Nasdaq

Nasdaq 華爾街日報

華爾街日報How Investors Are Reacting To Harley-Davidson (HOG) Consolidating Commercial Leadership Under Its CFO

- Harley-Davidson recently announced that Chief Digital and Operations Officer Jagdish Krishnan and Chief Commercial Officer Luke Mansfield will step down effective December 31, 2025, while Chief Financial Officer Jonathan Root will retain his finance role and assume the title of Chief Commercial Officer, maintaining oversight of global commercial operations.

- This consolidation of financial and commercial leadership under Jonathan Root signals a meaningful shift in how Harley-Davidson aligns its capital decisions with front-line sales and market execution.

- We’ll now examine how consolidating commercial leadership under the CFO reshapes Harley-Davidson’s existing investment narrative and risk-return profile.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Harley-Davidson Investment Narrative Recap

To own Harley-Davidson today, you need to believe the brand can stabilize core heavyweight bike demand while successfully expanding into more affordable segments and experiences, despite weak retail sales and macro headwinds. The consolidation of commercial leadership under CFO Jonathan Root looks more like an internal realignment than a change to the near term catalyst around capital deployment or the key risk of ongoing demand softness, so its impact on the immediate investment case appears limited for now.

Against this backdrop, the recent decision to maintain the quarterly cash dividend at US$0.18 per share is worth watching, as it sits alongside sizeable share buybacks as a core part of Harley-Davidson’s capital return story. While dividend continuity can appeal to income focused holders, it also has to be weighed against pressures on earnings and cash flows if motorcycle demand and margins come under more strain than expected.

But while management is tightening capital and commercial control, investors should still be aware of how prolonged weakness in global retail motorcycle sales could...

Read the full narrative on Harley-Davidson (it's free!)

Harley-Davidson's narrative projects $3.9 billion revenue and $390.5 million earnings by 2028. This requires a 4.4% yearly revenue decline and about a $147.7 million earnings increase from $242.8 million today.

Uncover how Harley-Davidson's forecasts yield a $27.60 fair value, a 18% upside to its current price.

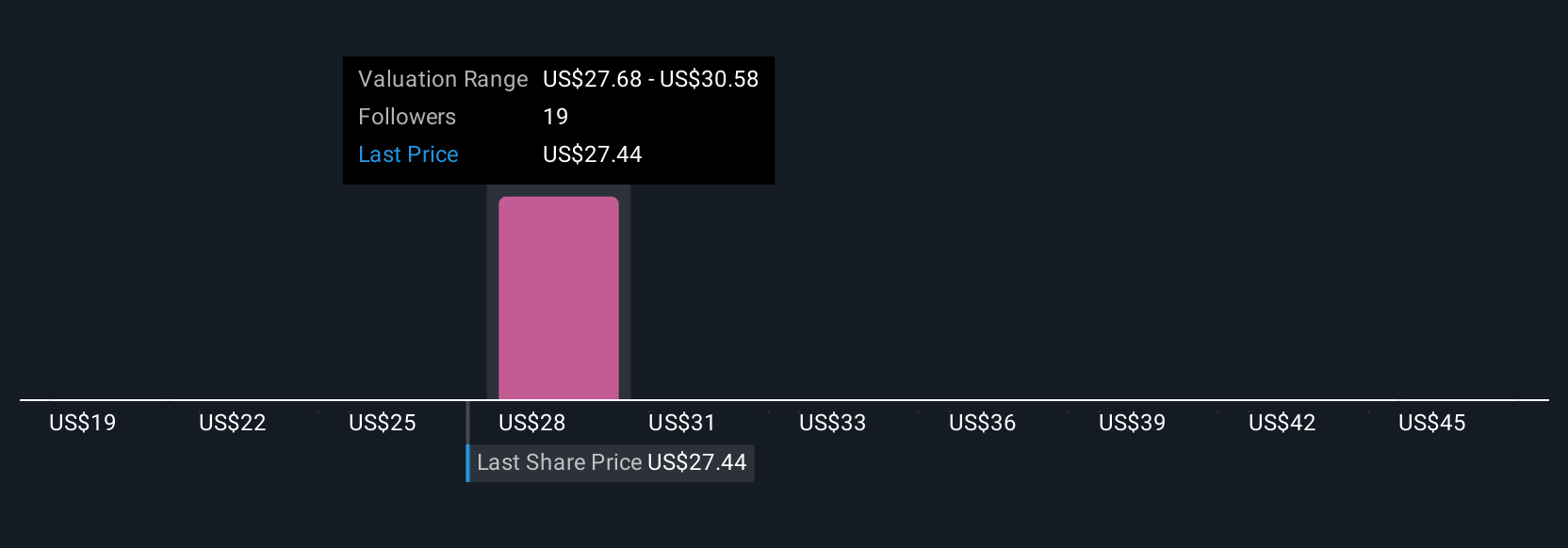

Exploring Other Perspectives

Five members of the Simply Wall St Community currently see Harley-Davidson’s fair value anywhere between US$19.00 and about US$47.94, reflecting a very broad range of expectations. Against that backdrop, the risk of persistently weak global motorcycle demand and tightening discretionary spending takes on added importance, since it could be a key factor in whether the business can support the earnings power implied by the higher end of those views.

Explore 5 other fair value estimates on Harley-Davidson - why the stock might be worth 19% less than the current price!

Build Your Own Harley-Davidson Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Harley-Davidson research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Harley-Davidson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Harley-Davidson's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com