Nasdaq

Nasdaq 華爾街日報

華爾街日報Why Photronics (PLAB) Is Up 43.1% After Strong Q4 Profit Jump And Upbeat 2026 Outlook

- Earlier in December 2025, Photronics reported fourth-quarter sales of US$215.77 million, slightly below the prior year, while net income and diluted earnings per share from continuing operations increased sharply to US$61.8 million and US$1.07 respectively.

- The company also issued upbeat guidance for the first quarter of fiscal 2026, projecting revenues between US$217 million and US$225 million and signaling confidence backed by high-end integrated circuit demand and ongoing capacity expansion in the U.S. and Korea.

- We’ll now examine how Photronics’ stronger profitability and confident first-quarter 2026 revenue outlook could reshape its investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Photronics Investment Narrative Recap

To own Photronics, you need to believe high-end photomask demand for AI, data centers and advanced ICs will keep supporting healthy margins despite cyclical swings and geopolitical uncertainty. The latest quarter’s sharp profit improvement, together with solid Q1 2026 revenue guidance, reinforces the near term earnings catalyst but does not fully remove the key risk that elevated capital spending could become a drag if demand falters.

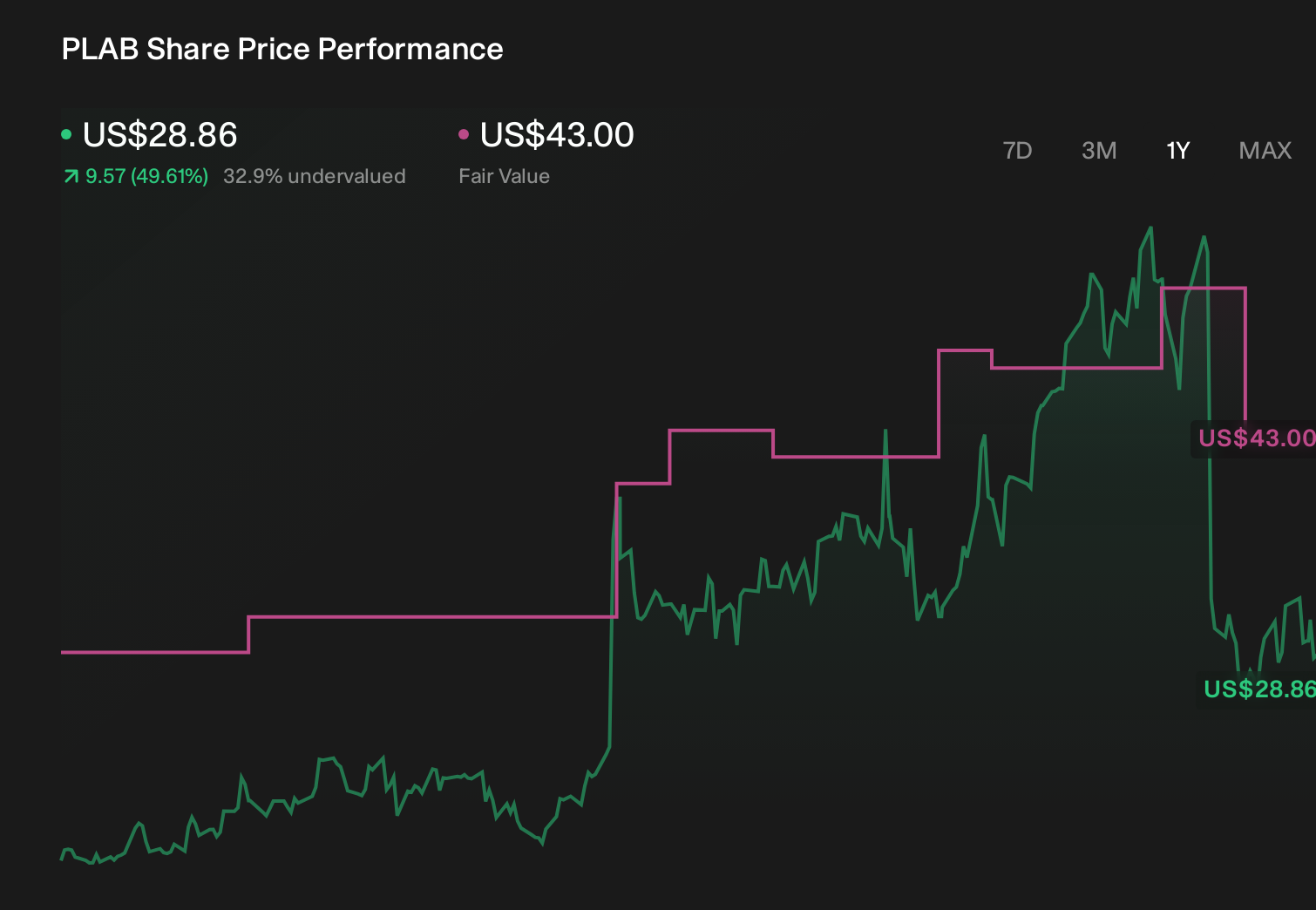

The most relevant update is Photronics’ Q1 fiscal 2026 revenue outlook of US$217 million to US$225 million, which directly links to the short term catalyst of high-end IC demand and utilization of new capacity in the U.S. and Korea. This guidance, following a quarter where sales dipped but profits jumped, puts more attention on whether that new capacity can be filled consistently enough to justify ongoing heavy investment.

Yet investors should also be aware that if those high capital expenditures do not translate into sustained revenue growth...

Read the full narrative on Photronics (it's free!)

Photronics’ narrative projects $950.2 million revenue and $131.6 million earnings by 2028. This requires 3.5% yearly revenue growth and a $23.1 million earnings increase from $108.5 million today.

Uncover how Photronics' forecasts yield a $40.50 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Seven individual fair value estimates from the Simply Wall St Community span roughly US$19.25 to US$40.50, showing how far apart private investors can be. You can weigh those views against the near term earnings catalyst from high-end IC demand and the risk that heavy capex strains cash flow if conditions soften.

Explore 7 other fair value estimates on Photronics - why the stock might be worth 48% less than the current price!

Build Your Own Photronics Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Photronics research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Photronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Photronics' overall financial health at a glance.

No Opportunity In Photronics?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 35 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com