Nasdaq

Nasdaq 華爾街日報

華爾街日報Has Xiaomi’s 291% Three Year Surge Left Much Upside for 2025?

- If you are wondering whether Xiaomi is still a smart buy after its big run, or if the easy money has already been made, you are not alone. This breakdown is here to tackle exactly that question.

- The stock is up 26.4% year to date and 37.0% over the last year, with a 291.3% gain over three years. However, the last 30 days saw a modest 1.2% pullback after a flat 0.4% move this past week.

- Recent moves have been shaped by optimism around Xiaomi's push deeper into premium smartphones and ecosystem hardware, alongside growing investor interest in its longer term Internet of Things and services strategy. At the same time, shifting sentiment on Chinese tech regulation and global supply chains has kept volatility elevated and made the market more sensitive to headlines.

- Despite that excitement, Xiaomi only scores a 1/6 valuation check. This suggests the market might already be pricing in a lot of good news. Next, we will unpack how different valuation methods view the stock, and later on return to a more nuanced way of thinking about what Xiaomi is really worth.

Xiaomi scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Xiaomi Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow model estimates what a business is worth today by projecting the cash it can generate in the future and then discounting those amounts back into today’s money.

For Xiaomi, the latest twelve month Free Cash Flow is about CN¥43.5 billion. Analysts provide detailed forecasts for the next few years, and after that Simply Wall St extrapolates longer term trends. Under this two stage Free Cash Flow to Equity approach, Xiaomi’s cash flows are expected to rise steadily, reaching roughly CN¥71.6 billion by 2029 and remaining in that ballpark through 2035 as growth gradually slows.

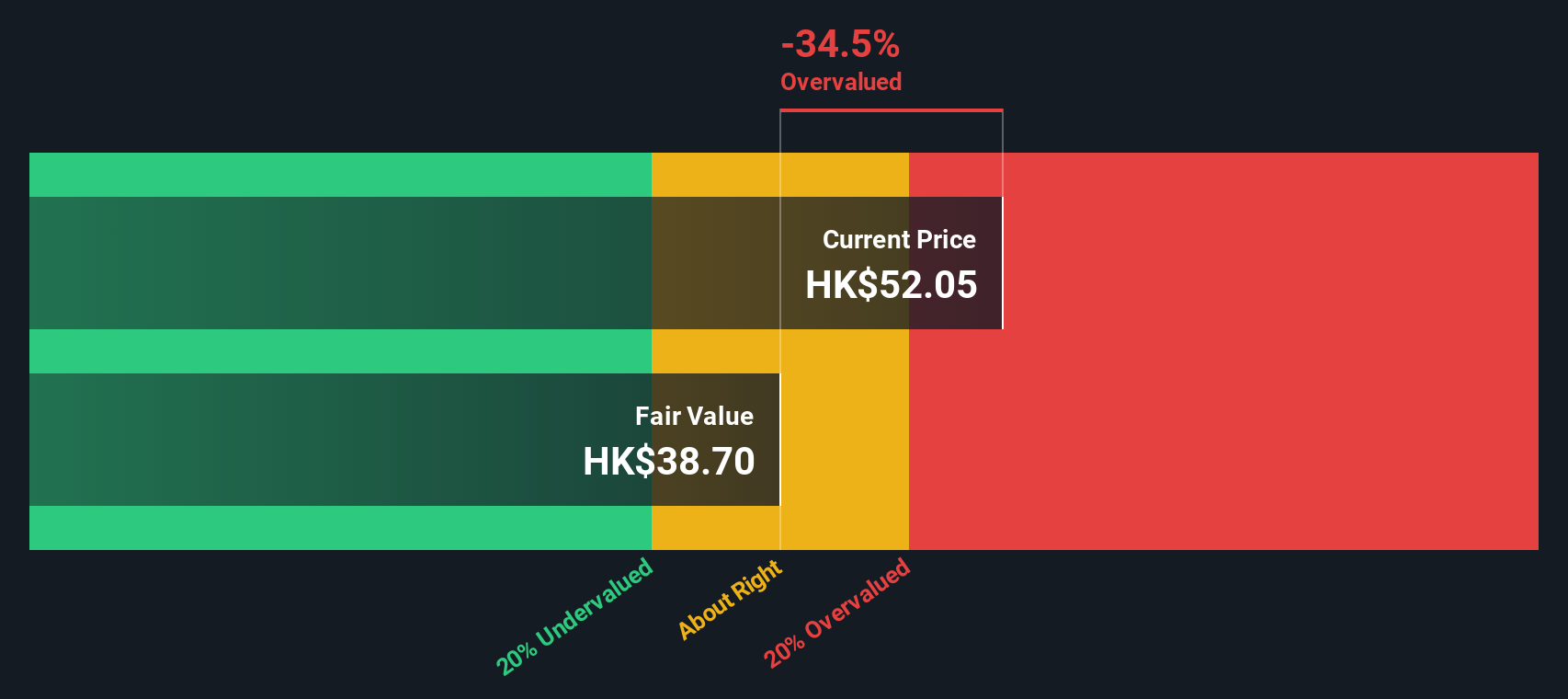

When these future cash flows are discounted back, the model arrives at an intrinsic value of around HK$45.77 per share. That implies the stock trades at about a 6.1% discount to its estimated fair value, which is a relatively small margin of safety but still leans positive. In plain terms, the DCF suggests Xiaomi is priced pretty close to what its long term cash generation appears to justify.

Result: ABOUT RIGHT

Xiaomi is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Xiaomi Price vs Earnings

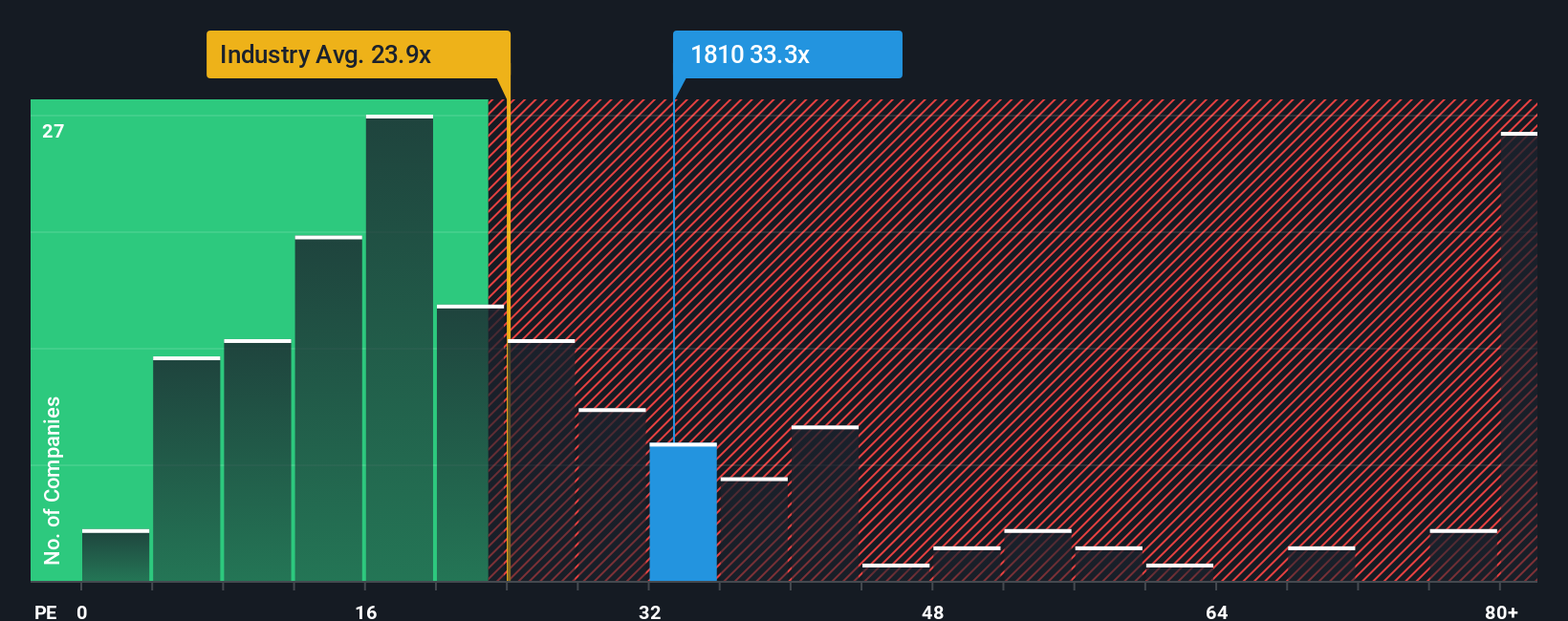

For profitable companies like Xiaomi, the price to earnings ratio is a useful way to judge valuation because it directly links what investors pay today to the profits the business is already generating. A higher PE can be justified when earnings are expected to grow quickly or when the business is seen as lower risk. Slower growth or higher uncertainty typically call for a lower, more conservative multiple.

Xiaomi currently trades on about 22.9x earnings, slightly above the broader Tech industry average of roughly 22.7x and well above the peer group average near 17.1x. On the surface, that suggests the market is willing to pay a premium for Xiaomi compared to many rivals. However, Simply Wall St’s proprietary Fair Ratio for Xiaomi is 20.5x, which adjusts the multiple you would expect to pay after accounting for its specific earnings growth outlook, profitability, industry positioning, size and risk profile. This tailored Fair Ratio is more informative than simple peer or industry comparisons because it captures Xiaomi’s individual strengths and risk factors rather than assuming all tech stocks deserve the same multiple. With the current 22.9x PE sitting modestly above the 20.5x Fair Ratio, the stock screens as somewhat expensive on this measure.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Xiaomi Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. Simply Wall St hosts these on the Xiaomi Community page, and millions of investors already use them as an easy way to connect a company’s story to its numbers.

A Narrative is your own clear view of where a business is heading, expressed as a short story about its competitive advantages, risks and catalysts, and then translated into concrete forecasts for future revenue, earnings, margins and a resulting fair value estimate.

In practice, a Narrative links three pieces together: what you believe Xiaomi’s business will look like, what that implies for a financial forecast, and what that forecast suggests is a reasonable fair value per share.

Because Simply Wall St continuously refreshes Narratives when new information such as earnings, guidance or major news is released, your Xiaomi view, and therefore your fair value, stays dynamic instead of being a once-a-year exercise.

For example, one Xiaomi Narrative on the platform might assume a fair value of about HK$51.80, while a more optimistic one might point to roughly HK$58.00. Comparing each Narrative’s fair value to the current market price gives its author a clear, numbers-backed signal on whether they think Xiaomi is a buy, hold or sell today.

Do you think there's more to the story for Xiaomi? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com