Nasdaq

Nasdaq 華爾街日報

華爾街日報Newborn Town (SEHK:9911): Valuation Check After Insider RSU Purchase Signals Growing Confidence

The latest move by Newborn Town (SEHK:9911), where Three D Partners Limited bought 2,724,000 shares under its RSU Award Scheme, points to insider confidence that can reshape how investors view recent price action.

See our latest analysis for Newborn Town.

That insider-backed RSU purchase lands on top of a strong backdrop, with the share price up 10.76 percent over one day and 200.86 percent year to date on a share price return basis. The 1 year total shareholder return of 176.32 percent signals powerful, though recently more volatile, momentum.

If Newborn Town’s surge has you thinking about what else could be gaining traction, this is a good moment to explore fast growing stocks with high insider ownership.

Yet even with triple digit gains and a sizeable discount to analyst targets, investors still face a key question: is Newborn Town trading below its intrinsic value, or are markets already pricing in its next wave of growth?

Price-to-Earnings of 17.2x: Is it justified?

Newborn Town trades on a 17.2x price-to-earnings multiple, which looks undemanding versus peers and industry given its HK$10.5 last close.

The price-to-earnings ratio links what investors pay per share to the company’s current earnings power, a key lens for profitable interactive media platforms.

Here, the 17.2x multiple sits against high quality earnings, an outstanding 42.6 percent return on equity and significant profit growth historically. This suggests the market is not aggressively pricing those strengths. Relative valuation work implies a fair price-to-earnings ratio closer to 20x. This is a level the market could move towards if growth and profitability remain on track.

Compared with the Asian Interactive Media and Services industry average of 20.3x and a far higher 91.9x peer average, Newborn Town’s 17.2x stands out as materially lower. This reinforces the view that the shares are trading at what appears to be good value rather than speculative extremes.

Explore the SWS fair ratio for Newborn Town

Result: Price-to-Earnings of 17.2x (UNDERVALUED)

However, recent 90 day share price weakness, along with reliance on continued high-margin growth in a crowded social networking market, could quickly challenge the undervaluation thesis.

Find out about the key risks to this Newborn Town narrative.

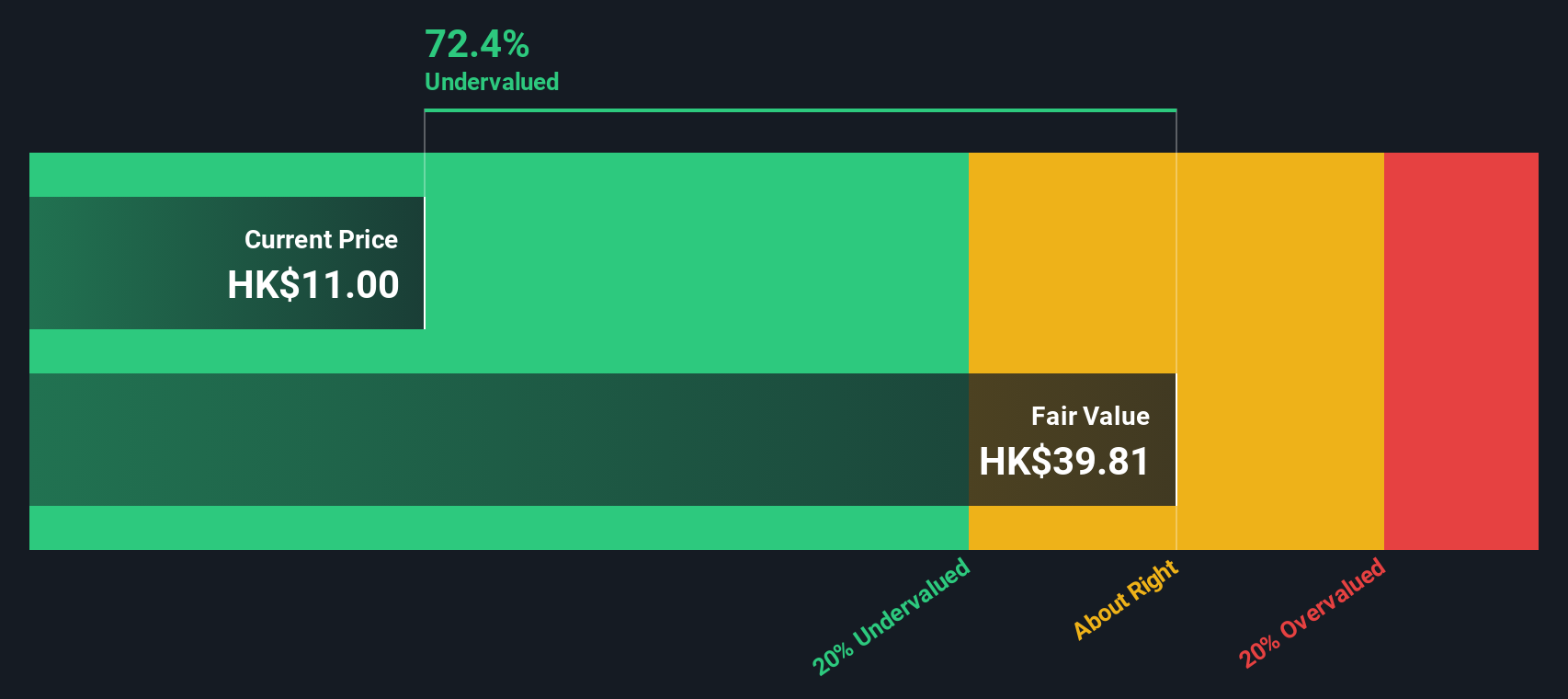

Another View via Our DCF Model

While the price to earnings ratio points to modest undervaluation, our DCF model paints a much stronger picture, suggesting Newborn Town is trading about 71 percent below an estimated fair value of roughly HK$36.2 per share. Is the market missing something, or is the model too optimistic?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Newborn Town for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 904 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Newborn Town Narrative

If you would rather examine the numbers yourself and question this view, you can build a detailed, personalized analysis in minutes: Do it your way.

A great starting point for your Newborn Town research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Do not stop with Newborn Town, use the Simply Wall St Screener to uncover fresh, data-backed opportunities that could upgrade your portfolio before others notice them.

- Capture the upside of fast-moving small caps by targeting these 3607 penny stocks with strong financials that combine growth potential with improving fundamentals.

- Position yourself at the forefront of automation by focusing on these 25 AI penny stocks shaping new profit pools in software, data, and intelligent infrastructure.

- Strengthen your income stream with these 12 dividend stocks with yields > 3% that aim to balance yield, payout sustainability, and long term stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com