Nasdaq

Nasdaq 華爾街日報

華爾街日報What Quest Diagnostics (DGX)'s Octave MS Collaboration Means For Shareholders

- On 1 December 2025, Octave Bioscience announced a collaboration with Quest Diagnostics to offer its Multiple Sclerosis Disease Activity (MSDA) blood test through Quest’s roughly 7,000 U.S. specimen-collection sites, with Quest also gaining first rights to support future Octave tests for multiple sclerosis and Parkinson’s disease.

- This agreement deepens Quest’s presence in neurology testing by pairing its national collection network with a clinically validated, multi-biomarker tool that can inform more data-driven treatment decisions for more than one million Americans living with multiple sclerosis.

- We’ll now examine how expanding access to Octave’s MSDA Test via Quest’s national network could influence Quest Diagnostics’ broader investment narrative.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Quest Diagnostics Investment Narrative Recap

To own Quest Diagnostics, you need to believe that broad-based demand for advanced testing, plus ongoing efficiency gains, can outweigh reimbursement and cost pressures. The Octave collaboration looks incrementally positive for Quest’s neurology portfolio, but does not materially change near term catalysts that still hinge on sustaining core volume growth and managing PAMA-related pricing risk.

Among recent announcements, Quest’s raised 2025 revenue guidance to US$10.96 billion to US$11.00 billion, alongside higher EPS guidance, is most relevant here, as it frames how new partnerships like Octave’s MSDA Test might support management’s emphasis on higher value, specialized testing as a contributor to longer term earnings power.

Yet while partnerships may support growth, investors should also be aware of mounting reimbursement pressure that could...

Read the full narrative on Quest Diagnostics (it's free!)

Quest Diagnostics’ narrative projects $11.9 billion revenue and $1.3 billion earnings by 2028. This requires 4.1% yearly revenue growth and about a $355 million earnings increase from $945.0 million today.

Uncover how Quest Diagnostics' forecasts yield a $197.31 fair value, a 8% upside to its current price.

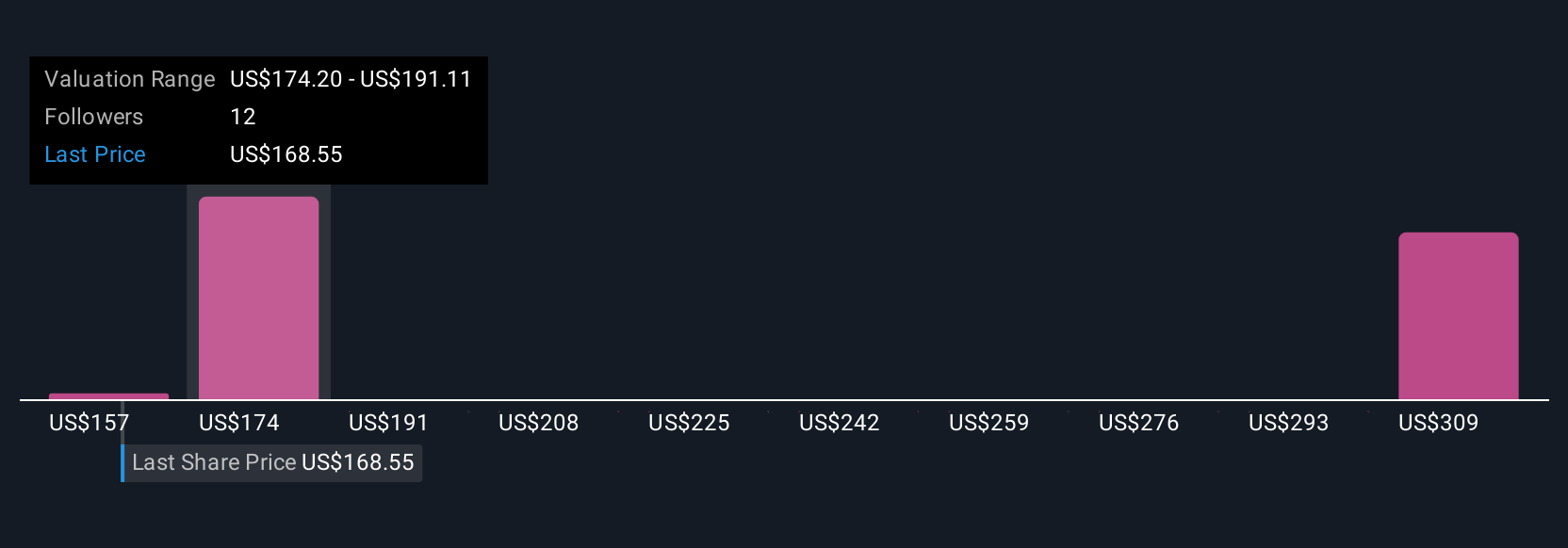

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates for Quest span roughly US$157 to US$225 per share, showing how widely individual views can differ. Against this, the risk of potential PAMA driven reimbursement cuts raises important questions about how Quest’s pricing and margins might evolve, which readers may want to examine through multiple lenses.

Explore 3 other fair value estimates on Quest Diagnostics - why the stock might be worth as much as 23% more than the current price!

Build Your Own Quest Diagnostics Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Quest Diagnostics research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Quest Diagnostics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Quest Diagnostics' overall financial health at a glance.

Curious About Other Options?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find companies with promising cash flow potential yet trading below their fair value.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com