Nasdaq

Nasdaq 華爾街日報

華爾街日報Allied Properties REIT (TSX:AP.UN): Reassessing Valuation After the December 2025 Distribution Cut

Allied Properties Real Estate Investment Trust (TSX:AP.UN) just trimmed its monthly distribution, declaring CA$0.06 per unit for December 2025, payable January 15, 2026. This move puts its cash flow strategy under the microscope.

See our latest analysis for Allied Properties Real Estate Investment Trust.

The distribution cut comes after a tough stretch, with a roughly 35 percent 3 month share price return and 23 percent year to date share price return both negative, while the 5 year total shareholder return of about 48 percent in the red shows how long term momentum has faded.

If this move has you rethinking income focused REITs, it could be a good moment to scan the broader market for resilience and growth via fast growing stocks with high insider ownership.

With units trading well below past levels but still facing weak long term returns and a recent distribution cut, is Allied now a mispriced turnaround story, or is today’s lower valuation simply reflecting muted growth ahead?

Price-to-Sales of 3.1x: Is it justified?

On a price-to-sales basis, Allied Properties Real Estate Investment Trust trades at 3.1 times revenue, which screens as expensive versus both peers and its implied fair level.

The price-to-sales ratio compares the market value of each unit to the revenue the trust generates. It is a common yardstick for real estate vehicles where earnings can be volatile or currently negative. For Allied, this richer multiple suggests investors are still paying up for its portfolio of urban workspaces and potential future profit recovery, despite the trust being unprofitable and carrying weaker coverage of interest and distributions.

That premium becomes clearer when set against benchmarks. The 3.1 times sales valuation sits well above the North American Office REIT industry average of 2.1 times and also above the peer group average of 1.6 times. This indicates the market is assigning Allied a noticeably higher revenue multiple than comparable names. It also exceeds the estimated fair price-to-sales ratio of 2.5 times, a level our models indicate the market could ultimately gravitate toward if sentiment or growth expectations ease.

Explore the SWS fair ratio for Allied Properties Real Estate Investment Trust

Result: Price-to-sales of 3.1x (OVERVALUED)

However, lingering losses and a recent distribution cut could still pressure sentiment if leasing conditions soften further or interest costs climb faster than expected.

Find out about the key risks to this Allied Properties Real Estate Investment Trust narrative.

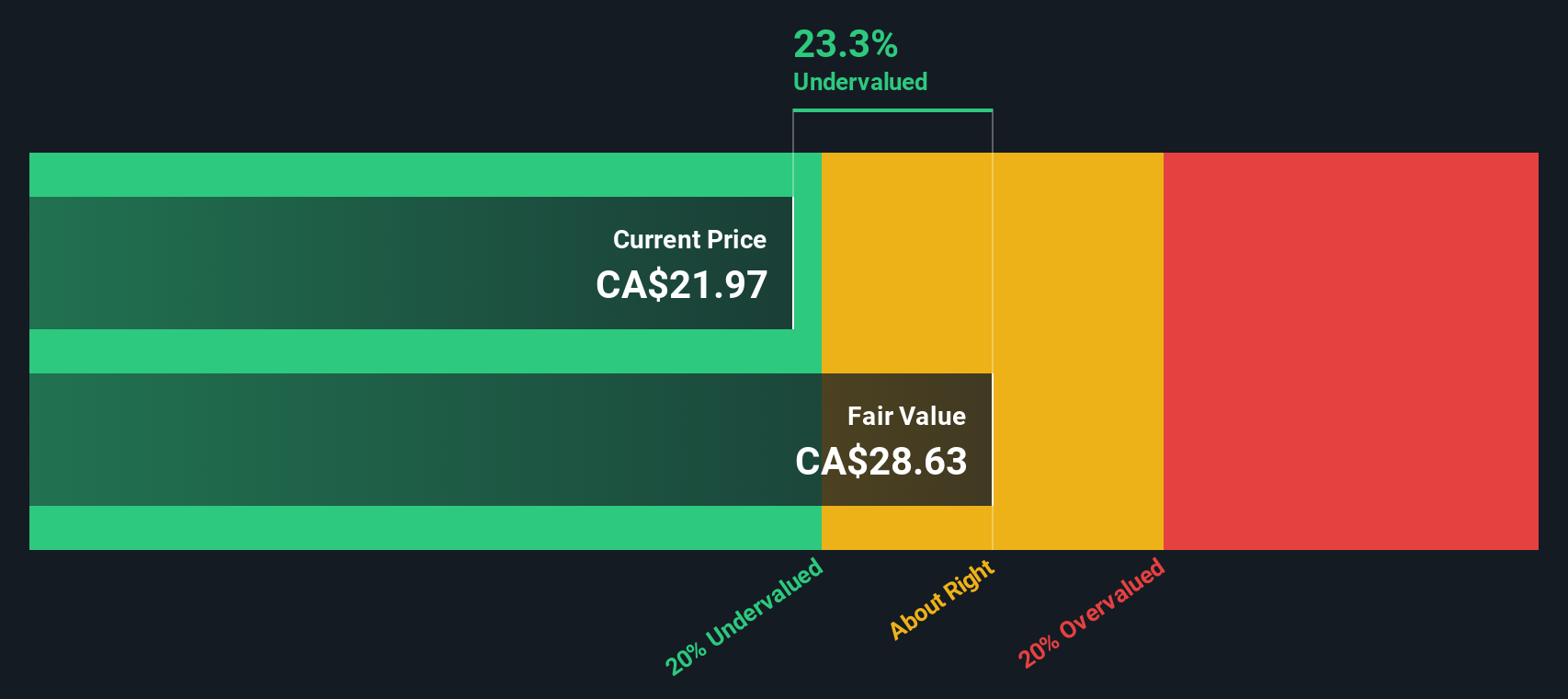

Another View: DCF Suggests Deep Value

Our DCF model paints a different picture, with Allied trading about 43 percent below its estimated fair value of roughly CA$23.24 per unit. If cash flows normalise as forecast, today’s beaten down price could represent an opportunity rather than a warning. It is also worth considering whether the model may be too optimistic about recovery.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Allied Properties Real Estate Investment Trust for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 908 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Allied Properties Real Estate Investment Trust Narrative

If you see the story differently or want to dig into the numbers yourself, you can quickly build a tailored view in just a few minutes: Do it your way.

A great starting point for your Allied Properties Real Estate Investment Trust research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more high conviction ideas?

If Allied sparks your interest, do not stop here. Use the Simply Wall Street Screener to uncover fresh, data driven ideas before other investors notice.

- Capture early stage growth potential by scanning these 3612 penny stocks with strong financials that already show solid underlying fundamentals instead of relying on hype alone.

- Position your portfolio at the heart of the digital transformation by reviewing these 30 healthcare AI stocks reshaping patient care, diagnostics, and efficiency.

- Seek more predictable income streams by targeting these 13 dividend stocks with yields > 3% that combine attractive yields with sustainable payout profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com