Is WTW’s KwantSure Partnership Quietly Rewiring Its Digital Risk Solutions Narrative (WTW)?

- On 15 July 2026, Willis Towers Watson US LLC, together with Kayna, announced a partnership with Kwant to launch KwantSure, embedding subcontractor insurance procurement directly into Kwant’s workforce and certificate-of-insurance platform used by general contractors across the United States.

- This move highlights Willis Towers Watson’s push deeper into digital, embedded insurance solutions that sit inside clients’ operational workflows, rather than traditional stand-alone broking channels.

- We’ll now explore how embedding tailored insurance within Kwant’s workforce platform could influence Willis Towers Watson’s investment narrative around digital risk solutions.

Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

Willis Towers Watson Investment Narrative Recap

To own Willis Towers Watson, you need to believe it can keep turning its advisory and broking franchise into scalable, tech-led risk solutions while managing high debt and strong competition. The KwantSure launch reinforces the digital and embedded insurance angle but does not materially change the near term picture, where the key catalyst remains execution on higher margin digital offerings, and a major risk is further fee pressure if technology and AI tools make core services easier for rivals to copy and undercut.

The Geospatial Mortality Model for the U.S. pension risk transfer market sits in the same digital risk toolkit as KwantSure, underlining how WTW is trying to embed data driven products deeper into client workflows. For investors watching catalysts, these kinds of tools can be helpful in assessing whether WTW is building enough differentiation versus Marsh McLennan and Aon to defend pricing and support steady revenue growth.

Yet, while these innovations are promising, investors should be aware that rising AI driven automation could still compress fees and margins if...

Read the full narrative on Willis Towers Watson (it's free!)

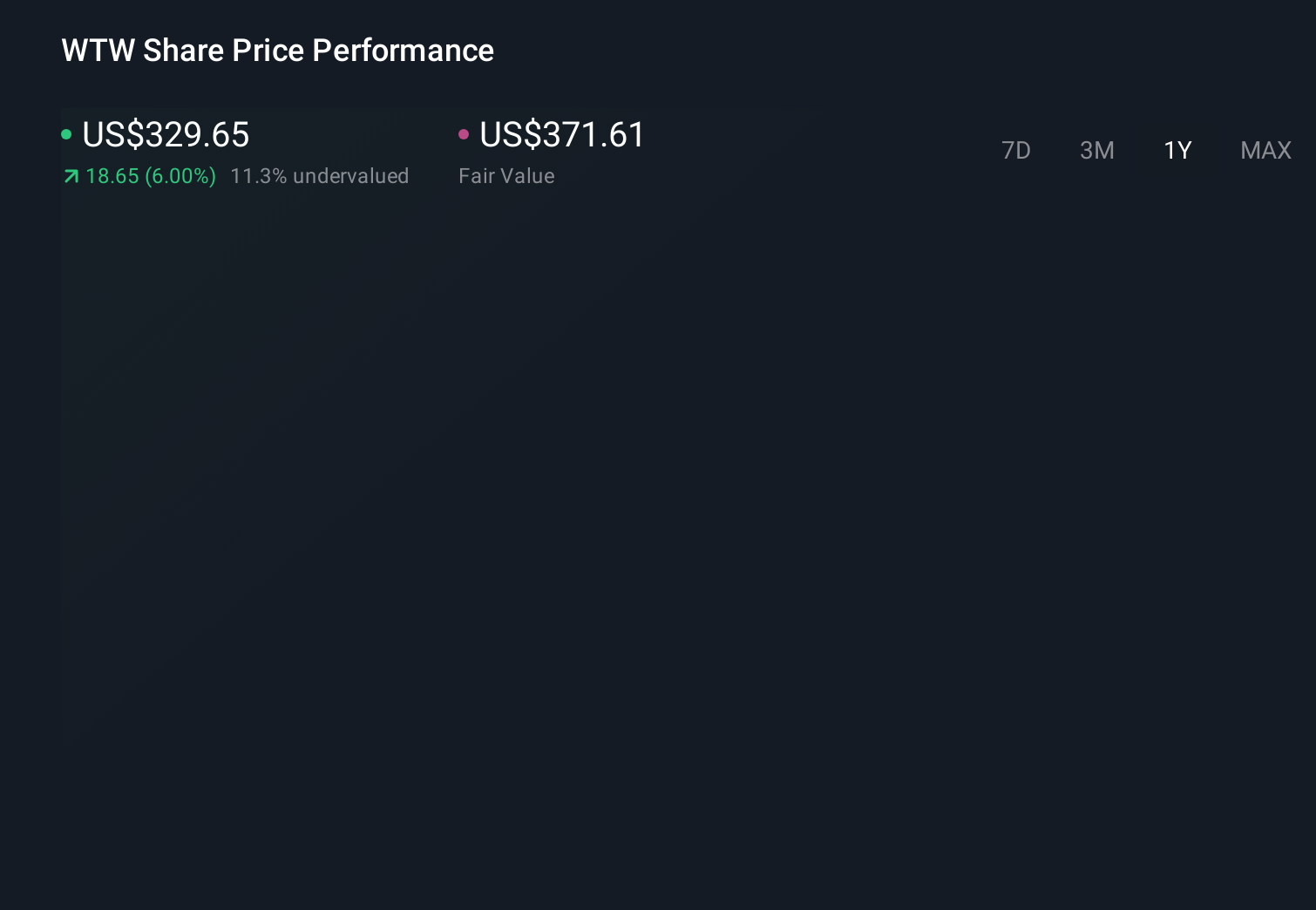

Willis Towers Watson's narrative projects $11.8 billion revenue and $1.9 billion earnings by 2029. This requires 6.1% yearly revenue growth and an earnings increase of about $0.2 billion from $1.7 billion today.

Uncover how Willis Towers Watson's forecasts yield a $334.32 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span about US$334 to US$446 per share, highlighting how far apart individual views can be. Against this spread, the central question is whether WTW’s push into embedded digital insurance like KwantSure can meaningfully offset the risk that AI driven automation turns core broking and consulting into a lower fee, more commoditized business, so it is worth considering several viewpoints before forming a view.

Explore 2 other fair value estimates on Willis Towers Watson - why the stock might be worth just $334.32!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Willis Towers Watson research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Willis Towers Watson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Willis Towers Watson's overall financial health at a glance.

Seeking Other Investments?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com