Nasdaq

Nasdaq 華爾街日報

華爾街日報Assessing American Express (AXP) Valuation After a Strong Year-to-Date Share Price Rally

American Express (AXP) keeps grinding higher, with the stock up roughly 3% over the past week and nearly 30% this year, as investors lean into its steady revenue and earnings growth.

See our latest analysis for American Express.

With the share price now at $384.89 and supported by an 18.31% 3 month share price return alongside a 29.55% 1 year total shareholder return, momentum appears intact rather than overextended.

If American Express has you rethinking what quality and growth look like in financials, it could be worth exploring fast growing stocks with high insider ownership as your next set of ideas.

Yet with the stock now trading above consensus analyst targets despite solid high single digit revenue and earnings growth, investors must ask: is American Express still undervalued, or has the market already priced in its future momentum?

Most Popular Narrative Narrative: 9.4% Overvalued

At $384.89, American Express sits above the most popular narrative's fair value estimate of $351.87. This frames the story as a rich but execution driven setup.

The company's ongoing focus on premium cardmembers and product refreshes, especially the upcoming U.S. Platinum Card relaunch, positions American Express to benefit from consumers' growing demand for personalized experiences and value added rewards, likely boosting net card fee growth and retention, which supports long term revenue and fee income expansion.

Want to see how steady double digit style growth, stable margins, and shrinking share count combine into that rich valuation story? The full narrative spells it out.

Result: Fair Value of $351.87 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that backdrop could shift if premium card competition intensifies or alternative payment platforms accelerate, which could pressure both customer growth and American Express's rich margins.

Find out about the key risks to this American Express narrative.

Another Lens on Valuation

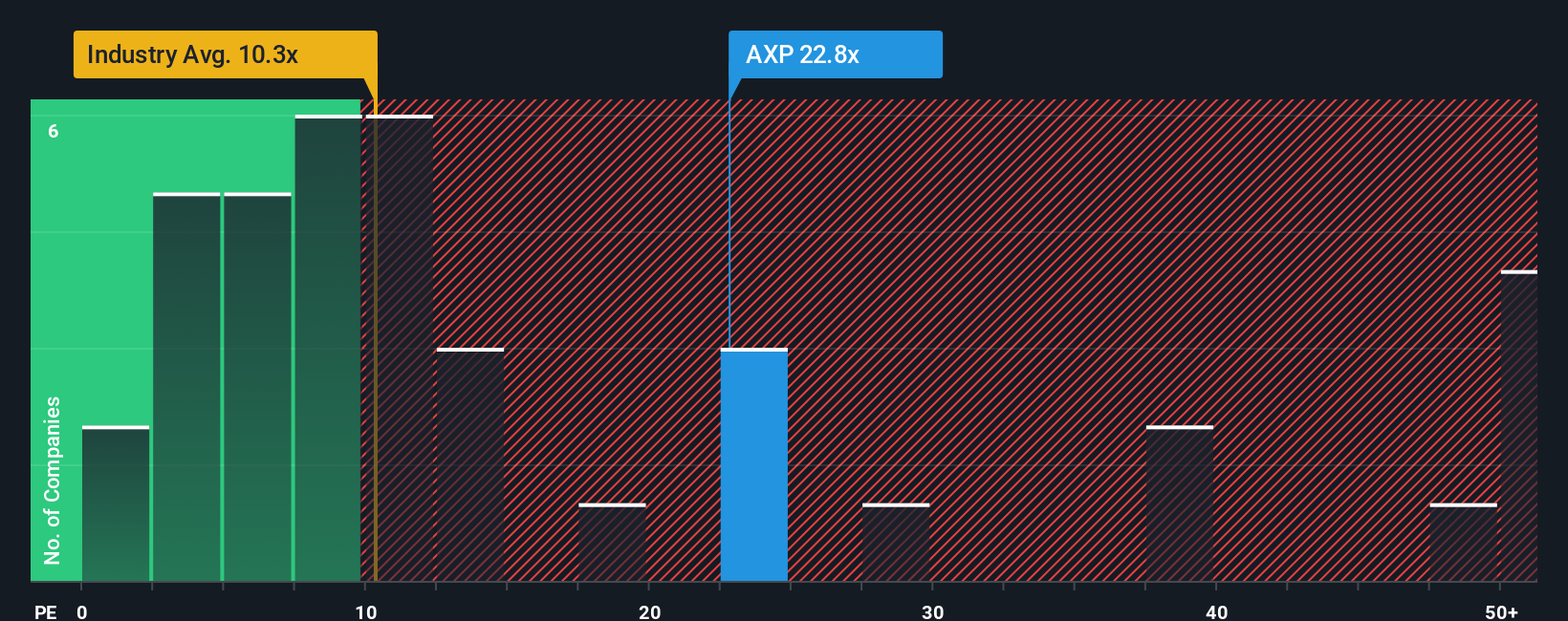

On earnings, American Express looks even richer. The current price implies a 25.5x price to earnings ratio, versus a fair ratio of 19.8x and just 9.2x across the US consumer finance industry. That premium may reflect quality, but it also raises downside risk if growth cools.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own American Express Narrative

If you see things differently or want to dive into the numbers yourself, you can build a personalized view of American Express in just a few minutes: Do it your way.

A great starting point for your American Express research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more investing angles?

Skip the guesswork and put your capital to work with focused idea lists from Simply Wall St’s screener, so you can systematically explore your next standout opportunity.

- Explore trends in artificial intelligence by targeting companies involved in rapid innovation with these 25 AI penny stocks.

- Seek income potential and resilience by focusing on businesses offering regular payouts through these 12 dividend stocks with yields > 3%.

- Investigate possible mispriced opportunities in the market by examining companies trading below their estimated intrinsic value using these 905 undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com