Nasdaq

Nasdaq 華爾街日報

華爾街日報Mineralys Therapeutics (MLYS): Reassessing Valuation After JAMA Spotlight on Lorundrostat’s Phase 3 Launch-HTN Trial

Mineralys Therapeutics (MLYS) just got a credibility boost, with its Phase 3 Launch HTN trial of lorundrostat featured in JAMA’s inaugural Research of the Year Roundup, spotlighting its approach to treatment resistant hypertension.

See our latest analysis for Mineralys Therapeutics.

Despite the recent recognition in JAMA, Mineralys’ share price return has cooled in the near term, with a weaker 1 month share price return and modest 3 month share price return. However, its year to date share price return and 1 year total shareholder return still point to powerful, longer term momentum as investors continue to price in lorundrostat’s opportunity.

If this kind of clinical momentum has your attention, it could be a good moment to compare Mineralys with other potential ideas across healthcare stocks and see what else might fit your strategy.

With shares still trading at a sizable discount to analyst targets despite JAMA level validation and pivotal data on the horizon, is Mineralys quietly undervalued, or is the market already baking in lorundrostat’s full commercial potential?

Price to Book of 4.9x: Is it justified?

On a price to book basis, Mineralys looks expensive at 4.9x versus peers, despite the stock trading at 36.02 in the market today.

Price to book compares a company’s market value to its net assets, a common yardstick for early stage and unprofitable biotechs where earnings are not yet meaningful.

For Mineralys, paying a higher multiple than both its direct peers and the broader US Biotechs industry suggests investors are placing a premium on its pipeline and future growth prospects rather than its current balance sheet.

The gap is stark, with Mineralys trading at 4.9x book value compared to a 3.2x peer average and 2.7x for the wider US Biotechs industry. This signals that the market is assigning it a notably richer valuation than typical sector benchmarks.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-book of 4.9x (OVERVALUED)

However, clinical setbacks for lorundrostat, or a risk off rotation from high growth, pre revenue biotechs, could quickly puncture Mineralys’ premium valuation.

Find out about the key risks to this Mineralys Therapeutics narrative.

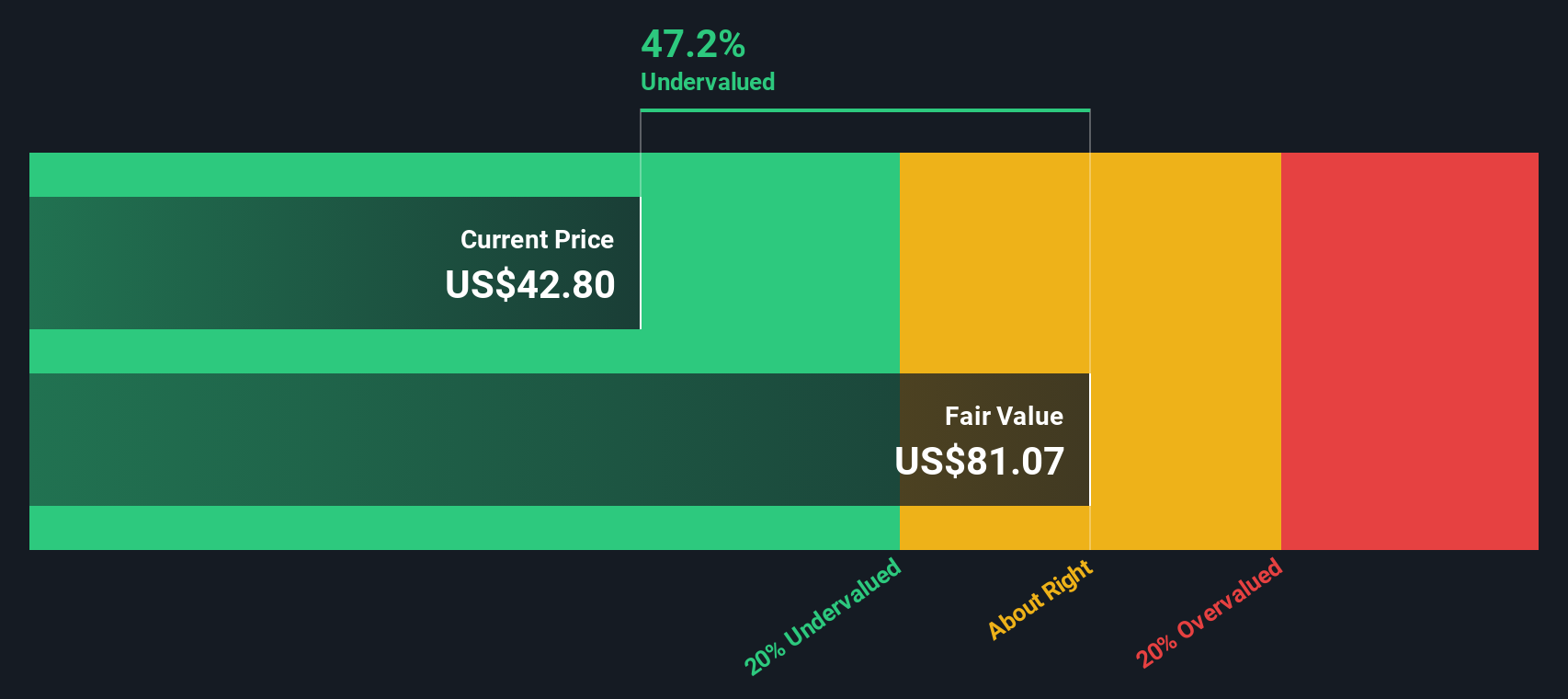

Another View: DCF Points to Deep Value

While the 4.9x price to book ratio suggests Mineralys is expensive against peers, our DCF model paints a very different picture, indicating the shares trade around 57% below an estimated fair value of $84.42. This raises a key question: is the market overpaying on assets, or underestimating future cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Mineralys Therapeutics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 912 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Mineralys Therapeutics Narrative

If you see the numbers differently or want to stress test your own thesis, you can build a custom view in just a few minutes using Do it your way.

A great starting point for your Mineralys Therapeutics research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Ready for more high conviction ideas?

Before you move on, lock in your next watchlist upgrades with hand picked stock ideas tailored to different strategies so real opportunities do not slip past you.

- Capture potential multi baggers early by targeting these 3629 penny stocks with strong financials that already show financial strength instead of just speculative hype.

- Lean into transformational trends by backing these 25 AI penny stocks positioned at the intersection of breakthrough technology and scalable business models.

- Strengthen your portfolio’s foundation with these 13 dividend stocks with yields > 3% that aim to combine reliable income with disciplined capital allocation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com