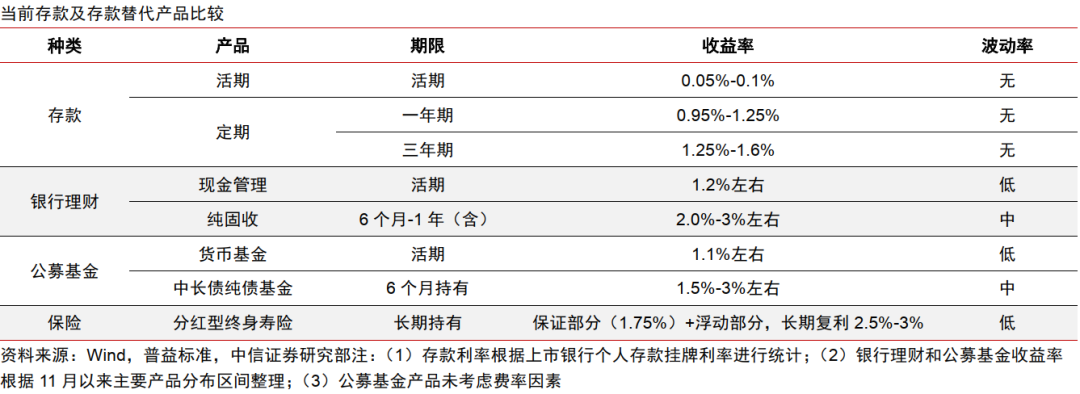

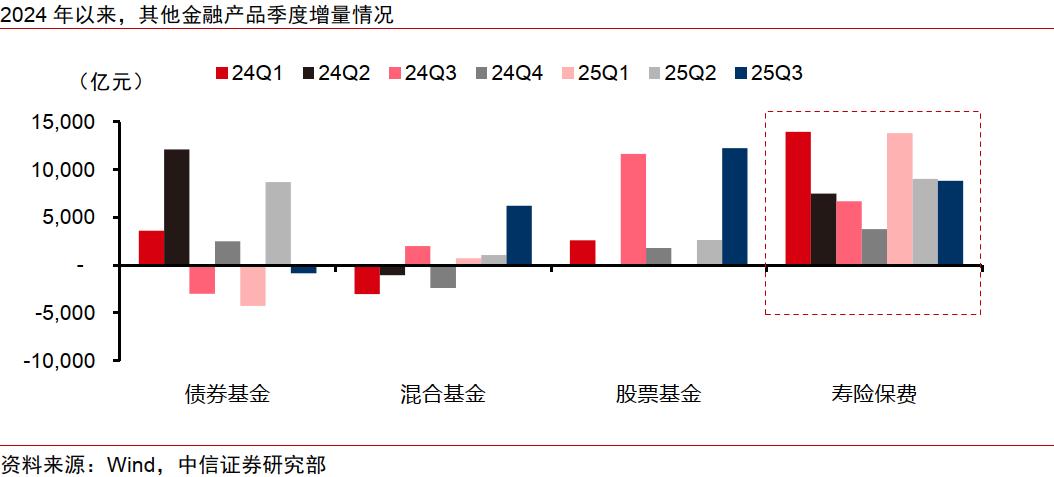

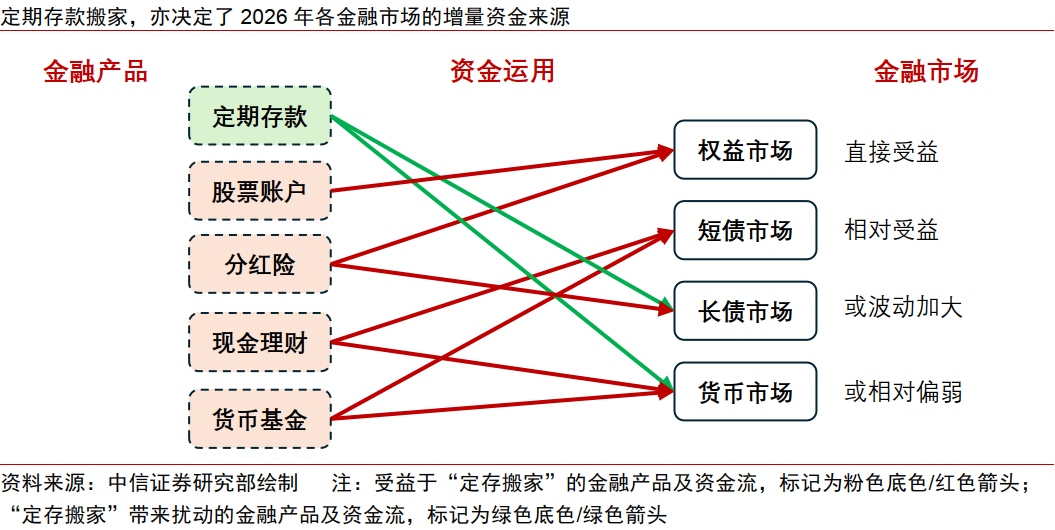

Financial products and market outlook: Short-term deposits, dividend insurance and other products benefit, equity and short-term debt markets.

1) Looking at bank deposits, short-term or directional. After deposit interest rates continued to decline, the possibility of renewing the original term of medium- to long-term fixed deposits at maturity declined, and residents were more likely to choose short-term fixed deposit products.

2) Looking at financial products, dividend insurance and cash management products are expected to benefit. Combined with price comparison factors and channel factors, cash management products and dividend insurance products may become direct beneficiaries of “fixed deposit and moving”, which was evident in the second half of 2025.

3) Looking at the financial market, the equity and short-term debt markets are more beneficial. Among them, the equity market directly benefits from the incremental allocation of insurance capital and the direct entry of a few high-profile funds into the market. The short-term bond market mainly benefits from cash management and financial management and the allocation needs of monetary funds, while the money market and long-term bond market may fluctuate more due to bank liquidity management.

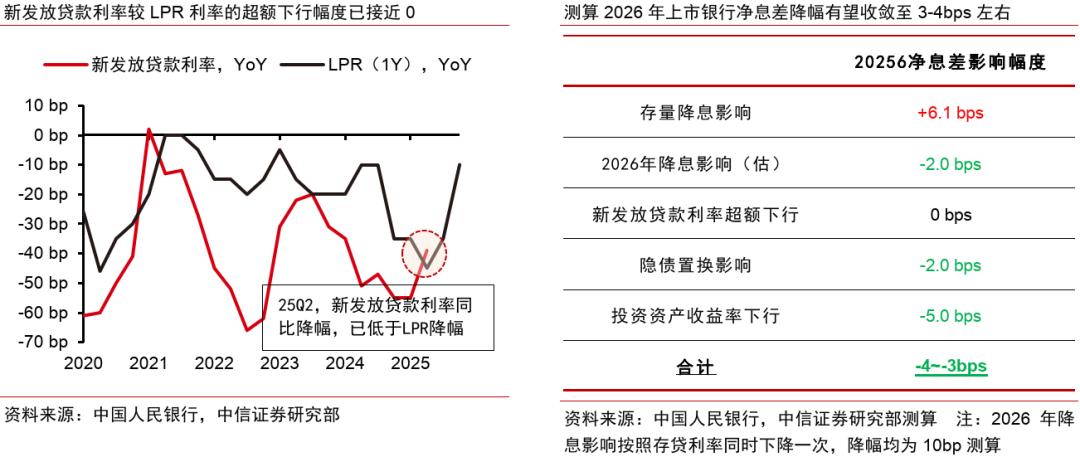

Bank balance outlook: Shorter deposit periods help to “control capital”, but liquidity management requirements have increased.

1) Deposit interest rates and net interest spreads may benefit. Considering differences in pricing levels, shortening general deposits and non-banking general deposits all help reduce the level of interest payments on bank deposits. The bank predicts that due to declining deposit costs and a decrease in the frequency of interest rate cuts, the net interest spreads of listed banks may decline to around 3-4 bps in 2026.

2) Increased liquidity management requirements. Compared to general deposits, non-bank deposits have higher requirements for bank liquidity management due to their weak stability (settlement interbank deposits are obvious). On the one hand, shortening of deposits and non-bankability affects banks' provision management at important points, and on the other hand, they have a negative impact on indicators such as LPR and NSFR.

Risk factors:

The quality of bank assets deteriorated beyond expectations; adverse changes in regulation and industry policies.