Nasdaq

Nasdaq 華爾街日報

華爾街日報Has the Market Already Priced In Walmart’s 25.8% 2025 Rally?

- If you are wondering whether Walmart is still good value after its huge run, or if you have already missed the boat, this breakdown will help you see what the market might be getting right or wrong about the stock.

- Walmart has climbed 25.8% year to date and 21.5% over the last year, with a strong 9.4% move in the past month even after a small 1.4% dip over the last week. This signals that sentiment has turned decisively more optimistic.

- Recent headlines have focused on Walmart doubling down on e-commerce, expanding its marketplace, and leaning further into grocery and value-driven essentials. These are all areas where it is steadily chipping away at competitors. At the same time, investors are watching how its investments in automation, supply chain technology, and membership programs can support profitable growth rather than just top line gains.

- Despite this strength, Walmart only scores 1/6 on our valuation checks, suggesting the stock screens as expensive on most traditional metrics. In the next sections we will unpack what the main valuation models say and then finish by looking at a more nuanced way to think about what Walmart might really be worth.

Walmart scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

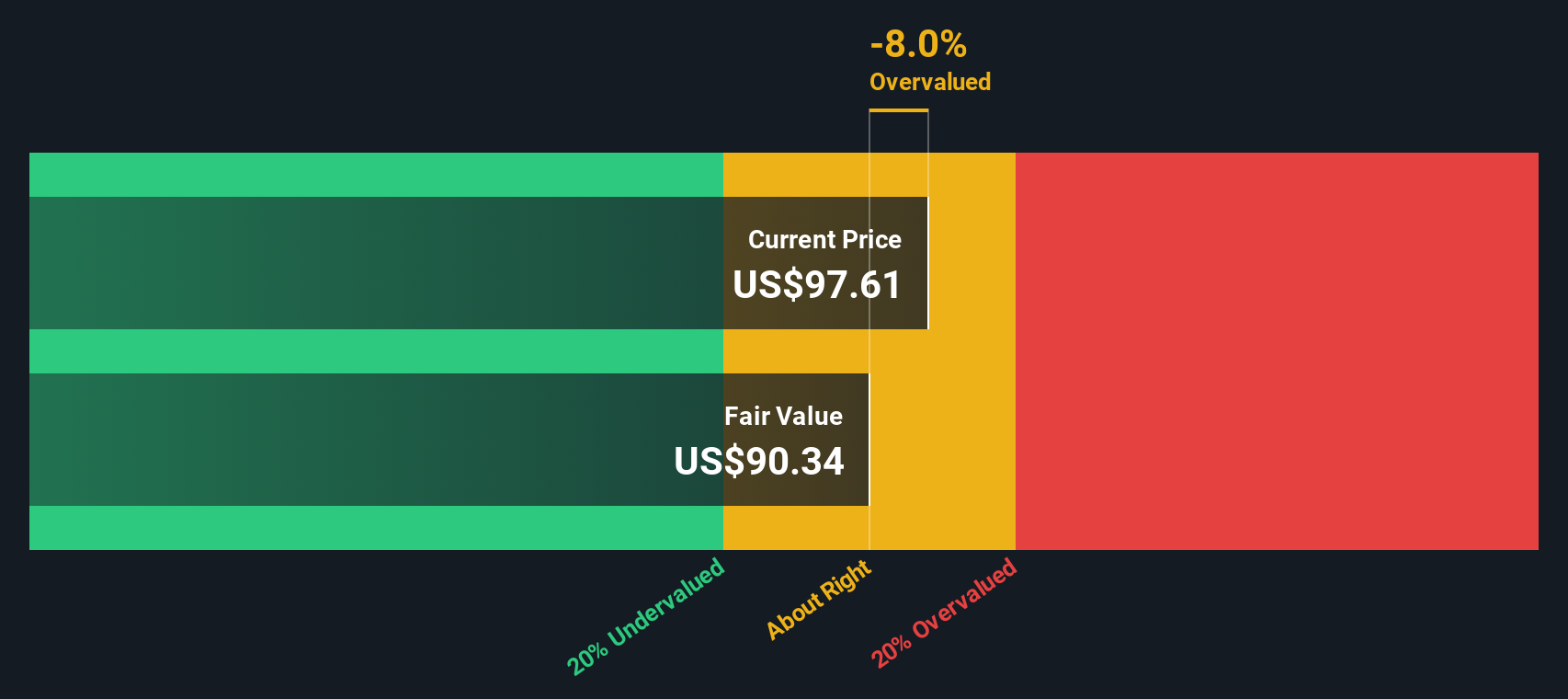

Approach 1: Walmart Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes Walmart's expected future cash flows and discounts them back to what they are worth in $ today, aiming to estimate an intrinsic value per share.

Walmart generated roughly $17.3 billion in free cash flow over the last twelve months, and analysts expect this to rise steadily as the business scales. By 2030, total free cash flow is projected to reach about $32.4 billion, with interim years stepping up from around $14.6 billion in 2026 as both analyst forecasts and extrapolated growth from Simply Wall St are layered in.

Adding up these projected cash flows and discounting them back results in an estimated intrinsic value of about $116.34 per share. Compared with the current market price, this implies the stock is only around 2.7% undervalued, effectively signaling that investors are already pricing in most of Walmart's future cash generation.

Result: ABOUT RIGHT

Walmart is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

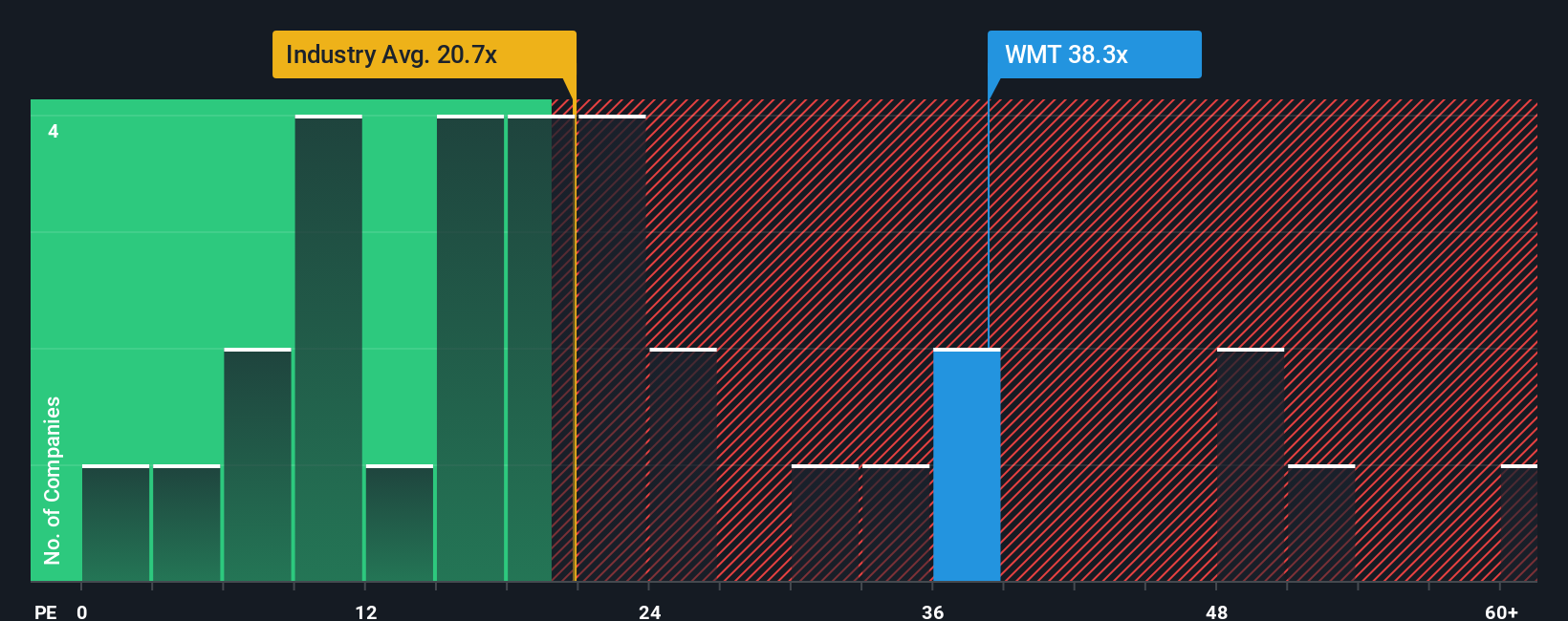

Approach 2: Walmart Price vs Earnings

For profitable and relatively mature businesses like Walmart, the Price to Earnings ratio is a useful yardstick because it links what investors pay directly to what the company earns per share today.

In general, faster growing and lower risk companies can justify a higher PE multiple, while slower growth or higher uncertainty should pull that multiple down toward or below the market and industry norms. Walmart currently trades on about 39.4x earnings, well above the Consumer Retailing industry average of roughly 21.7x and also ahead of its peer group average of about 25.8x. On those simple comparisons, the stock looks expensive.

Simply Wall St instead uses a proprietary Fair Ratio, which estimates what PE multiple Walmart should trade on given its earnings growth outlook, margins, scale, sector, and risk profile. For Walmart, that Fair Ratio is around 36.8x, lower than today’s 39.4x. Because this metric adjusts for company specific fundamentals rather than just comparing Walmart to a broad industry, it offers a more tailored view. On this basis, the shares appear modestly overvalued rather than outright stretched.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Walmart Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework that lets you attach a clear story to Walmart’s numbers by stating what you think its fair value is and how you expect its revenue, earnings, and margins to evolve over time.

A Narrative connects three pieces: the business story you believe in, the financial forecast that flows from that story, and the resulting fair value estimate that you can compare against today’s share price.

On Simply Wall St’s Community page, used by millions of investors, Narratives are an easy, guided tool that helps you turn your view on Walmart into a structured forecast. You can then see whether your fair value suggests it is a buy, a hold, or a sell at the current market price.

Because Narratives are updated dynamically as fresh news, earnings reports, or guidance arrive, your Walmart view can adjust automatically. You can compare your Narrative with others in the community, for example where one investor’s more cautious assumptions lead to a much lower fair value for Walmart than another investor’s optimistic Narrative that incorporates expectations of faster growth and higher margins.

Do you think there's more to the story for Walmart? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com