Nasdaq

Nasdaq 華爾街日報

華爾街日報CITIC Construction Investment Game Industry Investment Outlook 2026: Strong supply and demand drive high gaming boom, opening an upward channel for profit margins

The Zhitong Finance App learned that CITIC Construction Investment released a research report saying that in 2025, strong supply and demand in the game industry will drive the boom in the industry, and prosperity and profit margins may continue to rise next year. As supply-side version growth (23% increase in the first 10 months of 2025) supports subsequent flows, Tencent (00700), NetEase (09999), and new Miha tours are concentrated, and innovative categories (such as SLG+ elimination, creative chess, emerging women, etc.) have sufficient potential to weaken channel bargaining and increase AI purchasing efficiency, and profit margins continue to rise. Furthermore, judging from the AI progress described by various game companies in their financial reports, AI has been widely used in the entire process of game development and operation, and is expected to improve the efficiency of game development and operation.

CITIC Construction Investment's main views are as follows:

Gaming: The boom continues, profit margins rise, and integrated categories continue to gain strength

Strong supply and demand in 25 years have driven the boom in the industry

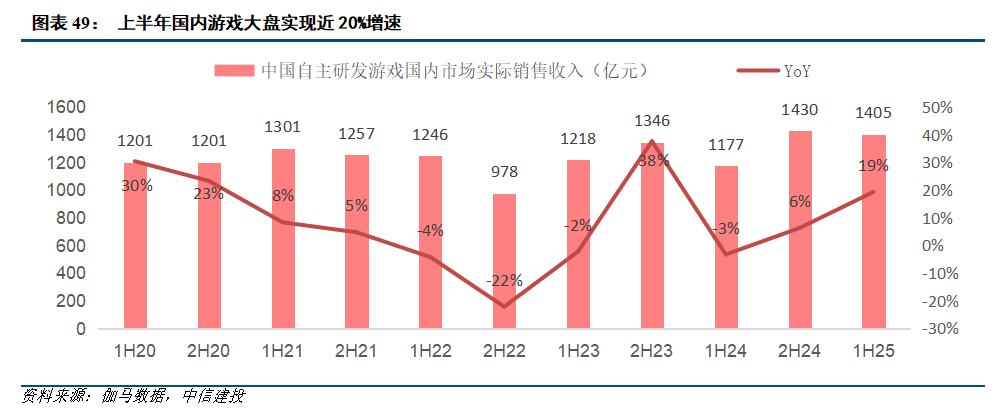

The game industry is booming this year. In the first half of the year, the market still grew by nearly 20% on a 100 billion dollar scale. In the first half of 2020, users stayed at home for a long time, and demand for online leisure and entertainment increased, driving the scale of online games independently developed by China to increase 30% year-on-year to 1201 billion yuan. Although popular games such as “Genshin” contributed more in the first half of '21, the number of domestic game users peaked (0.22% growth rate for domestic game users in '21), time spent at home was shortened, and the growth rate of the game market slowed to 8.30% in the first half of '21. Since then, due to factors such as underage addiction prevention and version control, the scale of the 1H22, 1H23, and 1H24 markets all declined slightly.

1. Supply side: The monthly version doubles in two years, and fun new games are constantly emerging

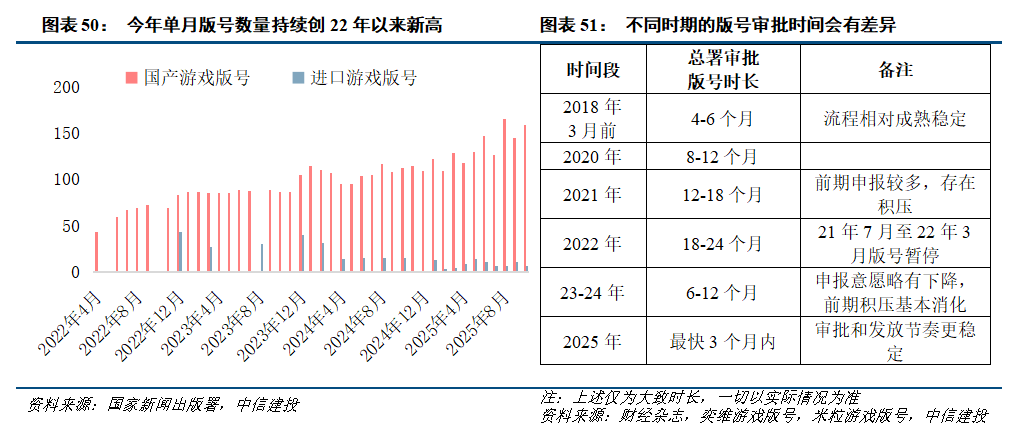

Judging from the number of editions, there has been sufficient supply since this year, and the cumulative number of editions distributed in January-October increased by 24% over the same period last year. From January to October of this year, a total of 1,441 domestic+imported versions were distributed, an increase of 24% over the previous year. The total number of models produced in China was 1,354, an increase of 26% over the previous year. Furthermore, the number of domestic editions distributed in a single month showed an overall upward trend. The peak was in August, reaching 166 models, a new high since the edition was restarted in April '22; imported editions were around 10 models per month, and the frequency of edition distribution was shortened from once every 2 months last year to once a month.

Judging from the version number approval cycle, it has been shortened to less than 3 months as soon as this year, and the pace of approval is more stable and predictable. An application for a game version requires three steps: compilation of application materials by the publishing house, approval by the Provincial Press and Publication Administration, and approval by the National Press and Publication Administration. Previously, there were two rounds of version suspension. One round was institutional reform in 2018, and the other round was 2021-2022. The suspension of edition numbers combined with many game versions declared in 2019-2020, resulting in a longer period of time to approve the 2021-2022 version. Since 2023, version approval has been shortened to less than one year, driven by multiple factors such as a slight decline in the willingness to file a version number, basic consumption of the backlog in the early stages, and optimization of the General Administration's approval process. It can be approved within 3 months as soon as this year, and the distribution of version numbers is more stable and the pace of approval is more predictable, so that game manufacturers can prepare for game launch at a more rapid pace.

Policy temperatures also continue to pick up. Since this year, there have been frequent developments in game policies, including support for cultural going overseas at the national level, tax cuts for cultural powerhouses, online publishing, and IPO refinancing, as well as industry policy support at the local level and simplification of version approval procedures.

1) At the national level, in April, there were three consecutive initiatives to support game development. Specifically, the “Internet Publishing Science and Technology Innovation Leadership Plan” issued by the State Press and Publication Administration and others to implement tax support policies to support IPO/mergers and acquisitions/refinancing; “Qiushi” magazine published to accelerate the construction of a strong cultural nation, mentioning that some Chinese literary works, online games, and online movies and TV dramas have successfully gone overseas in recent years, highlighting the power of Chinese culture; the press conference of the State Information Office on April 21 introduced the “Comprehensive Pilot Work Plan to Accelerate the Expansion and Opening-up of the Service Industry”, which mentioned the “Comprehensive Pilot Work Plan for Accelerating the Expansion and Opening Up of the Service Industry” IP builds an industrial chain from game production, distribution, and overseas operations.

2) At the local level, in May, Guangdong introduced “Certain Policies and Measures to Promote the High-Quality Development of Guangdong's Online Game Industry”, including supporting games with good cultural communication skills, creating overseas industry clusters, and supporting the diversified transformation of game IPs; in June, Zhejiang issued “Certain Measures to Support Games Going Overseas”, which mentions actively cultivating players in the overseas game market and supporting the development and cooperation of original boutique games; in July, Shanghai proposed “a policy pilot project to treat game products developed by foreign-funded game companies in Shanghai as domestic games in due course”, which is expected to accelerate the launch of games developed by foreign-funded enterprises in China .

2. Demand side: games are very “time-grabbing”, resilient, and pervasive

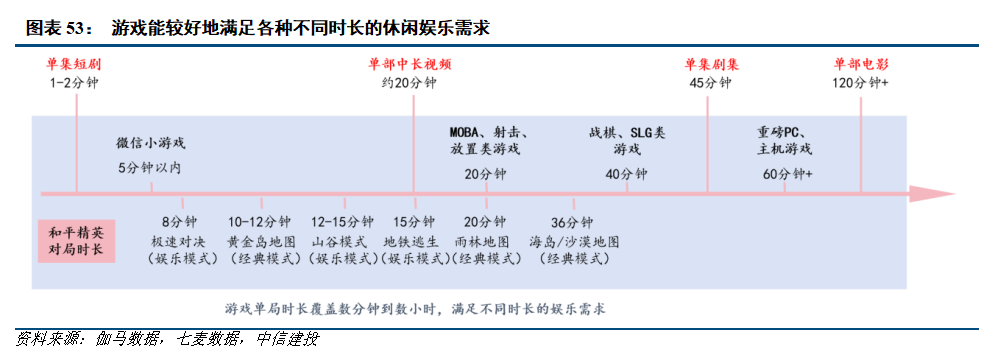

Duration dimension: Whether it's fragmented time of less than 5 minutes or more of in-depth entertainment needs, the game can meet the needs of 1 hour or more. With rich game categories and product forms (mini games, apps, console games, etc.), games basically meet users' leisure and entertainment needs for different periods of time.

1) Fragmentation time of about 5 minutes: WeChat mini game. According to the WeChat Open Course, a single game currently lasts 1-3 minutes.

2) Moderate entertainment requirements of about 20 minutes: MOBA, shooting, and placement games represented by “Wang Zhe Rongyao” and “Operation Delta”. For example, the duration of a single game in the different modes of “Operation Delta” is about 20 minutes, the mobile “Occupy Match” and “Blitz” sessions are 18 and 12 minutes respectively, and the PC “Occupy Match” and “Blitz” are 24 and 15 minutes respectively. The “Fearless Pact” mobile game standard and ranked modes average 20 to 30 minutes per game, while speed mode and practice mode only take 10 minutes per game.

3) Medium to long entertainment needs for about 40 minutes: Chess and SLG games represented by “The Battle of the Golden Shovel” and “The Three Kingdoms Conquer the World”. For example, the duration of a single game in “Battle of the Golden Shovel” is limited to 35-40 minutes. “Kingshot” takes about 30-60 minutes every day to participate in league activities, compete for resources, and hero development.

4) In-depth entertainment requirements for an hour or more: Major PC and console games represented by “Black Myths: Goku”. In June '25, Ren Zhiguo, general manager of Tencent IEG Northern Lights A1 Studio, mentioned that PC and console game users spend 3-5 hours online every day, which is twice that of mobile games. Mobile games often provide more complex operation methods and plot settings to meet leisure and entertainment needs with plenty of time and high immersion requirements.

Compared to other forms of entertainment, the game offers more freedom. Compared to pre-produced entertainment content such as skits, movies, series, and music, the game has more freedom, participation, and immersion. On the one hand, because of the rich variety of games, the game covers leisure and entertainment needs from a few minutes to a few hours; on the other hand, even within a game, different gameplay modes can cover different hours of entertainment. For example, “Peace Elite” has spawned more than 10 gameplay modes. The shortest gameplay is speed battles in the entertainment mode, which only takes 8 minutes; while the Golden Island, Rainforest, and Desert maps in classic mode take 10, 20, and 36 minutes for a single game, respectively, and the time span is quite large.

The bank expects the amount of time users allocate to games to increase in the first half of the year. In a situation where internet traffic is basically at its peak and users have limited time, different forms of entertainment need to compete for users' limited time and attention. Gaming and other forms of entertainment compete. The most intuitive expression is the proportion of time users allocate to games. The bank expects a significant increase in game time in the first half of this year compared to 24 years. The first reason is that the domestic game market increased by nearly 20% year-on-year in the first half of the year, and the number of game users grew less than 2%. With payment rates and user sizes stabilizing, more time can bring more traffic, thereby bringing more market size; second, both Evergreen Games and new games exceeded expectations in the first half of the year. Among Changqing games, the “Wang Zhe Rongyao” and “Crossing the Line of Fire” mobile games reached a record high in the second quarter, “Fifth Personality” reached a record high in the first quarter, and the “Peace Elite” model “Subway Escape” achieved 37 million daily activities during the May 1st period (daily activity penetration rate of nearly 50%). The main reason behind this is new gameplay and new operation activities that are frequently updated to attract old users to spend more time on the game. Among the new and sub-new games, “Operation Delta,” “Operation Supernatural,” and “The Legend of Staff and Sword” are highly popular and receive incremental time allocations.

Payment level: Game prices range from a few yuan to more than 10,000 yuan to meet the needs of users with different consumption levels. The variety of games is rich and the price range covered is relatively wide, thus meeting the entertainment needs of users with different consumption levels. For example, the daily ARPU for elimination, gaming, and casual sports games is generally less than 1 yuan; the daily ARPU for shooter and MOBA games is generally 1-2 yuan; the daily ARPU for RPG, SLG, and simulated management is concentrated at 4 yuan or more. At the same time, the maximum payment limit for the game is also very high; the price of scarce warlords in “Three Kingdoms” can reach 10,000 yuan or more. In contrast, although the price of online series and music is low but not immersive, it may not meet the entertainment needs of some high-end users; the time and money costs of offline travel, concerts, movies, and screenplay games are all high, and may not meet the needs of some users seeking value for money.

According to data from the Game Industry Committee, single-user game revenue increased 13% year-on-year in the first half of this year. Based on actual sales revenue and user size estimates in the domestic game market in the first half of the year, the bank's revenue for the first half of the year reached 248 yuan, an increase of 13% over the previous year. Both absolute value and growth rate hit new highs in the same period since 21. The bank believes that the core driving force for growth is the increase in game user time, and users are willing to tilt more leisure and entertainment budgets towards games.

In '26, the number of new supplies was higher, and the integration of categories was richer

The bank believes supply will continue to improve in 2026. Looking back at popular new games in 2025 (Delta, Supernatural, Sword of Staff), most of them were released in 2024 and before, and the number of editions continued to increase from January to October 2025. It is expected that these versions will continue to be released in 2026 and beyond.

The profitability of listed companies has increased, the motivation to set up projects is higher, and the quality is higher

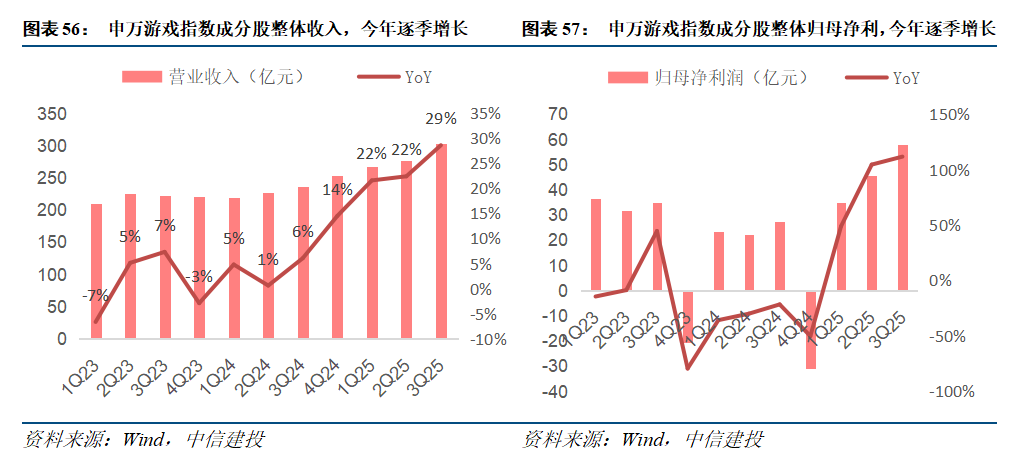

The boom in the game industry in the first three quarters of this year drove game companies' revenue, profits, and cash flow to grow significantly. Looking at the overall situation of the constituent stocks of the Shenwan Gaming Index, the revenue growth rates for the first three quarters of this year were 22%, 22%, and 29%, respectively, and the growth rate and absolute value hit new highs in 23 years; net profit growth rates to the mother were 49%, 104%, and 112%, respectively. Sales and R&D investment were restrained, and revenue growth was not at the expense of profit. Judging from the individual stock situation, ST Huatong's profit growth rate in the first three quarters was over 100%, and the profit growth rates of Giant Network and Gigabit showed a quarterly growth trend.

After team adjustments over the past two years and the accumulation of performance this year, game companies have more motivation to set up projects and are of higher quality.

1) Game companies are gradually establishing competitive tracks, and the success rate is higher. Ma Xiaoyi, senior vice president of Tencent in '24, publicly stated that those that can only rank in the top ten in the category and never have a chance to challenge first and second; they are just trying to earn some short-term income; it's better not to do it. At the end of '24, Gigabit also emphasized investing resources in leading projects to create quality products. It is expected that each region will have at most one large-scale new project (game gyroscope). On the other hand, categories are also more focused. For example, Kaiying Network focuses on IP-based MMORPGs, gigabit focuses on MMOs and SLG, and 37 Mutual Entertainment focuses on MMORPGs and SLG. Through the above two major changes, game companies' project success rates have increased significantly. For example, Giants' “Operation Paranormal” is a new product launched in the first quarter of '24.

2) The R&D expenses of leading game companies increased significantly in the third quarter of this year. The bank expects the expansion of R&D teams to be one of the main driving forces. The absolute R&D expenses of ST Huatong, Giant Network, and Gigabit in the third quarter reached 7.6, 3.4, and 280 million yuan respectively, an increase of 2.6, 130, and 100 million yuan over the second quarter, and the growth rate was over 45%. The increase in R&D expenses is expected, on the one hand, to be an increase in bonuses due to the high turnover of game products, and on the other hand, it is also driven by the expansion of R&D teams of various companies. The new team is expected to bring more possibilities to each company's new products.

Fusion categories are constantly rotating. For 26 years, I have been optimistic about two-dimensional, RPGs, and women's transformation

There has always been a phenomenon of category rotation in the game industry. Since 2020, “Genshin” and “Collapse: Stardome Railroad” have led two-dimensional games, and party games represented by “Egg Party” and “Yuanmeng Star” have risen strongly in 2024-2025. The category keywords for 2024-2025 are FPS, SLG, search and retreat, and horror. The high-profile games “Fifth Personality”, “Operation Supernatural”, and “Operation Delta” all have one or more of the above characteristics. In 2026, we will focus on integrating the rotation of innovative categories, including Tencent's “Under a Stranger”, NetEase's “Infinity”, and “Sea of Oblivion”. RPG+IP, Bilibili's “Three Kingdoms 100 Generals” creative chess, Baiao's “Code Name Bang Bang” for women + action.

The trend of increasing profit margins in the industry remains unchanged, and there are new changes in marketing/distribution/R&D

Marketing: Traditional purchases are declining, and the share of content/community/live streaming is increasing

Game promotion forms have diversified, and the proportion of content/community/live streaming marketing has increased. As traditional purchasing costs continue to rise, game companies tend to have stricter ROI controls on purchasing volume, and the younger generation of game users increasingly prefer to obtain information through social platforms such as Douyin and Xiaohongshu. The share of traditional purchases is declining, and the share of content/community/live streaming marketing is increasing. Although there is no third-party data to accurately calculate the budget share of different marketing methods, the bank can verify this trend from three perspectives:

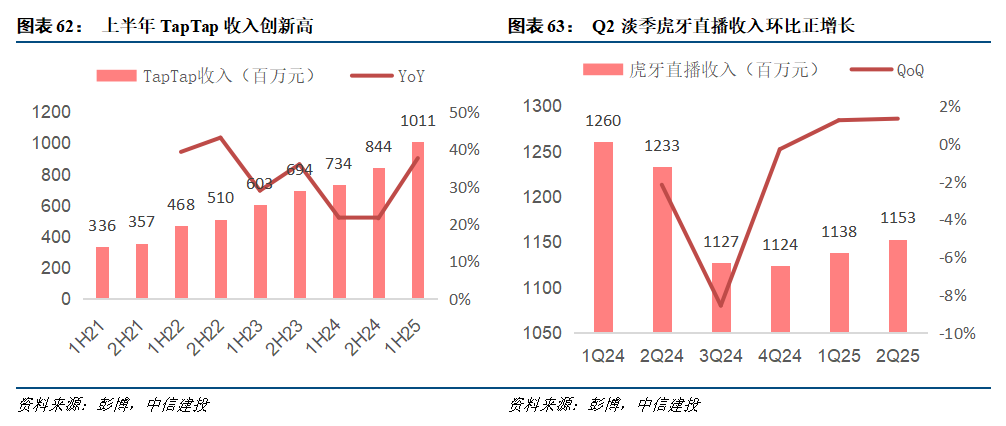

1) Since this year, the performance of game communities represented by TapTap and Huya has exceeded expectations, reflecting the game's marketing budget being skewed more towards game community platforms. The ROI of TapTap streaming ads and Huya live streaming is higher than traditional purchases. First, because these two platforms gather a large number of heavy game users and can more accurately match the target game audience and reduce ineffective marketing; second, strong interactive scenarios such as community discussions and live streaming are easier to stimulate user downloads and increase conversion rates. In the first half of the year, TapTap's revenue reached a record high of 1.01 billion yuan, a year-on-year increase of 38%, and the growth rate also hit a new high in 23 years; in the second quarter, Huya Live's revenue was 1.15 billion yuan, and it still achieved positive month-on-month growth during the off-season.

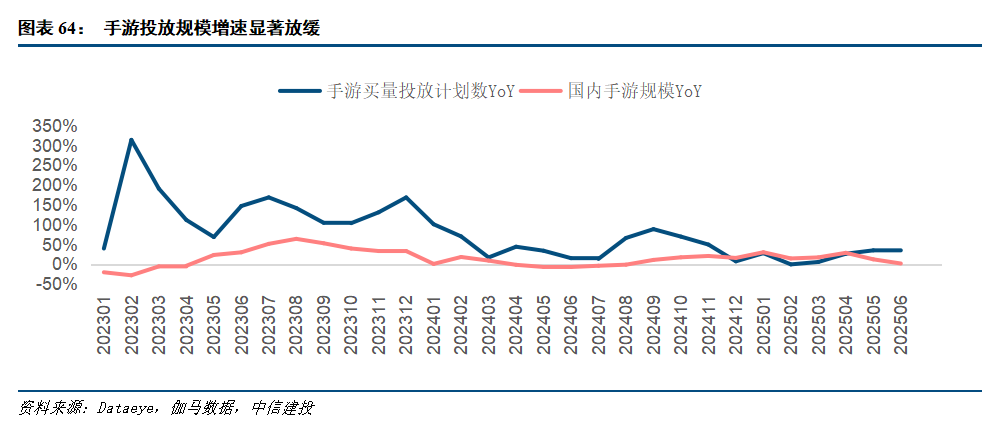

2) While the scale of mobile games has accelerated since this year, the growth rate of launch scale has slowed significantly. The number of domestic mobile game purchase plans increased 22% year on year in the first half of the year, only slightly higher than the 17% growth rate of the mobile game market during the same period. In some months, the mobile game market size growth rate was even higher than the growth rate of the purchase volume scale. This is quite different from the situation where the purchase volume more than doubled year on year in 23-24. It reflects a decline in the share of traditional purchases.

3) Through marketing adjustments, some game companies have drastically reduced sales expenses, driving double-digit growth on the profit side. Compared with traditional purchases, the single capital investment threshold for new marketing methods such as KOL cooperation and content marketing is lower. Companies that launched new games this year generally did not see a significant increase in sales expenses; some companies that focus on operating old games have also drastically reduced sales expenses through marketing adjustments. For example, the new games “The Explosion of Time” and “Heroes Don't Flash”, which were launched in the first quarter of 37 Mutual Entertainment, reduced sales sales in the second quarter, driving down 47% of sales expenses in the second quarter, down 8 pcts year on year, down 10 pcts from month to month; in the third quarter, sales expenses were reduced again to 45%, down 12 pcts year on year, down 2 pcts month on month. The decline in the sales expense ratio drove the company's net profit to mother to maintain a growth rate of more than 20% even though no large number of new products were launched in the second or third quarter. In the first half of '25, sales expenses for the first half of '25 were 840 million yuan, down 63% from the previous year, the sales expense ratio was 42%, down 29 pcts from the previous year, driving net profit for the first half of the year to a profit of 650 million yuan (-380 million yuan in the first half of '24)

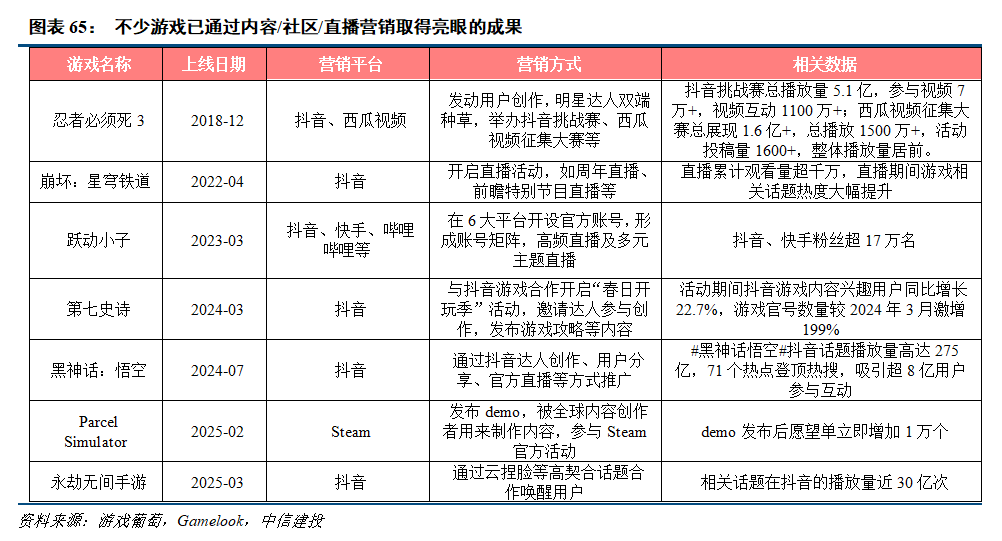

At present, quite a few games have achieved impressive results through content/community/live streaming marketing. According to the 2024 China Mobile Game Advertising and Marketing Report, over 80% of leading mobile games have set up official accounts on platforms such as WeChat video accounts, Douyin, Kuaishou, Bilibili, and TapTap. In addition to posting game information, they also carry out activities and comment area interactions to enhance communication between developers and users. On the Douyin side, “Everlasting Mobile Game” launched an AI face-pinching campaign through the official Douyin account. Related topics were broadcast nearly 3 billion times on Douyin; “Collapse: Stardom Railway” launched a series of live streaming events such as anniversaries and forward-looking special programs on Douyin, with a cumulative total of over 10 million viewers. On the Bilibili side, Tencent's “Operation Delta” became a typical example of game marketing at Station B. During the warm-up period, a large number of videos were played over 1 million. During the public beta phase, the total number of game users was nearly doubled through content, live streaming, and streaming on Station B.

Distribution: The voice of traditional intermodal transport channels is being challenged

The dispute between “Fortnite” and Apple has already had basic results, and it has become an important milestone for game developers to bypass traditional intermodal channels for revenue sharing. Epic Games, the developer of the overseas shooter “Fortnite”, led users to buy in-game virtual currency through external payment channels in order to bypass 30% of the iOS channel turnover, thus triggering a legal dispute with Apple. On April 30, 2025, a US court ruled that Apple will not charge any fees for purchases outside the app, nor can it restrict developers from guiding users to make purchases outside the app. This case shows that with the further improvement of the law, iOS apps are also expected to pay through external payment channels, and the TapTap game platform community with lower sharing rates is expected to become one of the main external payment channels.

Many of the most popular games have not been launched on the Android intermodal channel in the past 5 years, and this year's hot new products “Operation Supernatural” and “The Legend of Staff and Sword” have also not been launched. According to the bank's statistics, since 2019, top games such as “Genshin”, “Collapse: Stardom Railroad”, and “Dungeons and Warriors: Origins” have not been launched on the Android intermodal channel. If these blockbuster products themselves have a high level of popularity, they can achieve impressive user data even without an Android intermodal channel; then since this year, the three medium-sized products “Asking Sword of Eternity”, “Operation Supernatural”, and “Legend of the Sword of Staff” have also exceeded expectations when not launched on the Android intermodal transport channel, which further reflects the remarkable effects of emerging distribution channels such as TapTap, and the important role that user word of mouth has played in game promotion.

Ultimately, for game companies, since the game's official website and TapTap both have zero share, while the AppStore and Android intermodal transport channels have a turnover ratio of 30% to 50%, it is expected that circumventing traditional distribution channels will significantly increase the scale of profits. Giant Network's “Operation Supernatural” and Gibbit's “The Legend of Staff and Sword” both achieved sales volume in the third quarter. Combined, they were not connected to the Android intermodal transport channel. The bank expects the profits of these two companies to increase significantly in the third quarter.

AI empowers game development and operational efficiency improvement

Judging from the progress of AI described by various game companies in their financial reports, AI has been widely used in the entire process of game development and operation. Specifically, it can be divided into two categories:

1) AI multi-modality: Mainly used for AI to generate images, videos and 3D materials. ST Huatong increased efficiency by 60%-80% in the mass production process of art creation; 37 Mutual Entertainment used AI to generate more than 80% of 2D art assets during the distribution process, 3D assets accounted for more than 30%, and game advertising material and video accounted for more than 70%.

2) Localized deployment of AI models and tool platforms: Multiple external models are deployed and fine-tuned to make the generated results more accurate. For example, Perfect World developed its own large model smart platform, connected to multiple external models to customize AI agents for various scenarios; 37 Interactive Entertainment built the “Little Seven” agent platform for AI multi-modal generation, code generation, and text creation; and Shenzhou Taiyue and Gibbit have also built customized image generation tools.

Risk warning:

Copyright protection falls short of expectations; the risk that generative AI technology will fall short of expectations; the risk of difficult product development; the risk of product launch delays; the risk of rising marketing purchase costs; the risk of brain loss; the risk of rising labor costs; the risk of policy supervision; and the risk that commercialization capacity falls short of expectations.