Nasdaq

Nasdaq 華爾街日報

華爾街日報How Eurofins’ Major Vietnam Lab Expansion Will Impact Eurofins Scientific (ENXTPA:ERF) Investors

- Eurofins Consumer Product Testing Vietnam has completed a major expansion, relocating to a purpose-built 7,000 sq. m laboratory in Ho Chi Minh City that offers more than two and a half times the floor space of its previous site.

- This enlarged facility underscores Eurofins’ commitment to supporting Vietnam’s growing role in global manufacturing supply chains, enhancing its ability to serve international brands, retailers, and manufacturers with broader testing capacity.

- Next, we’ll explore how this substantially larger Ho Chi Minh City lab could influence Eurofins’ investment narrative and long-term growth profile.

We've found 12 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

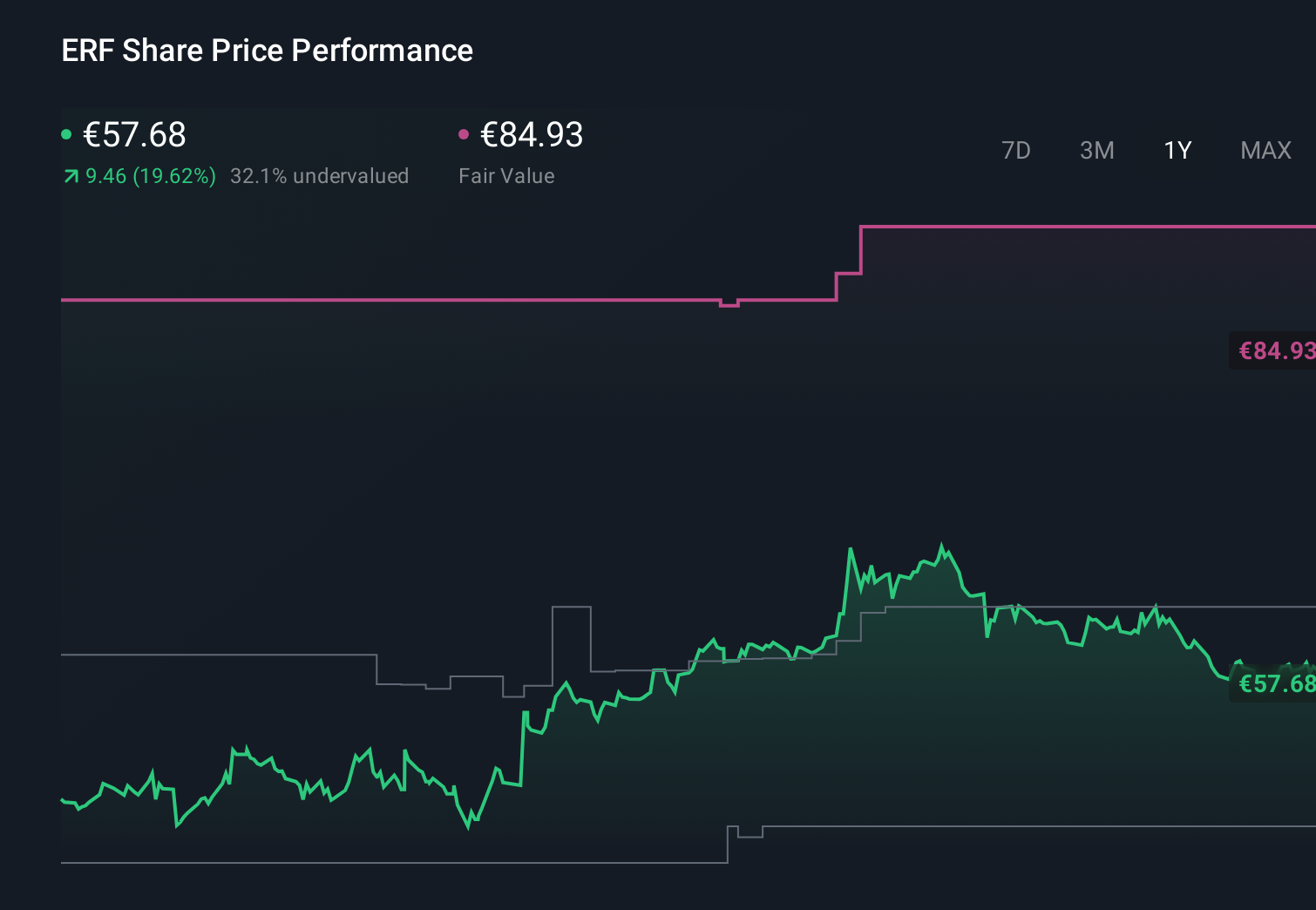

Eurofins Scientific Investment Narrative Recap

To own Eurofins, you need to believe that its global testing network can convert rising regulatory and outsourcing needs into steady, efficient growth, despite ongoing integration and capex demands. The Ho Chi Minh City expansion aligns with the hub and spoke strategy, but on its own it does not materially change the near term focus on improving margins and turning around underperforming assets like SYNLAB Spain, nor does it alter the key risk that heavy investment fails to translate into stronger cash generation.

The most relevant recent announcement is Eurofins’ ongoing share buyback activity, including 100,000 shares repurchased in early December 2025, which sits alongside capacity investments such as the enlarged Vietnam lab. While buybacks can support per share metrics, the more important catalyst remains whether Eurofins’ automation, digitalization and real estate program can lift profitability enough to offset integration challenges and justify both the capital intensity and these shareholder returns.

Yet beneath the promising growth story, investors still need to be aware of the risk that heavy capex and acquisitions could...

Read the full narrative on Eurofins Scientific (it's free!)

Eurofins Scientific’s narrative projects €8.8 billion revenue and €745.8 million earnings by 2028.

Uncover how Eurofins Scientific's forecasts yield a €63.93 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Six members of the Simply Wall St Community currently see Eurofins’ fair value between €46 and about €91, reflecting a wide spread of expectations. Against that, Eurofins’ large capex program and integration of weaker assets mean the payoff from its expanded lab network could be uneven, so it is worth weighing several different views on how efficiently the group can turn scale into sustainable earnings.

Explore 6 other fair value estimates on Eurofins Scientific - why the stock might be worth as much as 59% more than the current price!

Build Your Own Eurofins Scientific Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Eurofins Scientific research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Eurofins Scientific research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Eurofins Scientific's overall financial health at a glance.

Seeking Other Investments?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Rare earth metals are the new gold rush. Find out which 37 stocks are leading the charge.

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com