Nasdaq

Nasdaq 華爾街日報

華爾街日報How Investors Are Reacting To Continental (XTRA:CON) Shifting French Retail To Franchising After Aumovio Spin-Off

- Earlier this month, Continental entered exclusive talks to sell its French ContiTrade retail operations, including more than 130 BestDrive outlets and two retreading facilities, to ASC Investment while keeping the network under a franchise model.

- This move advances Continental’s shift toward a fully franchised distribution structure in France, potentially lightening capital needs while preserving brand reach and service coverage.

- We’ll now examine how this portfolio reshaping, alongside Barclays’ downgraded stance after the Aumovio spin-off, feeds into Continental’s investment narrative.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

Continental Investment Narrative Recap

To own Continental, you need to believe the company can turn its technology and tire businesses into steady, cash generative franchises while working through restructuring and macro headwinds. The French ContiTrade sale talks fit this story by potentially trimming asset intensity, but they do not materially shift the near term focus on managing flat volumes and restructuring costs, which still look like the key catalyst and the biggest risk in the coming quarters.

The most relevant recent announcement here is Barclays’ downgrade to Equalweight after the Aumovio spin off and a strong share price run. That shift in analyst sentiment highlights how quickly expectations can get reset, even as the broker raised its price target and still sees appeal in Continental’s planned dividend policy, which remains an important part of the near term investment case.

Yet investors should also be aware of how large ongoing restructuring and spin off costs could still...

Read the full narrative on Continental (it's free!)

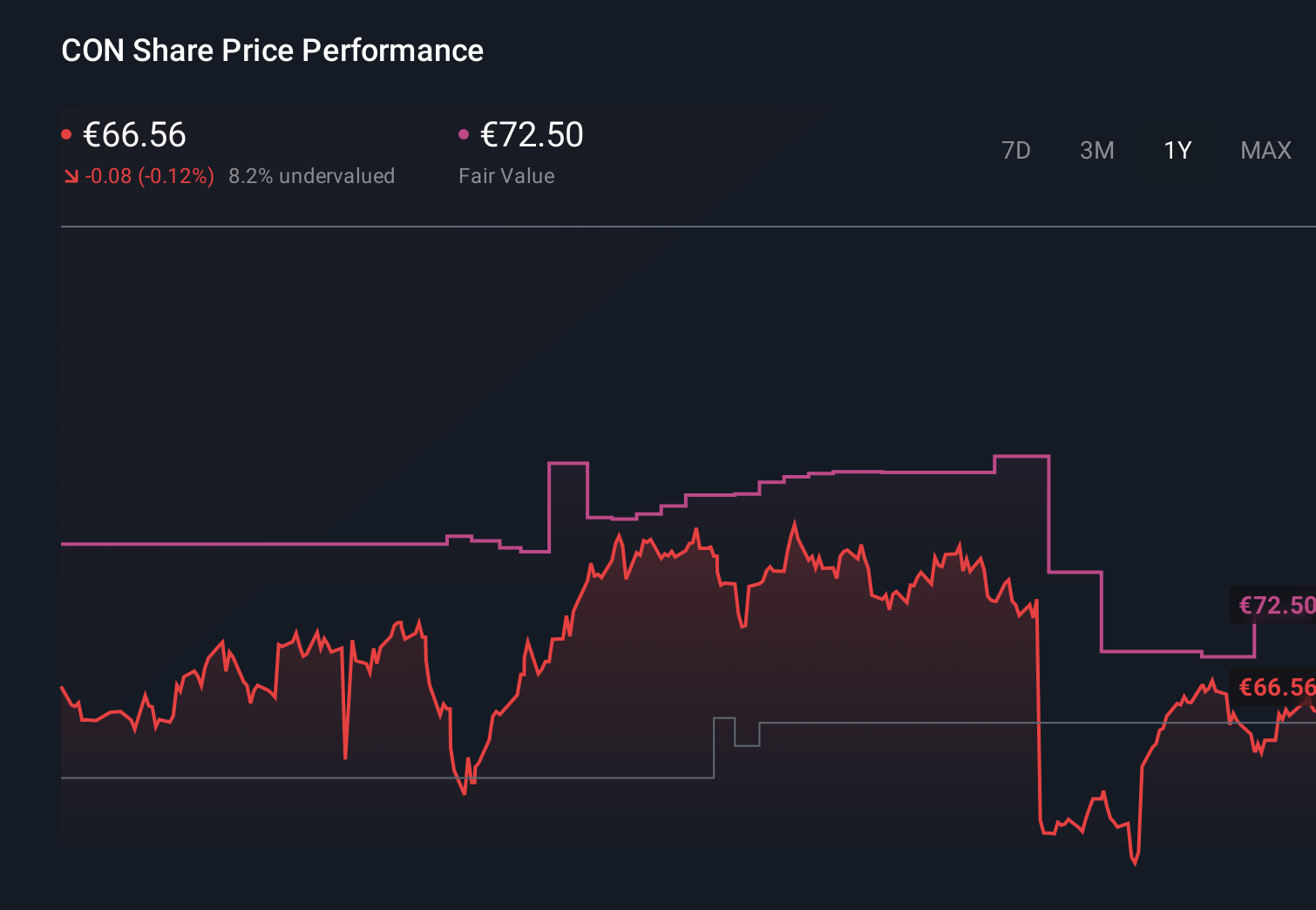

Continental’s narrative projects €41.4 billion revenue and €2.1 billion earnings by 2028.

Uncover how Continental's forecasts yield a €72.50 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community value Continental between €64.35 and €102.58, underscoring how far apart individual views can be. You might weigh those opinions against the risk that continued restructuring and separation costs keep weighing on free cash flow and near term earnings, with clear implications for how the business funds its transition and shareholder returns.

Explore 5 other fair value estimates on Continental - why the stock might be worth as much as 55% more than the current price!

Build Your Own Continental Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Continental research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Continental research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Continental's overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- We've found 12 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com