Capcom Stock Joins Two Japan Growth Names Backed By Heavy Insider Ownership

With inflation readings, interest rate moves and trade tensions pulling markets in different directions, many investors are looking for companies where management has real skin in the game and where external expectations remain optimistic. That is exactly what the Fast Growing Stocks With High Insider Ownership screener focuses on. It highlights businesses where insiders are heavily invested alongside you and analyst outlooks are broadly constructive. This combination can help you focus on growth opportunities that are supported both inside and outside the company. In this article, you will see three stocks from the screener that stand out based on these criteria.

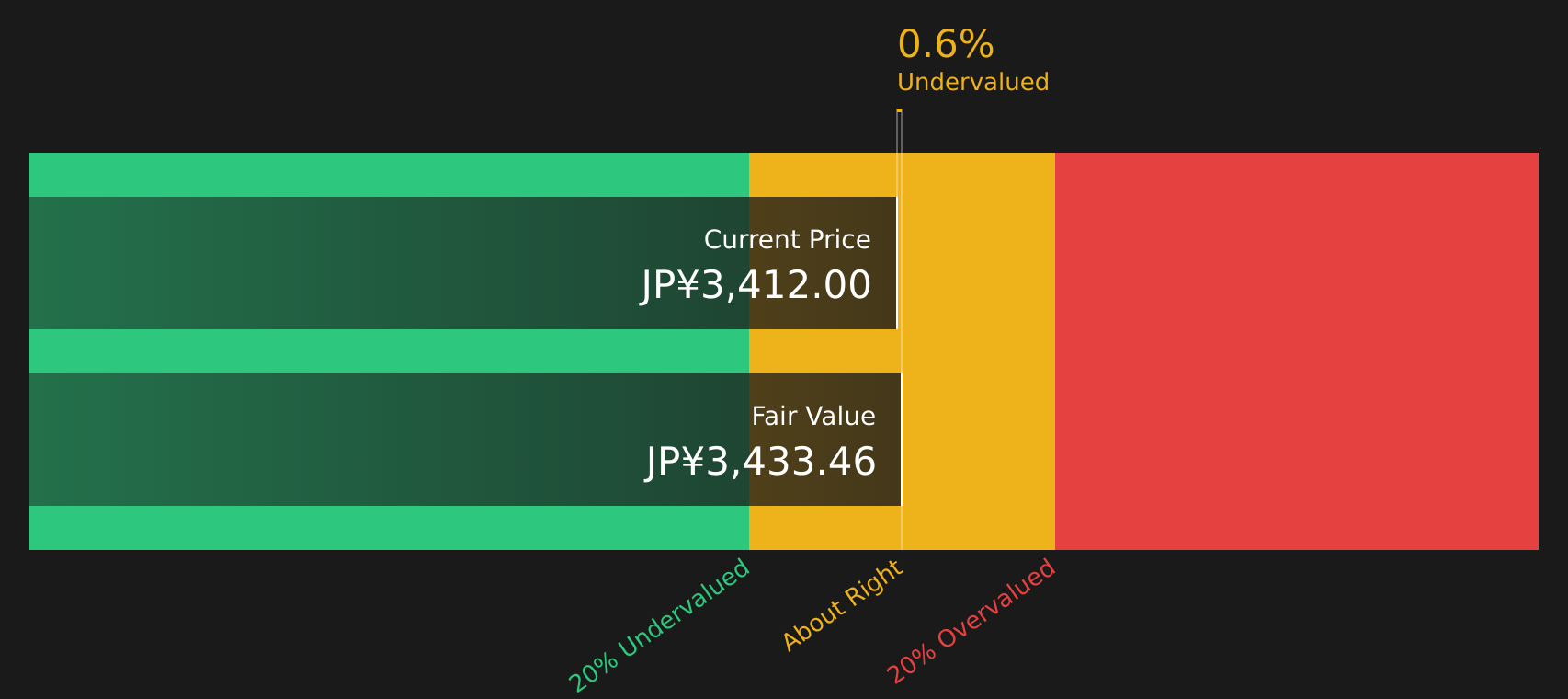

Capcom (TSE:9697)

Overview: Capcom is a Japanese video game producer best known for franchises like Resident Evil, Monster Hunter and Street Fighter, developing and selling home console and mobile games, running game arcades and amusement facilities, and licensing its characters worldwide.

Operations: Capcom generates most of its revenue from Digital Content at ¥144.3b, with additional contributions from Arcade Operations at ¥25.7b, Amusement Equipment at ¥17.8b, and Other businesses at ¥7.7b. Sales are spread across Japan (¥64.1b), the United States (¥53.2b), Europe (¥33.5b) and other regions (¥44.6b).

Market Cap: ¥1.37t

Capcom stands out in this screener because it combines globally recognised franchises and a proprietary game engine with fundamentals that many investors look for, including a 20.4% ROE, double digit historical and forecast earnings growth, and analyst expectations of upside from the current share price despite a relatively full P/E. At the same time, the heavy use of non cash earnings and a funding structure fully reliant on external borrowing add complexity to its quality profile, particularly after the stock lagged a strong Japanese market over the past year. Together with a pipeline of new titles and expansions tied to its major series, Capcom is a stock where the balance of growth potential and valuation risk may warrant close monitoring.

Capcom’s globally recognised franchises and 20.4% ROE set high expectations, but the real story sits in how future earnings are modelled and priced in the DCF valuation analysis for Capcom, especially where non cash items start to matter DCF valuation analysis for Capcom

Micronics Japan (TSE:6871)

Overview: Micronics Japan develops and sells test equipment for semiconductors and flat panel displays, including probe cards, wafer probers and related components that chipmakers and electronics manufacturers use to check whether their products work properly before shipping.

Market Cap: ¥617.5b

Micronics Japan is drawing attention because its core business in semiconductor testing is tied to chip demand, and recent guidance points to strong sales and profit expectations, underpinned by DRAM and probe card demand. Earnings growth of 60.4% in the past year and a net margin of around 19.2% suggest the current business model is working efficiently, while forecasts for earnings and revenue growth ahead of the wider Japanese market reinforce that impression. At the same time, a rich 41.8x P/E, a funding structure reliant on external borrowing and a highly volatile share price raise questions about how much optimism is already reflected in the stock. The key consideration for investors is whether the quality of earnings and governance justifies that premium.

Micronics Japan’s fast rising earnings and rich 41.8x P/E hint at a story that is not fully priced in yet, but the real twist sits in the analyst forecasts for Micronics Japan

Kasumigaseki CapitalLtd (TSE:3498)

Overview: Kasumigaseki CapitalLtd is a Tokyo based real estate consulting company that develops and operates solar power projects, logistics and warehousing facilities, apartment hotels under the fav, FAV LUX and seven x seven brands, and healthcare facilities alongside an overseas business.

Operations: Kasumigaseki CapitalLtd generates all of its ¥134,428m in revenue from Real Estate Consulting Business within Japan.

Market Cap: ¥169.6b

Kasumigaseki CapitalLtd is on many growth watchlists because analysts expect earnings to rise around 34.6% per year, building on 66.8% earnings growth in the last year and revenue projections well ahead of the broader Japanese market. Forecast ROE climbing toward 32.8% and an 8% net margin suggest the core real estate and infrastructure model could become more efficient. A P/E below some fair value estimates and analyst target prices above the current level indicate room for re rating if those forecasts are met. The flip side is that the company leans heavily on external funding, has seen shareholder dilution and is led by relatively new management, which makes the balance between growth potential and financial risk crucial to understand in detail.

Kasumigaseki CapitalLtd’s fast earnings projections and rising forecast ROE grab attention, but the real puzzle is whether that growth path is realistic or stretched. That is exactly what the analyst forecasts for Kasumigaseki CapitalLtd starts to unpack.

The three stocks covered here are just a starting sample, and the full Fast Growing Stocks With High Insider Ownership screener on Simply Wall St surfaces 91 more companies with equally compelling narratives through the Fast Growing Stocks With High Insider Ownership screener. Use the Simply Wall St tools to identify, analyze and filter for the specific catalysts and insider backed growth stories that matter most, so you can focus on your highest conviction ideas.

Take Control of Your Investment Journey

If Kasumigaseki CapitalLtd or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Momentum Flies Past?

Fresh stock ideas can move from quiet to full breakout quickly, and once the crowd catches on, the easy entry often drops away, so act now.

- Spot sturdy compounders early by scanning a curated list of solid balance sheet and fundamentals (37 results) that puts financial strength and durable fundamentals front and center before the crowd piles in.

- Ride structural demand shifts by reviewing a hand picked 35 power grid technology and infrastructure stocks built around companies positioned in critical energy and transmission infrastructure while it is still under the radar for now.

- Get ahead of capital rotations by checking a focused 29 best rare earth metal stocks featuring producers tied to materials that can become scarce just as global demand builds, so consider researching them early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com