British Steel Rescue Puts UK Industrial Stocks In Focus

The UK government’s decision to nationalise British Steel has thrown a spotlight on the country’s industrial and materials heavyweights, as investors weigh the trade off between political risk and potential support for domestic manufacturing. With China objecting to the move and warning of countermeasures, the stakes are not just about one steel producer, but about confidence in UK listed industrial stocks more broadly. This article looks at three large UK companies from our sector screener that appear closely exposed to this news, and explains how the same headlines could be a help or a hindrance for each stock.

Ashtead Technology Holdings (LSE:AT.)

Overview: Ashtead Technology Holdings provides specialist subsea equipment rental and related services that support offshore energy projects, from survey and robotics to inspection and asset integrity work, across renewables, oil and gas, decommissioning and infrastructure markets worldwide.

Operations: Ashtead Technology generates about £203.2 million in revenue primarily from oil well equipment and services, with around £135.9 million from Europe, £29.3 million from the Americas, £17.8 million from the Middle East and £20.2 million from Asia Pacific.

Market Cap: £342.1 million

Ashtead Technology sits at the heart of subsea infrastructure, which puts it squarely in focus as the UK talks more about industrial resilience and supply chains after the British Steel nationalisation. The company combines relatively strong profitability metrics, including a 20.5% Return on Equity and net margins around the mid teens, with analyst expectations for continued earnings and revenue growth. It trades on a P/E that is reported to be well below both peers and the wider European trade distributors group. However, the balance sheet carries meaningful debt, which raises the importance of consistent cash generation if conditions tighten. For investors weighing valuation against risk, the key question is whether this combination of offshore exposure and pricing leaves too much on the table.

Ashtead Technology’s mix of mid teens margins, a 20.5% Return on Equity and a P/E reportedly well below peers raises a clear question. See the 5 key rewards and 1 important warning sign that could explain whether the debt load is just background noise or a decisive plot twist.

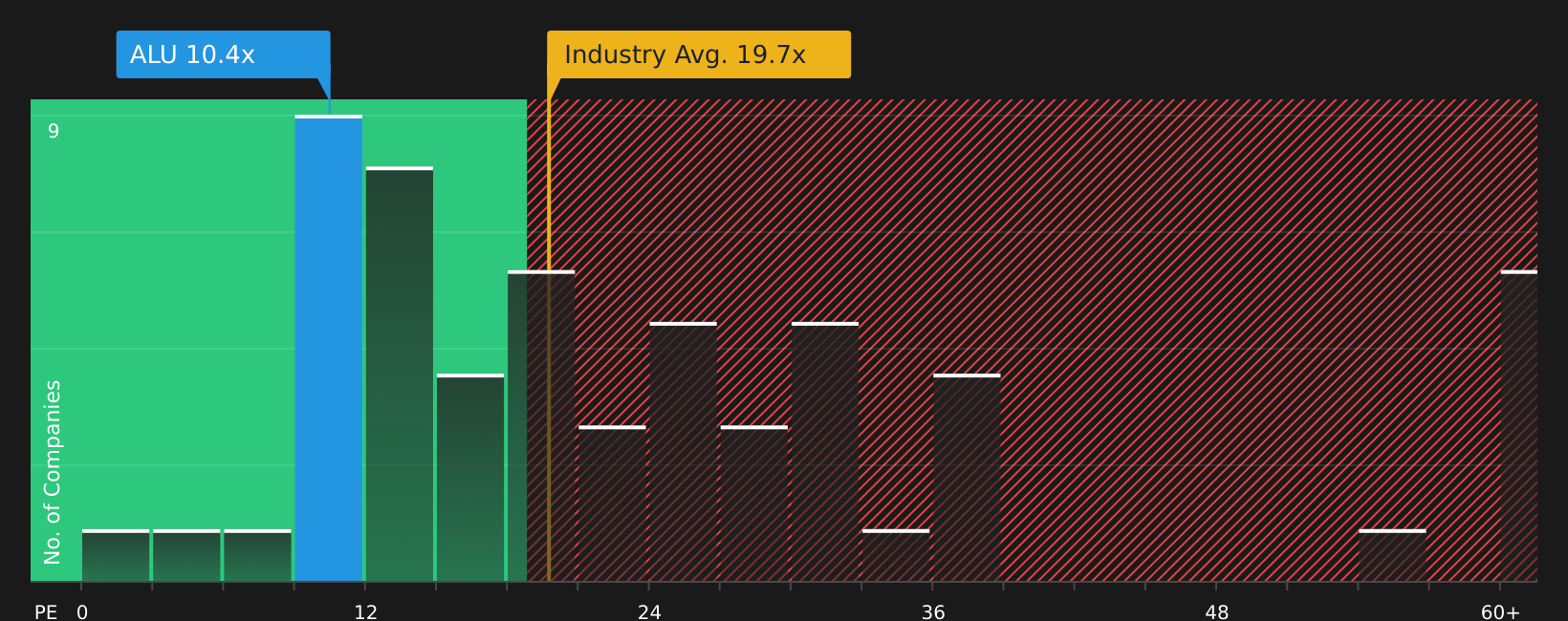

Alumasc Group (AIM:ALU)

Overview: Alumasc Group manufactures and sells building products and systems, supplying everything from aluminium and steel components to roofing membranes, insulation, drainage and housebuilding accessories for construction projects in the UK and overseas.

Operations: Alumasc Group generates around £48.6 million in revenue from Water Management products, £40.6 million from Building Envelope solutions and £17.2 million from Housebuilding Products.

Market Cap: £82.7 million

Alumasc Group may appeal to investors who believe UK reindustrialisation and domestic supply chains could gain importance after the British Steel nationalisation. The company is closely linked to UK construction and infrastructure, sells higher value roofing and water management systems, and is focusing on sustainability-oriented products. However, it also faces a soft UK construction market and execution risk as it pursues international growth. Forecast earnings growth above the wider UK market, combined with a P/E below sector peers and a price target comfortably above the current share price, may suggest to some investors that the stock is mispriced, although funding risk and a relatively new management team mean the investment case still involves significant uncertainty.

Alumasc Group’s mix of UK exposure, sustainability products and a P/E below sector peers suggests the market might be missing something in plain sight. For the fuller story, see the analysis report for Alumasc Group

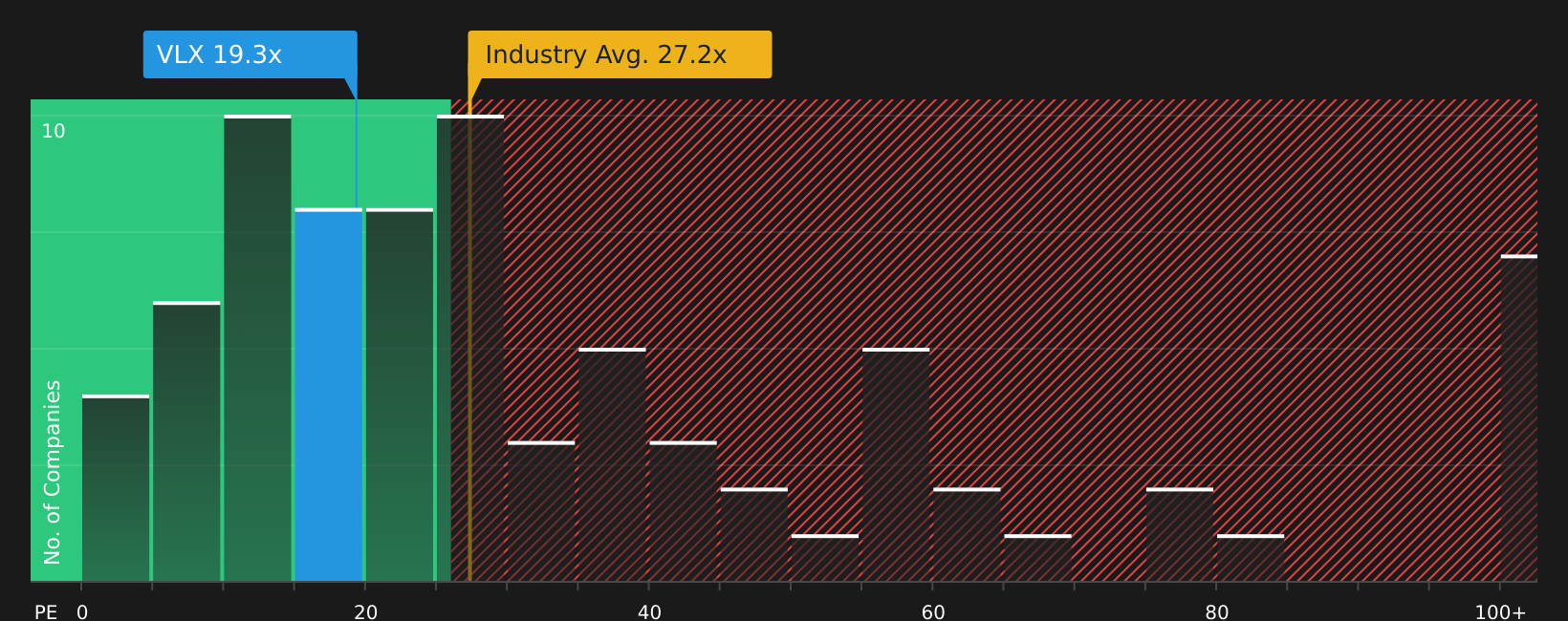

Volex (AIM:VLX)

Overview: Volex is a UK based manufacturer of power and data cables and broader connectivity solutions, supplying electric vehicle, medical, industrial and consumer equipment makers with everything from EV charging hardware to complex wiring assemblies across North America, Europe and Asia.

Operations: Volex generates its revenue across three major regions, with about $158 million from Asia, $439.1 million from Europe and $645.5 million from North America.

Market Cap: £963.7 million

For investors watching how the British Steel nationalisation might refocus attention on UK manufacturing resilience, Volex offers a different angle on critical industrial infrastructure. The company sits in the wiring and connectivity layer that keeps factories, data centres, EVs and medical devices running. Analysts report a P/E that is below some electrical peers, while also noting expectations for earnings and revenue. At the same time, heavy reliance on external borrowing and execution risk around acquisitions and integration mean the investment case is not straightforward. The key consideration for investors is whether the mix of sector exposure, margin profile and UK industrial positioning is enough to justify taking on those funding and integration risks.

Volex’s growth story in EVs, medical and industrial gear is easy to like, but the market may not be pricing the full picture. Before you decide, scan the analysis report for Volex.

If the industrial and materials stocks in this article caught your eye, they are only a small slice of the opportunity set, and the full UK Industrial and Materials Sector Stocks screener surfaces 21 more companies that appear to have equally compelling stories. Use Simply Wall St to identify, filter and analyze the specific catalysts and narratives that matter to you so you can focus on the highest conviction ideas in this corner of the market.

Take Control of Your Investment Journey

If Alumasc Group or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Curious About Alternative Stock Paths?

Fresh ideas do not stay under the radar for long. Some stocks are already building momentum while others are dropping off the radar. Check these screens before the crowd, act now.

- Spot resilient compounding potential by reviewing a curated 7 resilient stocks with low risk scores that may help you stay invested through rough patches without constantly watching every headline.

- Ride structural shifts in energy and infrastructure with a focused shortlist from the 90 nuclear energy infrastructure stocks while sentiment is still catching up to the story.

- Position ahead of the next hardware breakout using the hand picked 53 AI infrastructure stocks that highlights companies building the backbone for future computing demand.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com