3 Energy Stocks With Direct Oil Price Exposure

Energy stocks are back in focus as geopolitical flare ups around the Strait of Hormuz collide with a world that now uses oil more efficiently and relies on deeper inventories and backup routes. That mix can dull some shocks but still leaves room for sharp surprises if supply is hit hard enough. For investors, the question is which large integrated oil and pipeline operators appear better positioned against that backdrop, and which might carry more risk. This article reviews three stocks from our Energy Sector Stocks screener that appear positively exposed to the current news flow.

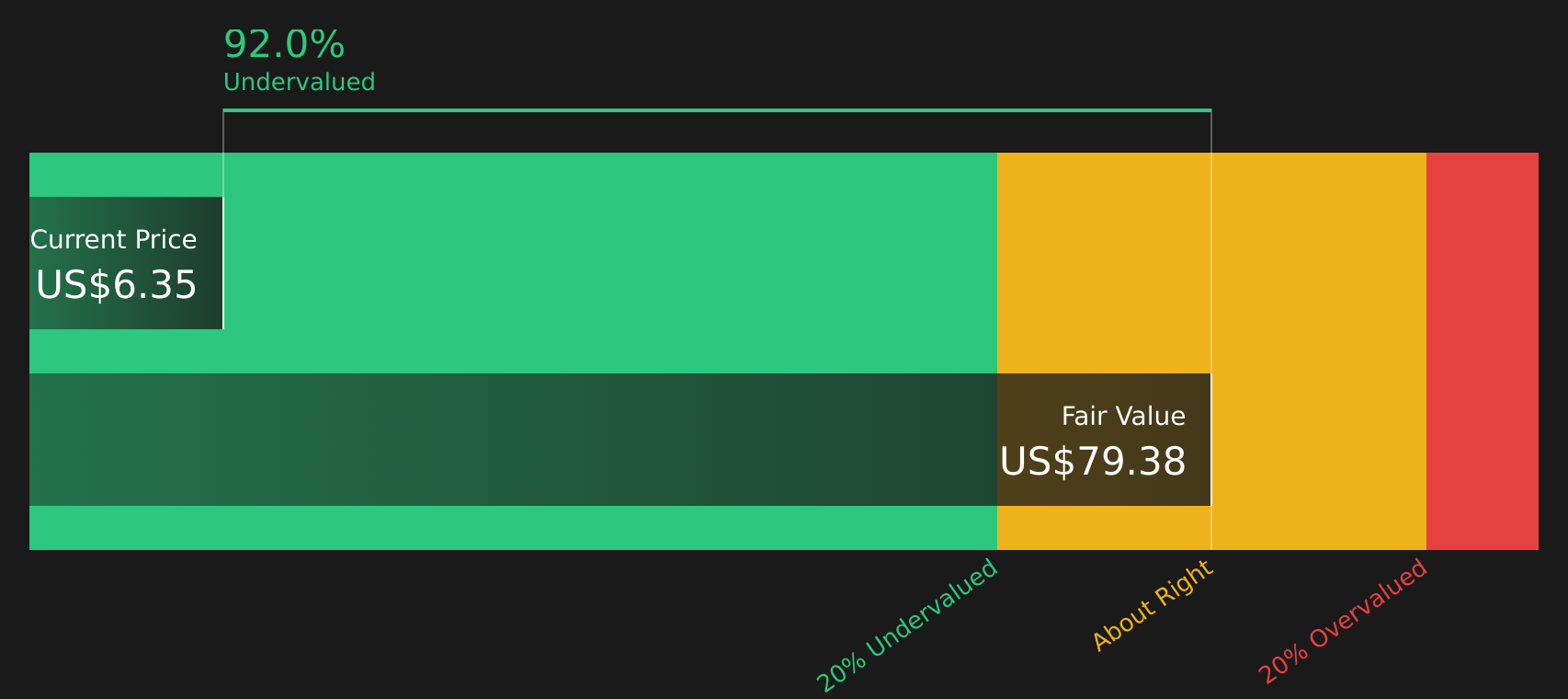

Valeura Energy (TSX:VLE)

Overview: Valeura Energy is an upstream oil and gas producer focused on exploring, developing, and operating oil fields in Thailand, with additional natural gas activities in Turkey, supplying crude and gas into international markets.

Operations: Valeura Energy generates essentially all of its US$542.2 million in revenue from oil and gas exploration and production, with Thailand contributing about US$558.5 million and small offsetting items in Turkey and corporate.

Market Cap: CA$1.2b

Investors looking at Valeura Energy are effectively getting direct exposure to oil prices at a time when Middle East supply risks are pushing key regional benchmarks like Dubai crude to large premiums over Brent. The company sells into those Asia linked markets. Valeura is growing production in Thailand, with recent Nong Yao drilling lifting volumes and supporting a sizeable 57.8 million barrels of oil equivalent reserve base, but profit margins have compressed and the current P/E is high, so execution on cost control and development timing matters. With analysts in broad agreement that earnings could rise from here and pointing to higher price targets, the difference between its growth plans and today’s compressed margins is what investors need to understand next.

Valeura Energy’s compressed margins, sizeable reserve base, and premium regional pricing raise a simple question for investors: what is the market missing about its next phase of earnings power and risks highlighted in the 3 key rewards and 1 important warning sign

Greenfire Resources (GFR)

Overview: Greenfire Resources is a Canadian oil sands producer that explores, develops, and operates bitumen assets at its Hangingstone Facilities in the Athabasca region near Fort McMurray, Alberta.

Operations: Greenfire Resources generates CA$550.6 million in revenue from its oil sands operations, all from Canada.

Market Cap: CA$785.2m

Greenfire Resources gives you pure play exposure to Canadian heavy oil at a time when geopolitical tensions around key shipping routes are keeping supply risks in focus, while efficiency gains are tempering demand growth. The company is working through production issues and facility downtime at its Expansion Asset and is ramping up output at the Demo Asset. This means execution on drilling, boiler repairs, and emissions compliance is critical. At the same time, the stock trades far below Simply Wall St’s estimated future cash flow value, so any progress toward consistent production and profitability could matter a lot for sentiment.

Greenfire Resources looks like a stalled heavy oil story trading well below Simply Wall St’s estimated future cash flow value, and the analysis report for Greenfire Resources could reveal the key production and balance sheet twist investors are missing.

Strathcona Resources (TSX:SCR)

Overview: Strathcona Resources is a Canadian oil and gas producer focused on heavy oil and thermal projects across the Cold Lake and Lloydminster regions, using steam assisted processes to extract bitumen and heavy crude. It pulls together multiple assets in Alberta and Saskatchewan into one large upstream producer centered on long life, oil weighted reserves.

Operations: Strathcona Resources generates CA$2.0b in revenue largely from its Cold Lake (CA$2,022m), Lloydminster Thermal (CA$963m), and Lloydminster Conventional (CA$618m) segments, with total revenue of CA$3.7b coming from Canada.

Market Cap: CA$8.4b

Strathcona Resources offers direct exposure to oil prices at a time when Strait of Hormuz tensions keep supply risks in the background, while global efficiency gains are limiting demand growth and helping restrain price spikes. The company is advancing heavy oil projects such as Meota Central and targeting higher production. At the same time, earnings have been under pressure, margins have slipped to 6.8%, and the dividend is not well covered by earnings or free cash flow. With analysts collectively projecting strong future earnings growth and viewing the stock as undervalued, investors are left to weigh its oil sands concentration, higher reliance on debt, and major shareholder selling against its project pipeline and long life Canadian reserves.

Strathcona Resources looks like an ambitious heavy oil consolidator where long life reserves, project ramp ups, and debt all intersect. Get the full story in the 3 key rewards and 3 important warning signs (1 is major!)

The three energy stocks in this article are only a starting point, and the full Energy Sector Stocks (Integrated Oil & Gas and Pipeline Operators) screener has highlighted 29 more large integrated oil and pipeline operators with equally compelling stories around asset quality, balance sheets, and exposure to sector trends. Use Simply Wall St to identify and analyze the specific catalysts, cash flow profiles, and risk reward narratives that matter most to you so you can focus on the highest conviction opportunities in this part of the market.

Take Control of Your Investment Journey

If Strathcona Resources or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh stock ideas can move from quiet to breakout fast, and by the time momentum is flying, the easy entry point is gone. Scan these under the radar lists and consider them before they become widely followed.

- Target potential income streams by reviewing the curated 6 dividend fortresses that aim to provide yields while prices are still under the radar.

- Spot potential breakout operators early by scanning the 10 resilient stocks with low risk scores before the crowd focuses on their steadier balance sheets and price momentum.

- Follow long term metal demand themes by checking the hand picked 8 top copper producer stocks while sentiment is still subdued and entry prices remain accessible.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com