Nasdaq

Nasdaq 華爾街日報

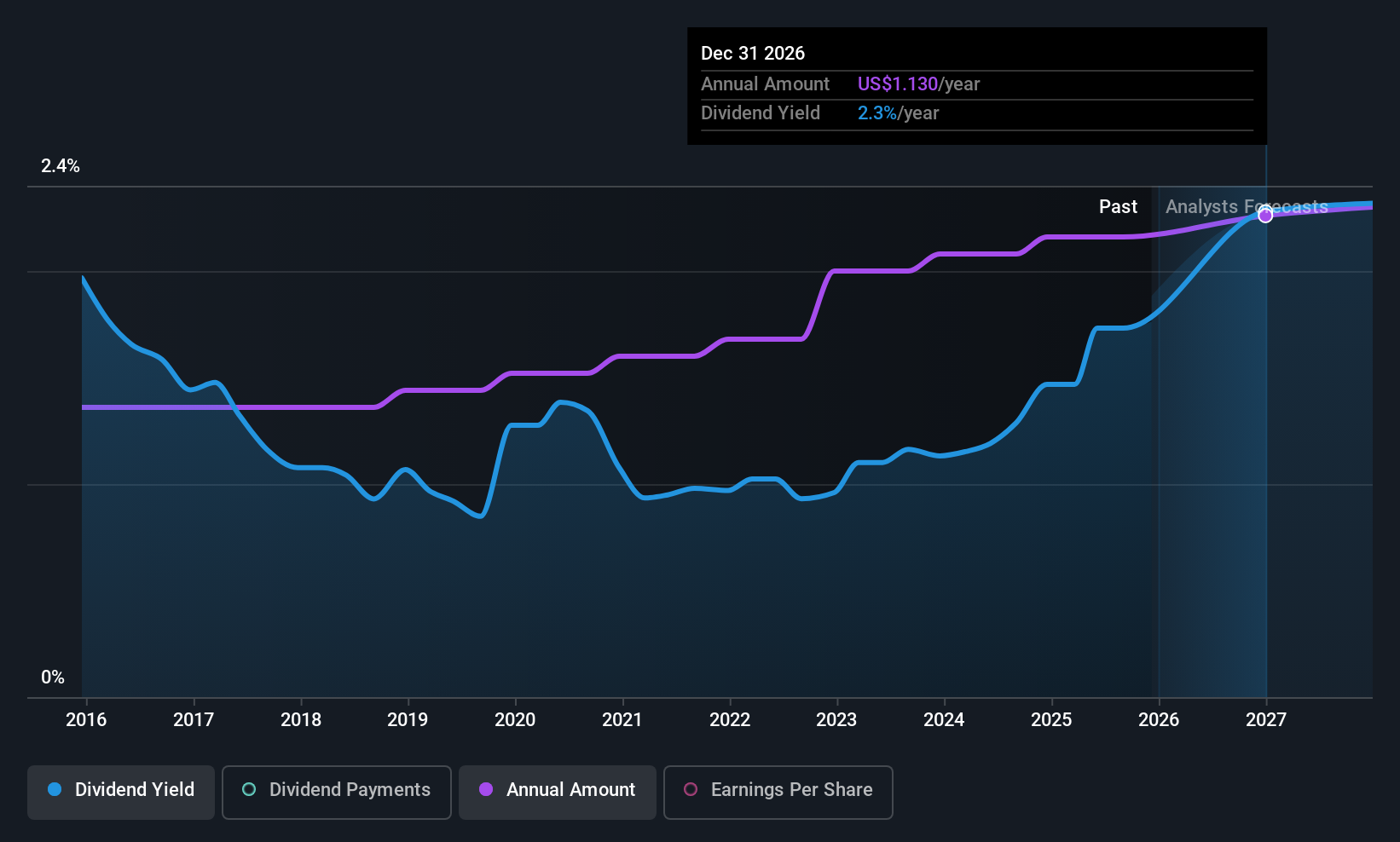

華爾街日報Albany International's (NYSE:AIN) Upcoming Dividend Will Be Larger Than Last Year's

Albany International Corp.'s (NYSE:AIN) dividend will be increasing from last year's payment of the same period to $0.28 on 8th of January. This takes the dividend yield to 2.3%, which shareholders will be pleased with.

Albany International's Long-term Dividend Outlook appears Promising

If the payments aren't sustainable, a high yield for a few years won't matter that much. Even though Albany International isn't generating a profit, it is generating healthy free cash flows that easily cover the dividend. In general, cash flows are more important than the more traditional measures of profit so we feel pretty comfortable with the dividend at this level.

Analysts expect a massive rise in earnings per share in the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 6.8%, so there isn't too much pressure on the dividend.

See our latest analysis for Albany International

Albany International Has A Solid Track Record

The company has an extended history of paying stable dividends. Since 2015, the annual payment back then was $0.64, compared to the most recent full-year payment of $1.12. This implies that the company grew its distributions at a yearly rate of about 5.8% over that duration. Dividends have grown at a reasonable rate over this period, and without any major cuts in the payment over time, we think this is an attractive combination as it provides a nice boost to shareholder returns.

Dividend Growth Potential Is Shaky

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. Unfortunately things aren't as good as they seem. Albany International's earnings per share has shrunk at 13% a year over the past five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future. On the bright side, earnings are predicted to gain some ground over the next year, but until this turns into a pattern we wouldn't be feeling too comfortable.

In Summary

Overall, we always like to see the dividend being raised, but we don't think Albany International will make a great income stock. The company is generating plenty of cash, but we still think the dividend is a bit high for comfort. Overall, we don't think this company has the makings of a good income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For instance, we've picked out 2 warning signs for Albany International that investors should take into consideration. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.