Nasdaq

Nasdaq 華爾街日報

華爾街日報Has Dycom’s 99% Rally in 2025 Pushed Its Valuation Beyond Fundamentals?

- If you are wondering whether Dycom Industries is still worth buying after such a massive run, you are not alone. This article is going to dig into what that price really implies.

- The stock has climbed 0.7% over the last week, 20.6% over the last month, and is now up an eye catching 98.7% year to date, compounding a 95.4% 1 year gain and a huge 405.3% return over 5 years.

- Much of this momentum reflects growing optimism around long term spending on fiber deployment and network upgrades across North America, with Dycom winning its share of large scale contracts in that space. At the same time, investors are reassessing what that backlog and visibility might be worth in a market that is hungry for infrastructure plays.

- Despite all of that, Dycom currently scores just 0/6 on our valuation checks, which raises some fair questions about how much good news is already priced in. Next we will walk through the main valuation approaches analysts use today and then finish with a more nuanced way to think about the stock's true worth.

Dycom Industries scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Dycom Industries Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today in dollar terms.

For Dycom Industries, the 2 Stage Free Cash Flow to Equity model starts with last twelve month free cash flow of about $283.4 million. It then layers in analyst forecasts through 2027 and extrapolates out to 2035. Those projections see free cash flow easing from around $214.6 million in 2026 to roughly $163.2 million by 2035, reflecting a gradual slowdown rather than rapid long term growth.

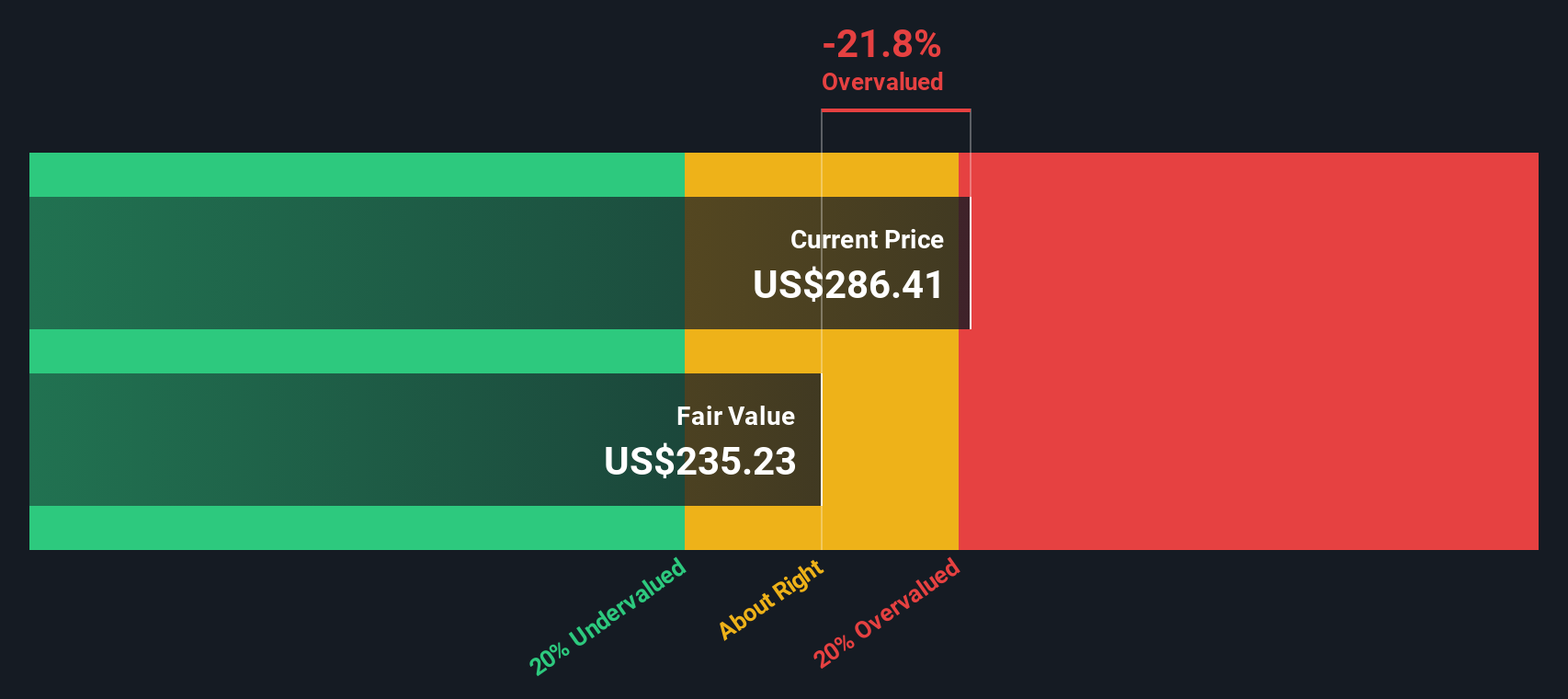

When all those future cash flows are discounted to today, the model arrives at an intrinsic value of about $86.57 per share. Compared with the current market price, the implied intrinsic discount suggests Dycom is roughly 305.7% overvalued, meaning investors are paying far more than the cash flow math supports.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Dycom Industries may be overvalued by 305.7%. Discover 913 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Dycom Industries Price vs Earnings

For a profitable company like Dycom Industries, the price to earnings, or PE, ratio is a practical way to gauge whether investors are paying a reasonable price for each dollar of current profits. In general, faster growing and lower risk businesses can justify a higher PE multiple, while slower growth, more cyclical or riskier names tend to deserve a lower one.

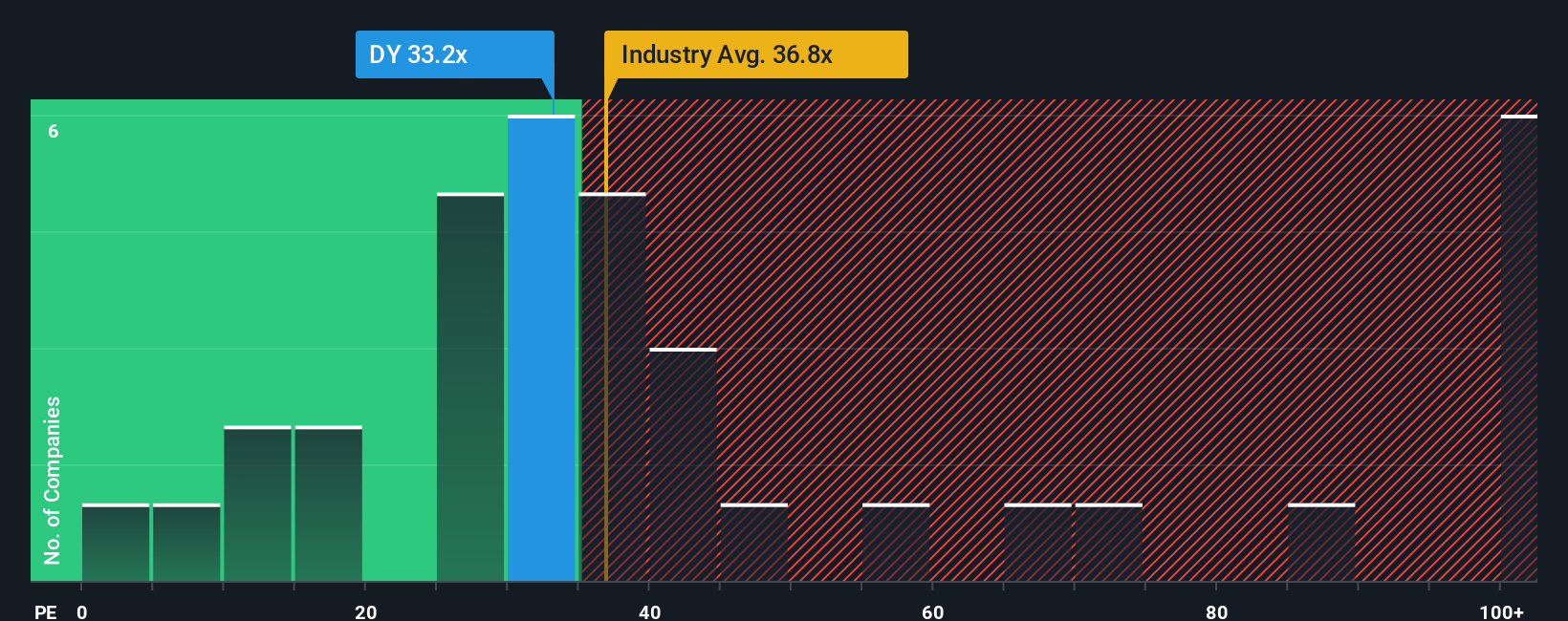

Dycom currently trades on a PE of about 34.2x, which is slightly above the broader Construction industry average of roughly 32.6x and comfortably ahead of its peer group average of around 26.7x. To add more nuance, Simply Wall St calculates a proprietary Fair Ratio for Dycom of 30.4x, which reflects what its PE should be given its earnings growth profile, margins, industry, market cap and risk factors.

This Fair Ratio is more informative than a simple comparison with peers or the industry, because it adjusts for company specific strengths and vulnerabilities rather than assuming all businesses deserve the same multiple. With Dycom trading at 34.2x versus a Fair Ratio of 30.4x, the stock screens as somewhat expensive on an earnings basis.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1455 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Dycom Industries Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple framework that lets you attach a story, your view on Dycom Industries growth, risks and competitive position, to the numbers such as future revenue, earnings, margins and ultimately fair value.

A Narrative links what you believe about a company to a specific financial forecast and then to a clear fair value estimate. On Simply Wall St you can create and compare these Narratives on the Community page, where millions of investors share how their stories translate into numbers.

Once you have a Narrative, the platform continuously compares its Fair Value to Dycom's current share price to help you consider whether today looks more like a buy, hold or sell opportunity. It also automatically refreshes your Narrative when new information like earnings or major news is released.

For Dycom, one bullish Narrative on the Community page might assume high teens revenue growth, expanding margins and a fair value above about $385 per share. A more cautious Narrative could lean on mid single digit growth, flatter margins and a fair value close to the current price, showing how different perspectives can coexist and be tested side by side.

Do you think there's more to the story for Dycom Industries? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com