Mastercard (MA) Stock Looks Fully Valued With Earnings Priced In

Mastercard stock sits at an interesting point, with a roughly 48.7% total return over the past five years and a recent share price of US$551.54, while the broader valuation checks still lean toward the shares being expensive rather than a clear bargain.

- Over five years, Mastercard has returned about 48.7%, which is a solid outcome but not one that automatically justifies paying any price for the stock.

- On the upside, ongoing growth in digital payments and partnerships across areas like cross border transactions and tokenised online checkout can support revenue expectations. At the same time, regulatory pressure on fees and rising competition from bank owned networks and alternative payment rails may cap how much investors are willing to pay for that growth.

- With a low value score of 2 out of 6, Mastercard currently screens as leaning expensive on the broader set of valuation checks rather than standing out as underpriced.

The issue now is whether Mastercard's current premium is still reasonable given the trade off between its long term return record and the growing set of risks around fees, competition, and regulation.

Has Mastercard Run Too Far on Earnings?

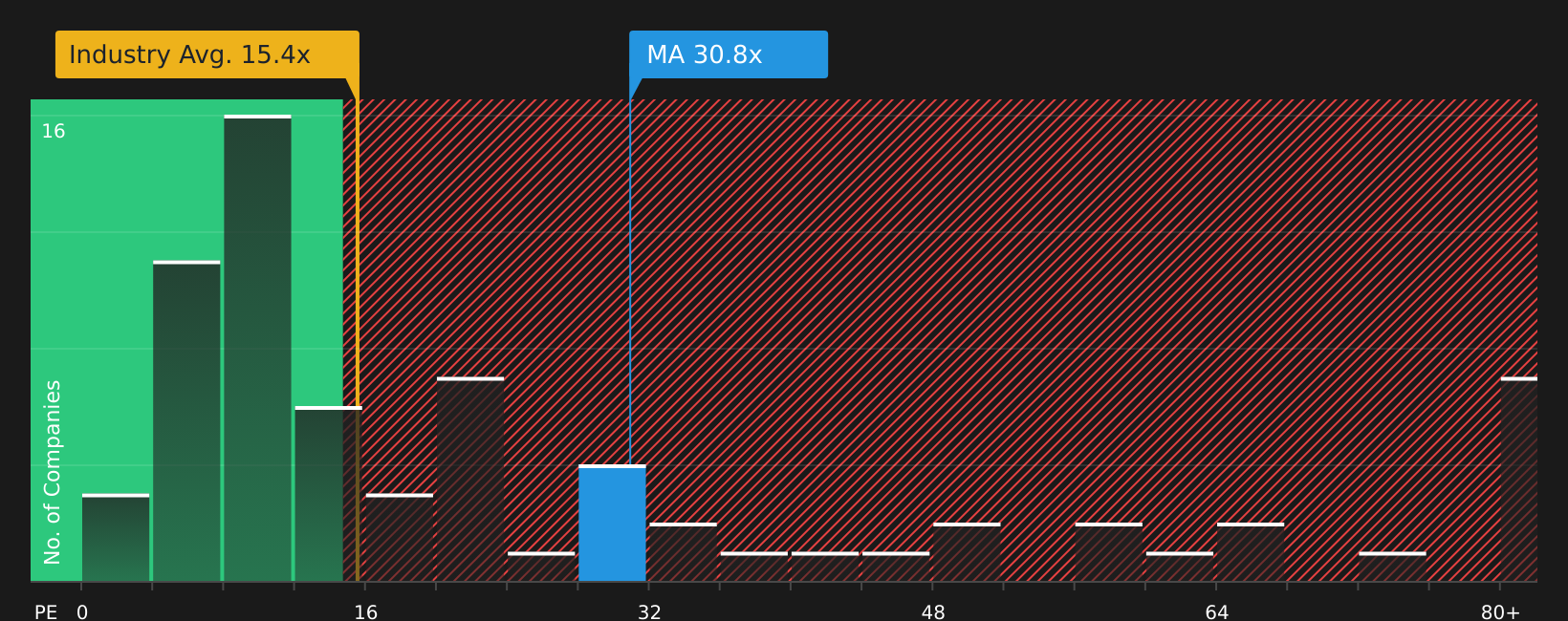

The P/E ratio is a useful yardstick for Mastercard because earnings remain a core way investors frame what they are willing to pay for a mature, profitable payments network. Mastercard currently trades on a P/E of about 31.3x, which sits above both the Diversified Financial industry average of roughly 15.6x and the peer group average near 27.6x.

The stock also screens above a modelled fair P/E of 21.0x. This reflects what investors might typically pay given Mastercard's size, margins, sector and risk profile. That gap suggests the market is assigning a clear premium to the Mastercard story, even as recent headlines highlight fee caps, bank owned network plans and alternative payment rails that could pressure economics over time.

On this P/E measure, Mastercard stock currently looks overvalued versus both tailored fair value estimates and broader industry benchmarks.

See what the numbers say about this price — find out in our valuation breakdown.

The Mastercard Narrative: What Would Justify Today's Price?

To make sense of why Mastercard's current P/E premium might still hold or could fade, Simply Wall St Narratives set out the specific paths the company could follow in terms of growth, margins and earnings, and what each path might imply for the stock's value relative to today's price. These are available on Mastercard's Community page. Each path ties its outcome to a clear view of where Mastercard's growth, profitability and risks go next, giving you something concrete to revisit as fresh data and news come through.

Community views on Mastercard are split, with some seeing a quality compounder on sale while others think the premium already builds in the good news.

Bull case: 26% undervalued

"Mastercard isn’t standing still while stablecoins reshape payments, it’s building settlement infrastructure and tools for "agentic commerce" around them instead of fighting the trend..."

Read the full Bull Case to see why Mastercard could be undervalued

Bear case: 6% overvalued

"Valuation premium: Mastercard trades around 30× forward earnings, above industry average (~22×), leaving little margin for error..."

Read the full Bear Case to see why Mastercard could be overvalued

Do you think there's more to the story for Mastercard? Head over to our Community to see what others are saying!

The Bottom Line

For Mastercard, the market multiple view points to an overvalued stock, with investors clearly paying up relative to peers and tailored benchmarks. That premium rests on the belief that Mastercard can keep converting its position in digital payments into resilient earnings despite regulatory and competitive pressure. With broader valuation checks also screening weak, the key question is whether that optimism on future growth and profitability is still justified, or whether the current P/E leaves too little room for any disappointment on fees, new payment rails, or how quickly the industry changes from here.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com