Nasdaq

Nasdaq 華爾街日報

華爾街日報Murata Manufacturing (TSE:6981) Valuation After New SiC-Optimized High-Voltage MLCC Enters Mass Production

Murata Manufacturing (TSE:6981) just moved its next generation high voltage MLCC into mass production, a quiet but meaningful step for investors tracking the shift to SiC based power systems and EV hardware.

See our latest analysis for Murata Manufacturing.

The market seems to be noticing these moves, with a roughly mid teens 1 month share price return and a strong double digit year to date share price return supported by healthy multi year total shareholder returns. This signals building momentum rather than a short lived spike.

If Murata’s trajectory around EV and intelligent systems has your attention, this is also a good moment to discover other high growth tech and AI stocks that could benefit from similar structural trends.

With earnings growing solidly, a fresh SiC focused product cycle, and shares now trading only slightly below analyst targets, the real question is whether Murata still offers mispriced upside or if the market has already discounted the next leg of growth.

Price-to-Earnings of 26.2x: Is it justified?

Murata’s current valuation rests on a price-to-earnings ratio of 26.2 times, with the share price at ¥3,400 and trading modestly below some fair value estimates.

The price-to-earnings multiple compares what investors pay today with the company’s current earnings. This is a key lens for established, profitable tech hardware names like Murata. For a business with improving margins, accelerating earnings and exposure to structural themes in EVs and high performance computing, a richer multiple can indicate that investors are willing to pay more for what they view as more predictable profit growth.

Relative to its closest peer set, Murata actually looks restrained. Its 26.2 times earnings multiple sits well below the 43.8 times peer average, suggesting the market is not fully pricing its recent profit acceleration. However, compared with the broader Japanese electronic industry, the same 26.2 times earnings looks punchy versus an average of 15.2 times and slightly ahead of an estimated fair price-to-earnings ratio of 25.5 times. This is a level the market could gravitate toward if growth expectations cool.

Explore the SWS fair ratio for Murata Manufacturing

Result: Price-to-Earnings of 26.2x (ABOUT RIGHT)

However, softening EV demand or slower adoption of SiC power systems could delay Murata’s growth inflection, especially if competitors ramp high performance MLCC capacity more quickly.

Find out about the key risks to this Murata Manufacturing narrative.

Another View on Value

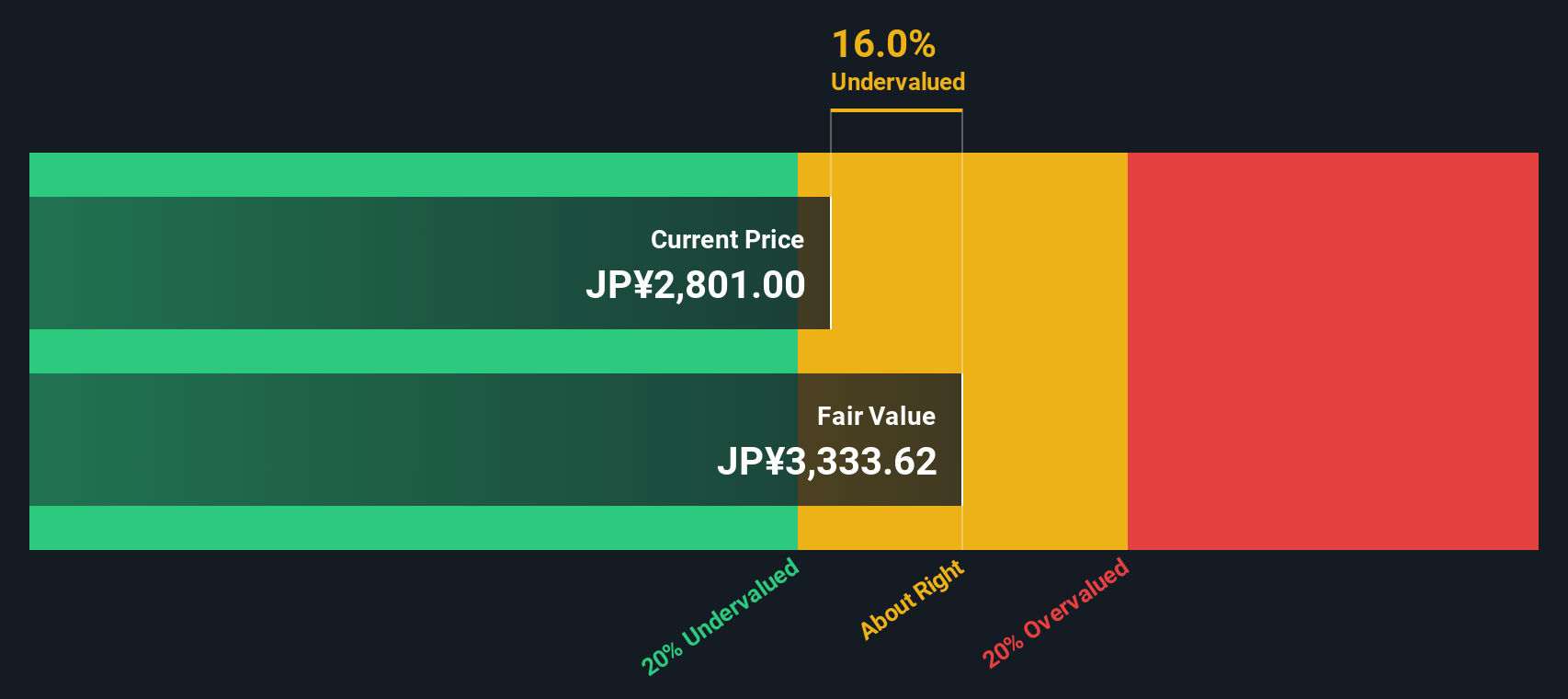

Our SWS DCF model paints a more generous picture, suggesting Murata is trading about 10% below its fair value of roughly ¥3,790. That points to upside even after the rerating, but only if earnings and cash flows track the model’s steady growth path. Will they?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Murata Manufacturing for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 908 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Murata Manufacturing Narrative

If you see the numbers differently or want to challenge these assumptions, you can quickly build your own view in just a few minutes: Do it your way.

A great starting point for your Murata Manufacturing research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for your next investment move?

Do not stop at one opportunity. Use the Simply Wall Street Screener to pinpoint new ideas that match your risk appetite, income goals, and growth ambitions.

- Capture early stage growth potential with these 3614 penny stocks with strong financials that already back their stories with solid financial foundations.

- Target structural tailwinds in automation and data by screening for these 26 AI penny stocks positioned at the heart of the AI build out.

- Lock in attractive entry points using these 908 undervalued stocks based on cash flows to spot quality businesses trading below what their cash flows suggest they are worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com