Nasdaq

Nasdaq 華爾街日報

華爾街日報A Fresh Look at W.W. Grainger’s (GWW) Valuation After Its Recent Share Price Rebound

W.W. Grainger (GWW) has quietly pushed higher in recent weeks, with the stock up about 7% over the past week and roughly 11% in the past month after a tough start to the year.

See our latest analysis for W.W. Grainger.

That bounce has only partly repaired the damage from earlier in the year, with the year to date share price return still slightly negative and the 1 year total shareholder return in the red. However, multi year total shareholder returns remain very strong, suggesting long term momentum is intact even as near term sentiment improves.

If Grainger’s move has you rethinking your watchlist, this could be a good moment to explore fast growing stocks with high insider ownership and see what other fast moving names are building momentum.

With shares still below their highs but only a small discount to analyst targets, investors face a key question: is Grainger now a rare value in a quality compounder, or has the market already priced in its future growth?

Most Popular Narrative: 2.3% Undervalued

With W.W. Grainger last closing at $1029.56 against a narrative fair value of about $1053.47, the story leans toward a modest upside built on steady execution rather than explosive growth.

The acceleration of digital transformation in B2B or industrial commerce is expanding the addressable market for Grainger's online platforms (especially Zoro and MonotaRO), driving faster than industry top line gains, operating leverage, and margin expansion as e commerce penetration rises.

Want to see what kind of revenue runway and profit profile could support this premium? The narrative leans on disciplined growth, sticky margins, and a punchy future earnings multiple. Curious how those ingredients combine to justify today’s price and a little more? Read on to see the full playbook behind that fair value view.

Result: Fair Value of $1053.47 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that playbook could be derailed if MRO demand stays muted, or if rising input costs and pricing pressure squeeze margins more than expected.

Find out about the key risks to this W.W. Grainger narrative.

Another Lens on Value

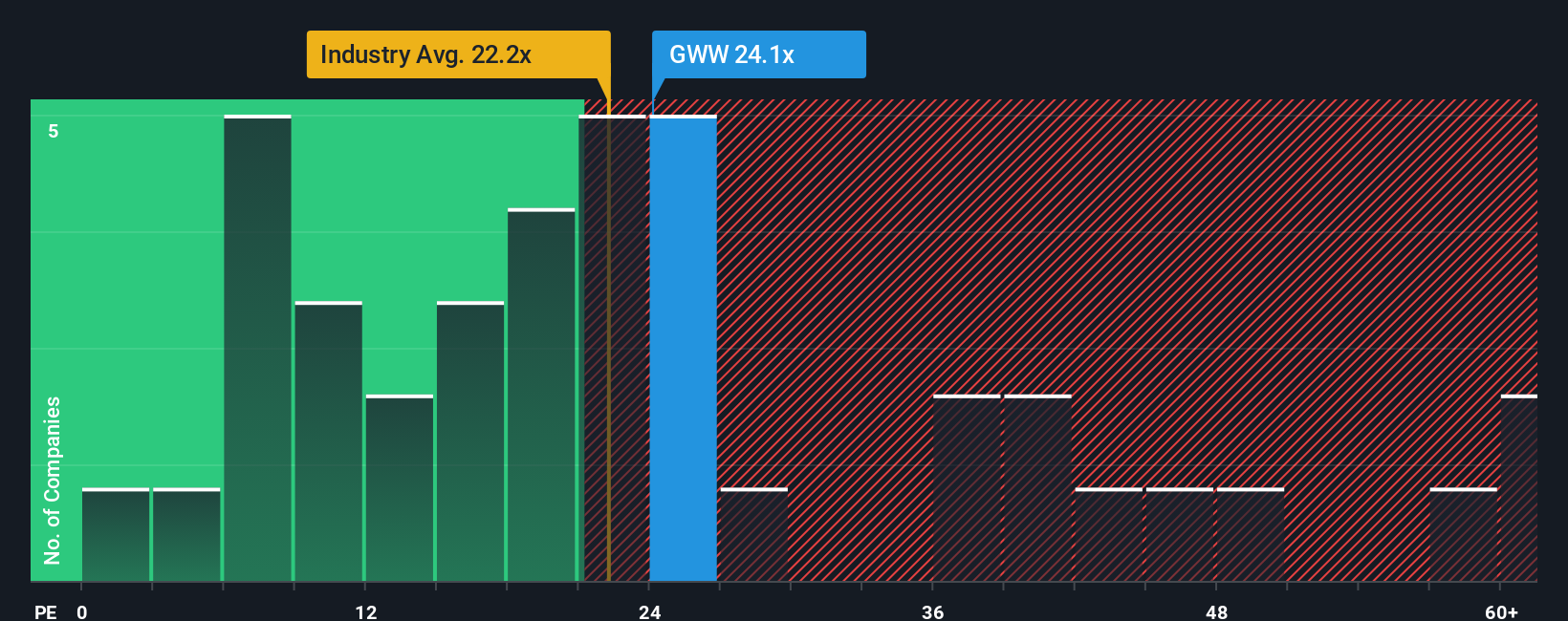

On earnings, the picture looks less forgiving. Grainger trades at about 28.3 times earnings, richer than both peers at 22.6 times and the US Trade Distributors industry at 19.9 times, and even above its own 28.1 times fair ratio. This hints at valuation risk if growth underwhelms.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own W.W. Grainger Narrative

If this perspective does not quite fit your view, or you would rather dive into the numbers yourself, you can build a custom narrative in just a few minutes, Do it your way.

A great starting point for your W.W. Grainger research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Ready for more investment ideas?

Before you close this tab, put Simply Wall Street’s Screener to work and lock in a watchlist of fresh opportunities other investors may be overlooking.

- Capture potential upside by targeting quality companies trading below intrinsic value using these 908 undervalued stocks based on cash flows that highlight mispriced cash flow opportunities.

- Position yourself for the next technological wave by scanning these 26 AI penny stocks that are building businesses around artificial intelligence innovation.

- Focus on potential income by looking at reliable payers through these 13 dividend stocks with yields > 3% that combine yield with solid underlying fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com