Nasdaq

Nasdaq 華爾街日報

華爾街日報Is Enel Chile (SNSE:ENELCHILE) A Risky Investment?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Enel Chile S.A. (SNSE:ENELCHILE) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Enel Chile Carry?

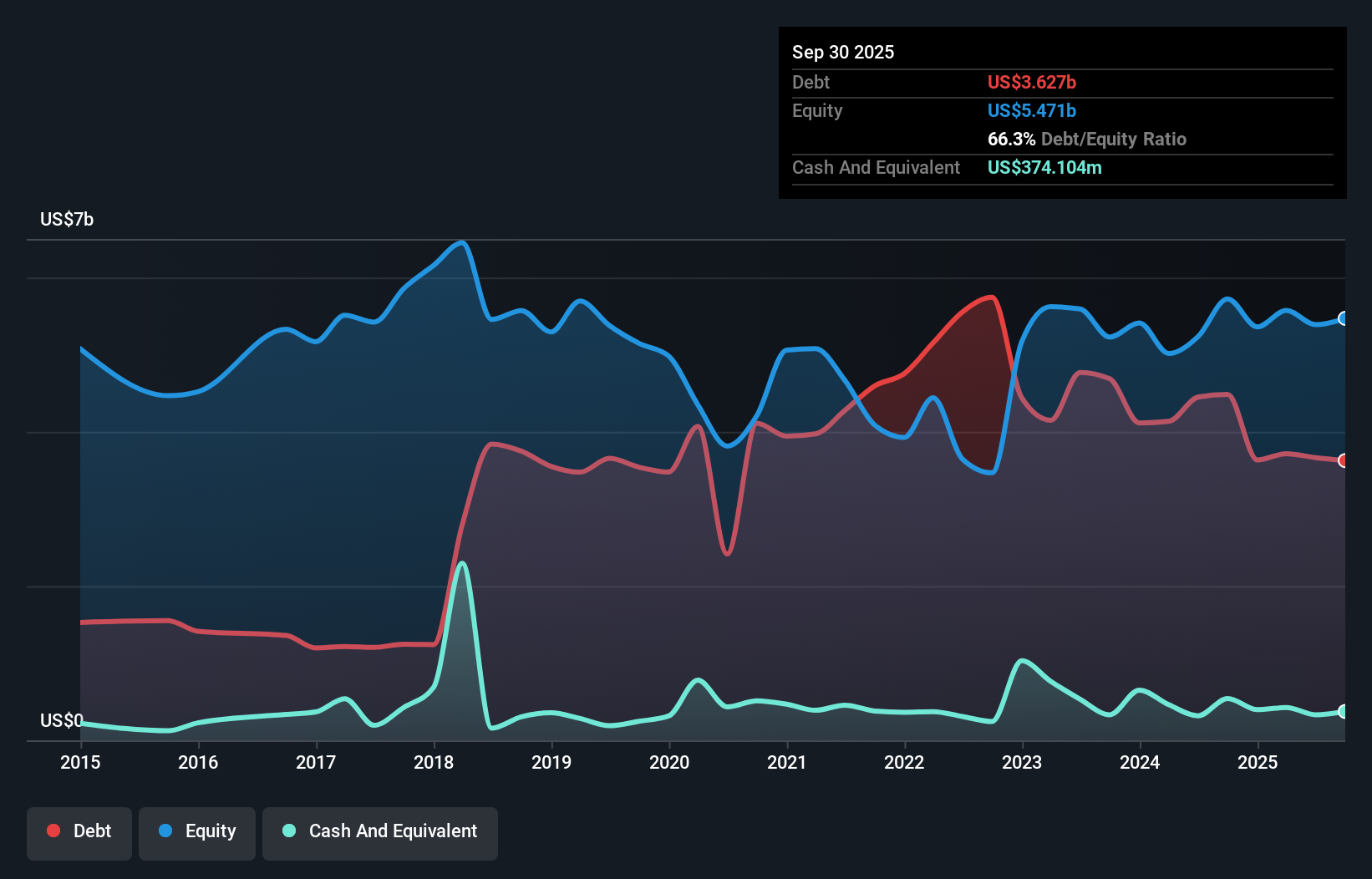

The image below, which you can click on for greater detail, shows that Enel Chile had debt of US$3.63b at the end of September 2025, a reduction from US$4.49b over a year. However, it does have US$374.1m in cash offsetting this, leading to net debt of about US$3.25b.

How Healthy Is Enel Chile's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Enel Chile had liabilities of US$1.93b due within 12 months and liabilities of US$5.17b due beyond that. Offsetting this, it had US$374.1m in cash and US$1.53b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$5.19b.

This is a mountain of leverage relative to its market capitalization of US$5.52b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

View our latest analysis for Enel Chile

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Weak interest cover of 2.4 times and a disturbingly high net debt to EBITDA ratio of 5.7 hit our confidence in Enel Chile like a one-two punch to the gut. The debt burden here is substantial. Even worse, Enel Chile saw its EBIT tank 71% over the last 12 months. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Enel Chile can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Enel Chile produced sturdy free cash flow equating to 77% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

On the face of it, Enel Chile's net debt to EBITDA left us tentative about the stock, and its EBIT growth rate was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. We should also note that Electric Utilities industry companies like Enel Chile commonly do use debt without problems. Overall, we think it's fair to say that Enel Chile has enough debt that there are some real risks around the balance sheet. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 2 warning signs we've spotted with Enel Chile (including 1 which is potentially serious) .

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.