Nasdaq

Nasdaq 華爾街日報

華爾街日報Is SMIC’s 133% 2025 Surge Still Justified by Cash Flow and Earnings Expectations?

- If you have been wondering whether Semiconductor Manufacturing International is still a smart buy after its huge run up, you are not alone. This stock has become a lightning rod for debates about value versus momentum.

- Despite a recent pullback of around 2.9% over the last week and 7.6% over the last month, the shares are still up an eye catching 133.4% year to date and about 161.4% over the past year, which naturally raises questions about how much upside might be left.

- These moves have unfolded against a backdrop of heightened global interest in domestic Chinese chip production, ongoing technology export restrictions, and policy support aimed at building a homegrown semiconductor ecosystem. Together, those forces have helped shift investor perception of the company from a cyclical foundry play to a strategic national asset, which can change how the market is willing to value it.

- Yet on our framework the stock currently scores just 0 out of 6 on valuation checks. In the sections that follow we will unpack what different valuation methods say about that score and hint at a more nuanced way to think about fair value that we will come back to at the end.

Semiconductor Manufacturing International scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Semiconductor Manufacturing International Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth today by projecting its future cash flows and discounting them back to the present using a required rate of return.

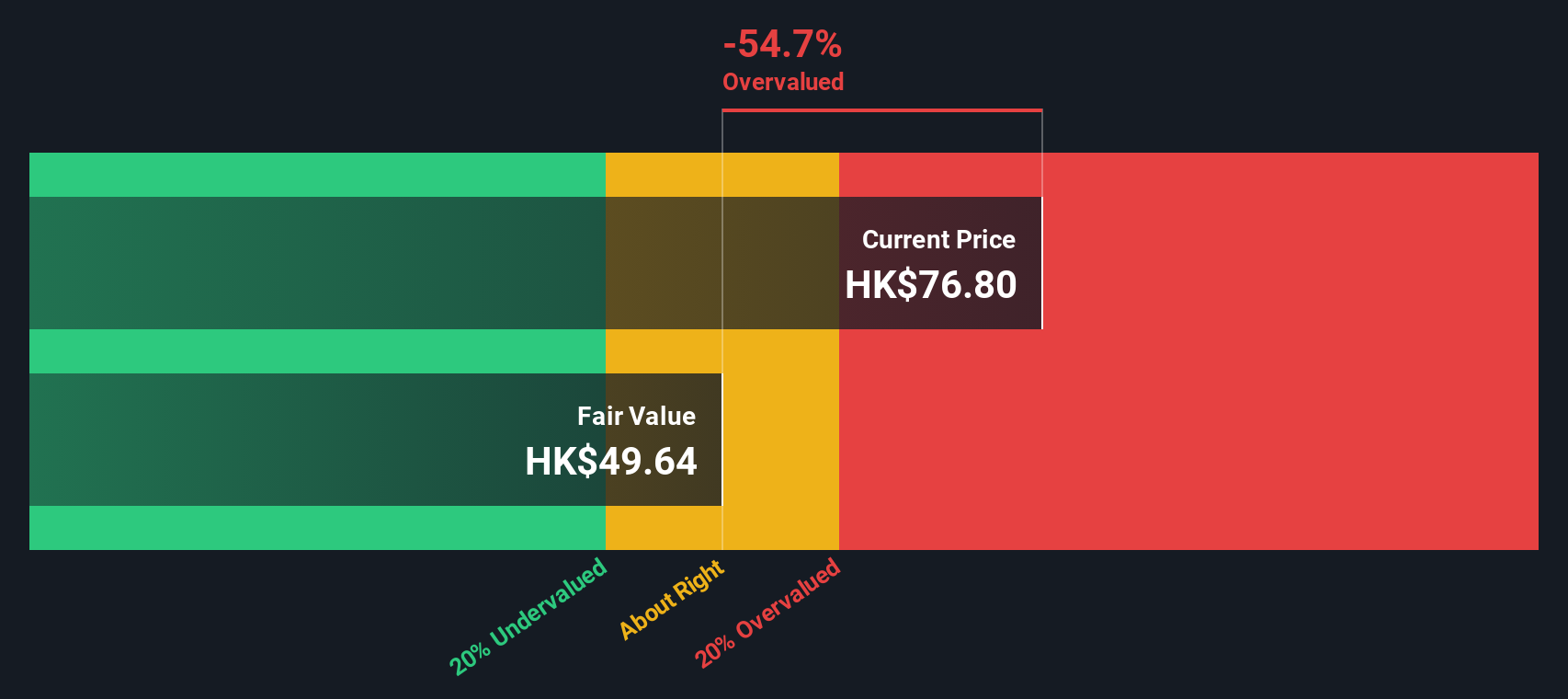

For Semiconductor Manufacturing International, the latest twelve month free cash flow is roughly $5.9 Billion in the red, indicating heavy ongoing investment. Analyst and extrapolated forecasts, however, assume this will swing into positive territory over the next few years, rising to about $2.9 Billion by 2029 and continuing to grow through 2035. The model used here is a 2 Stage Free Cash Flow to Equity approach, where nearer term estimates are based on analyst projections and the following years are extrapolated by Simply Wall St.

On this basis, the intrinsic value comes out at roughly HK$35.93 per share. Compared with the current market price, the DCF suggests the stock is about 88.4% overvalued, implying that investors are paying a very full price for expected future growth.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Semiconductor Manufacturing International may be overvalued by 88.4%. Discover 907 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Semiconductor Manufacturing International Price vs Earnings

For profitable companies, the Price to Earnings ratio is often the go to yardstick because it ties what you pay directly to the profits the business is generating today. It also intuitively connects to investors expectations, since faster growing and less risky companies typically command higher PE multiples, while slower growth or higher uncertainty usually warrants a lower, more conservative multiple.

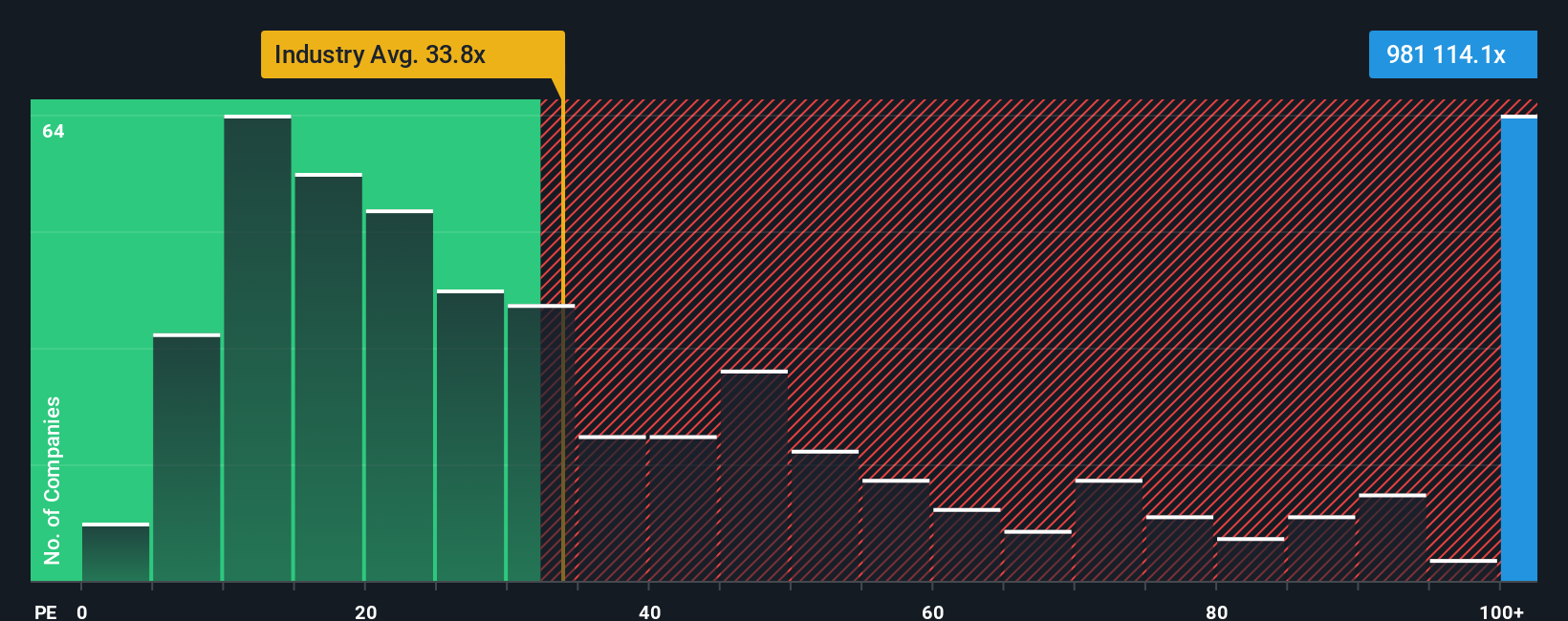

Semiconductor Manufacturing International currently trades on about 112.23x earnings. That is far richer than both the broader Semiconductor industry average of around 34.70x and the closer peer group, which sits near 28.68x. On those simple comparisons alone, the stock screens as expensive. However, Simply Wall St also uses a Fair Ratio, a proprietary estimate of what a reasonable PE multiple should be after adjusting for the company s earnings growth outlook, profitability, risk profile, industry characteristics and size.

This Fair Ratio for Semiconductor Manufacturing International is 41.27x, which remains well below the actual PE of 112.23x. Because the market multiple is significantly higher than what the fundamentals would typically justify on this framework, the shares still look meaningfully overvalued on a PE basis.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1448 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Semiconductor Manufacturing International Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives, an approach where you write a simple story about what you think will happen to a company and connect that story directly to forecasts for revenue, earnings, margins and ultimately a fair value estimate.

On Simply Wall St's Community page, used by millions of investors, a Narrative is an easy and accessible tool that links three things together: your view of the business, a quantified financial forecast that reflects that view, and the implied fair value you believe is reasonable given those assumptions.

Because each Narrative automatically compares its Fair Value to the current share price, it becomes a practical guide for deciding whether Semiconductor Manufacturing International looks like a buy, a hold, or a sell. It also updates dynamically as new information, such as earnings or major news, flows into the platform.

For example, one Semiconductor Manufacturing International Narrative might assume resilient domestic demand and improving margins, and assign a fair value near HK$71.60. A more cautious Narrative could focus on overcapacity, pricing pressure and China concentration, and arrive at a fair value closer to HK$20.00. Yet both are transparent, data linked stories you can inspect, adjust and compare to your own view.

Do you think there's more to the story for Semiconductor Manufacturing International? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com