Nasdaq

Nasdaq 華爾街日報

華爾街日報Will Activist Pressure and Board Changes Shift BILL Holdings' (BILL) Profitability Playbook?

- At its December 11, 2025 annual meeting, BILL Holdings' shareholders approved the appointment of finance executive Natalie Derse to the board of directors.

- Her addition comes just days after activist investor Barington Capital pressed the board to cut costs and evaluate all strategic options amid concerns over profitability and business momentum.

- We’ll now explore how Barington Capital’s push for cost reductions and a potential strategic review could reshape BILL Holdings’ investment narrative.

We've found 13 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

BILL Holdings Investment Narrative Recap

To own BILL, you need to believe its B2B financial automation platform can convert strong transaction growth into durable, profitable economics despite recent share price weakness and macro-sensitive SMB volumes. The Barington letter raises the odds that near term cost discipline and a formal strategic review become the key catalysts, while the biggest risk remains that slower customer spending and mix shifts pressure transaction revenue and delay a clean, sustainable move into solid profitability. Overall, the Derse appointment itself is not a material change.

Among recent updates, the Reuters report that BILL is exploring a potential sale, with activists already on the register, is most closely tied to Barington’s call for “all strategic alternatives.” Any formal process or outcome could interact directly with the same catalysts and risks investors are already weighing around cost structure, competitive positioning, and how quickly the company can translate its AI and embedded finance initiatives into consistent earnings power.

Yet while potential strategic options may sound attractive, investors should also be aware of...

Read the full narrative on BILL Holdings (it's free!)

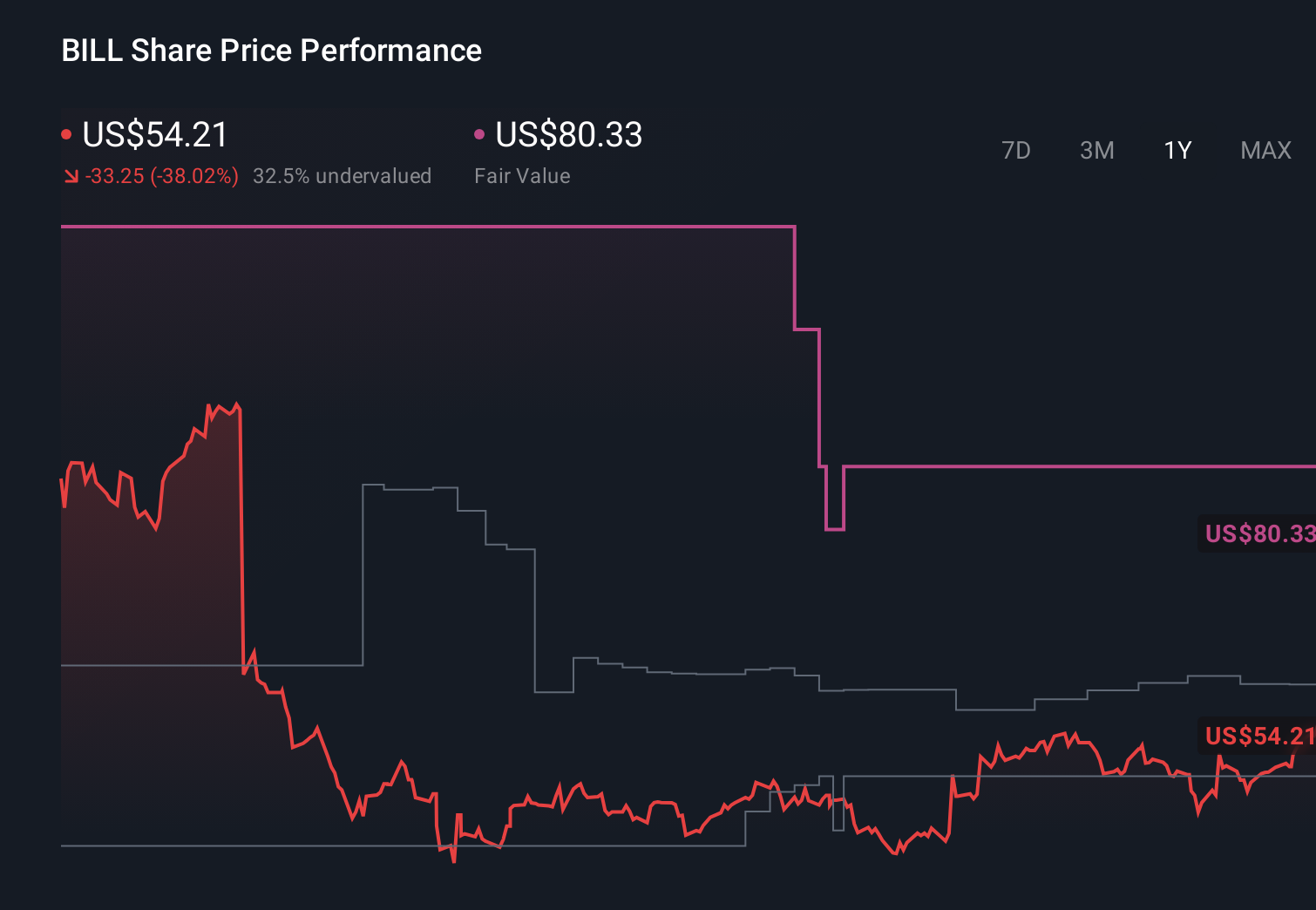

BILL Holdings’ narrative projects $2.1 billion revenue and $94.8 million earnings by 2028. This requires 13.2% yearly revenue growth and a $71.0 million earnings increase from $23.8 million today.

Uncover how BILL Holdings' forecasts yield a $60.86 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community currently value BILL between US$42 and about US$91.78 per share, reflecting a wide spread of expectations. When you set those alongside the risk that softer SMB spending could drag on transaction volumes and delay margin improvement, it becomes clear why it helps to compare several different views before forming your own.

Explore 5 other fair value estimates on BILL Holdings - why the stock might be worth 23% less than the current price!

Build Your Own BILL Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your BILL Holdings research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free BILL Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate BILL Holdings' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com