Nasdaq

Nasdaq 華爾街日報

華爾街日報NIO (NIO) Is Down 8.4% After Strong November Multi-Brand Deliveries And Global Push - Has The Bull Case Changed?

- NIO Inc. recently reported that it delivered 36,275 vehicles in November 2025, a 76.3% year-over-year increase across its NIO, ONVO, and FIREFLY brands, bringing cumulative deliveries to 949,457 as of the end of that month.

- Alongside this delivery surge, NIO has been accelerating international expansion and infrastructure partnerships, while simultaneously contending with reduced Chinese EV subsidies and more cautious analyst commentary on future demand.

- We’ll now examine how November’s strong multi-brand delivery growth and ongoing international expansion may influence NIO’s broader investment narrative.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

NIO Investment Narrative Recap

To own NIO, I think you need to believe that its multi-brand strategy, battery swap ecosystem and international push can eventually turn rapid delivery growth into sustainable profits. November’s 76.3% year over year delivery rise supports that growth story, but softer Q4 guidance, reduced Chinese subsidies and ongoing net losses keep the key near term catalyst (a credible path to profitability) and the biggest risk (policy driven demand swings and margin pressure) very much in focus.

The most relevant update here is NIO’s Q4 2025 guidance for 120,000 to 125,000 deliveries and RMB 32,758 million to 34,039 million in revenue, which frames November’s strong numbers within a still cautious outlook. That guidance, coming alongside widening multi-brand deliveries and expanding infrastructure partnerships, helps investors weigh whether volume growth and NIO’s ecosystem are enough to offset subsidy cuts, intense competition and the company’s still sizeable net losses.

Yet behind the delivery headlines, investors should also be aware of how reduced subsidies could pressure ONVO volumes and margins over time...

Read the full narrative on NIO (it's free!)

NIO’s narrative projects CN¥148.4 billion in revenue and CN¥7.5 billion in earnings by 2028. This requires 28.8% yearly revenue growth and an earnings increase of about CN¥31.8 billion from CN¥-24.3 billion today.

Uncover how NIO's forecasts yield a $6.83 fair value, a 35% upside to its current price.

Exploring Other Perspectives

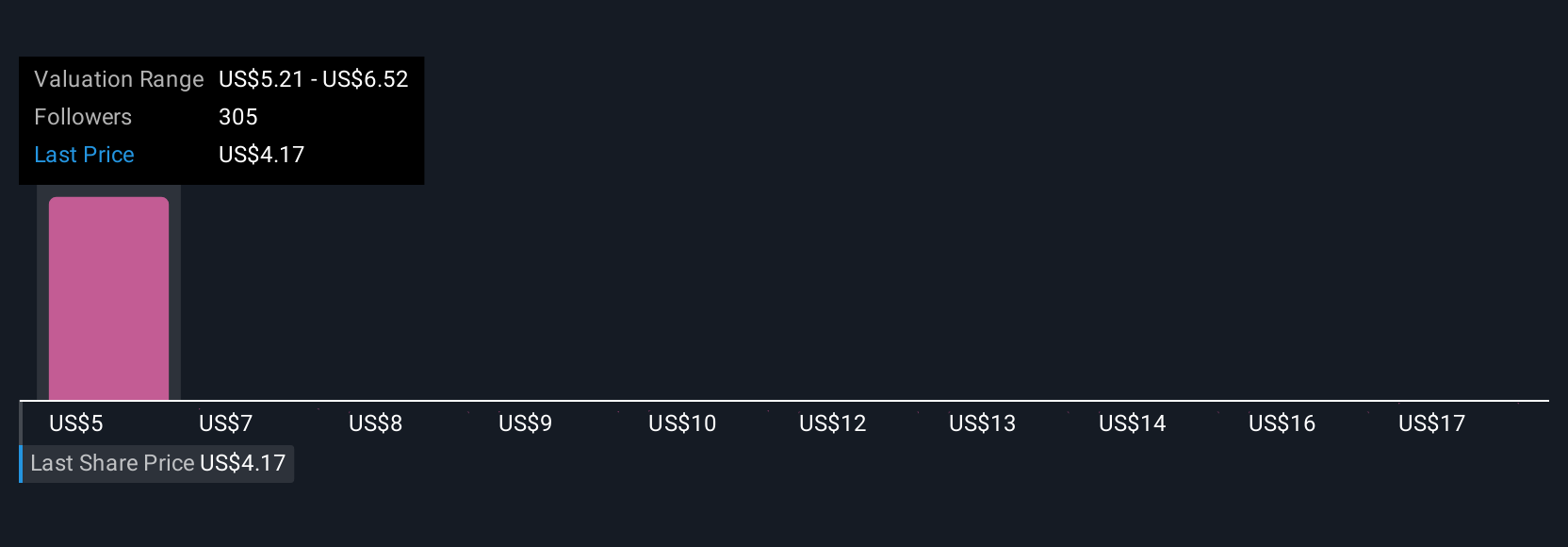

Twenty three members of the Simply Wall St Community currently see NIO’s fair value anywhere between US$4.15 and US$18.27, underscoring very different assumptions about its future. When you set those views against NIO’s continued net losses despite rising deliveries, it becomes clear why many investors are focusing closely on execution and profitability before forming a firm opinion on the stock.

Explore 23 other fair value estimates on NIO - why the stock might be worth 18% less than the current price!

Build Your Own NIO Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your NIO research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free NIO research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NIO's overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com