Nasdaq

Nasdaq 華爾街日報

華爾街日報Toyota Boshoku (TSE:3116) Valuation Check After Launching Its First Smart Plant in Hopkinsville, Kentucky

Toyota Boshoku (TSE:3116) just flipped the switch on its first smart plant in Hopkinsville, Kentucky, a new US hub for advanced seat frame components that could quietly reshape its growth story.

See our latest analysis for Toyota Boshoku.

That Hopkinsville smart plant launch comes on the back of solid momentum, with a year to date share price return of 22.8 percent and a 1 year total shareholder return of 29.08 percent suggesting investors are warming to Toyota Boshoku’s growth and execution story.

If this expansion has you thinking more broadly about autos, it could be a good moment to scout other opportunities among auto manufacturers as potential additions to your watchlist.

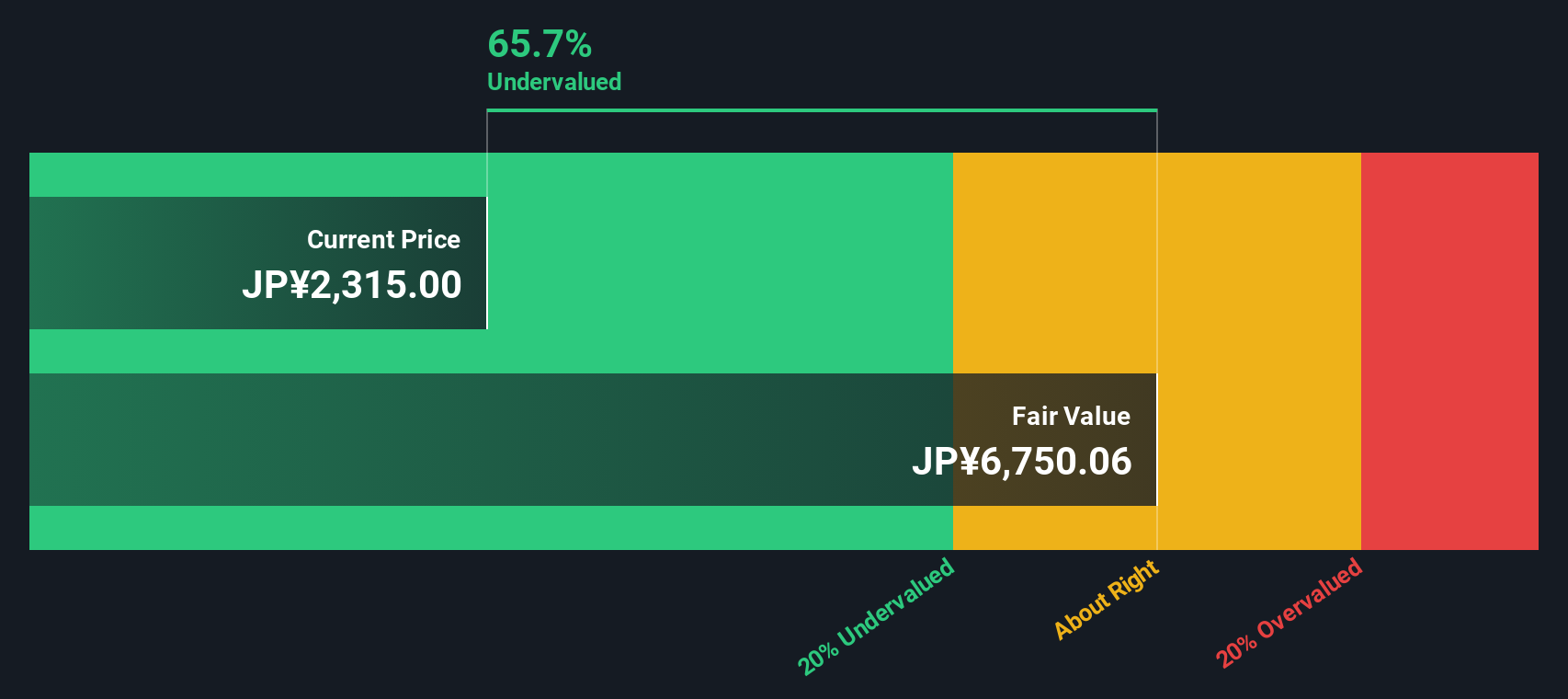

Yet with shares up strongly and trading only modestly below analyst targets, even as intrinsic value models imply a steep discount, the key question now is simple: is Toyota Boshoku still a buy, or is future growth already priced in?

Price-to-Earnings of 21.4x: Is it justified?

Toyota Boshoku last closed at ¥2475, and on 21.4 times earnings it screens as expensive versus peers despite our DCF work implying deep undervaluation.

The price to earnings multiple compares the share price to the company’s per share earnings, making it a quick gauge of how much investors are paying for current profits.

In Toyota Boshoku’s case, the market appears willing to pay up for future earnings growth, but that optimism sits awkwardly alongside a large recent one off loss and currently thin 1 percent profit margins.

The premium looks stark when set against the Japan Auto Components industry average of 9.9 times and an estimated fair price to earnings ratio of 16.1 times. This is a level the multiple could gravitate toward if expectations cool or earnings fail to accelerate as forecast.

Explore the SWS fair ratio for Toyota Boshoku

Result: Price-to-Earnings of 21.4x (OVERVALUED)

However, thin 1 percent margins and any stumble in ramping the Hopkinsville smart plant could quickly sour sentiment on Toyota Boshoku’s premium valuation.

Find out about the key risks to this Toyota Boshoku narrative.

Another Way to Look at Value

Our DCF model paints a very different picture to the rich 21.4 times earnings multiple, implying Toyota Boshoku could be deeply undervalued relative to its future cash flows rather than expensive. Is the market mispricing that long term potential, or is the model too optimistic?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Toyota Boshoku for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 908 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Toyota Boshoku Narrative

If you see the numbers differently or want to dig into the details yourself, you can build a custom view in just minutes. Do it your way

A great starting point for your Toyota Boshoku research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Ready for more investment ideas?

Before you move on, put Simply Wall St to work for you and lock in a shortlist of compelling, data backed stock ideas tailored to your strategy.

- Target potential multi baggers by scanning these 3611 penny stocks with strong financials that pair smaller market caps with solid underlying fundamentals.

- Capitalize on transformative tech trends by reviewing these 26 AI penny stocks positioned at the frontier of artificial intelligence innovation.

- Lock in value focused opportunities by filtering for these 908 undervalued stocks based on cash flows that trade below what their cash flows suggest they are worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com