EchoStar (ECHO) Stock Still May Be Below Fair Value On SpaceX Stake Buzz

EchoStar stock has delivered a very strong 378.5% return over the past three years, yet its valuation checks currently send mixed signals as the Discounted Cash Flow (DCF) intrinsic value estimate points to meaningful upside while market multiples lean the other way.

- Over three years, EchoStar has returned 378.5%. This makes the current pricing question more about how much of the story is already reflected in the share price.

- Recent analyst focus on the potential value of EchoStar's SpaceX stake and spectrum assets can support the bullish case. At the same time, insider share sales and debate over how to value those holdings may temper enthusiasm for paying a higher price.

- EchoStar scores 4 out of 6 on the valuation checks, which points to a mixed picture rather than a clear bargain or clear overvaluation.

The issue now is whether EchoStar's current share price already reflects the intrinsic value suggested by the Discounted Cash Flow (DCF) estimate or if there is still a reasonable margin between price and value.

Does EchoStar Look Undervalued on Cash Flow?

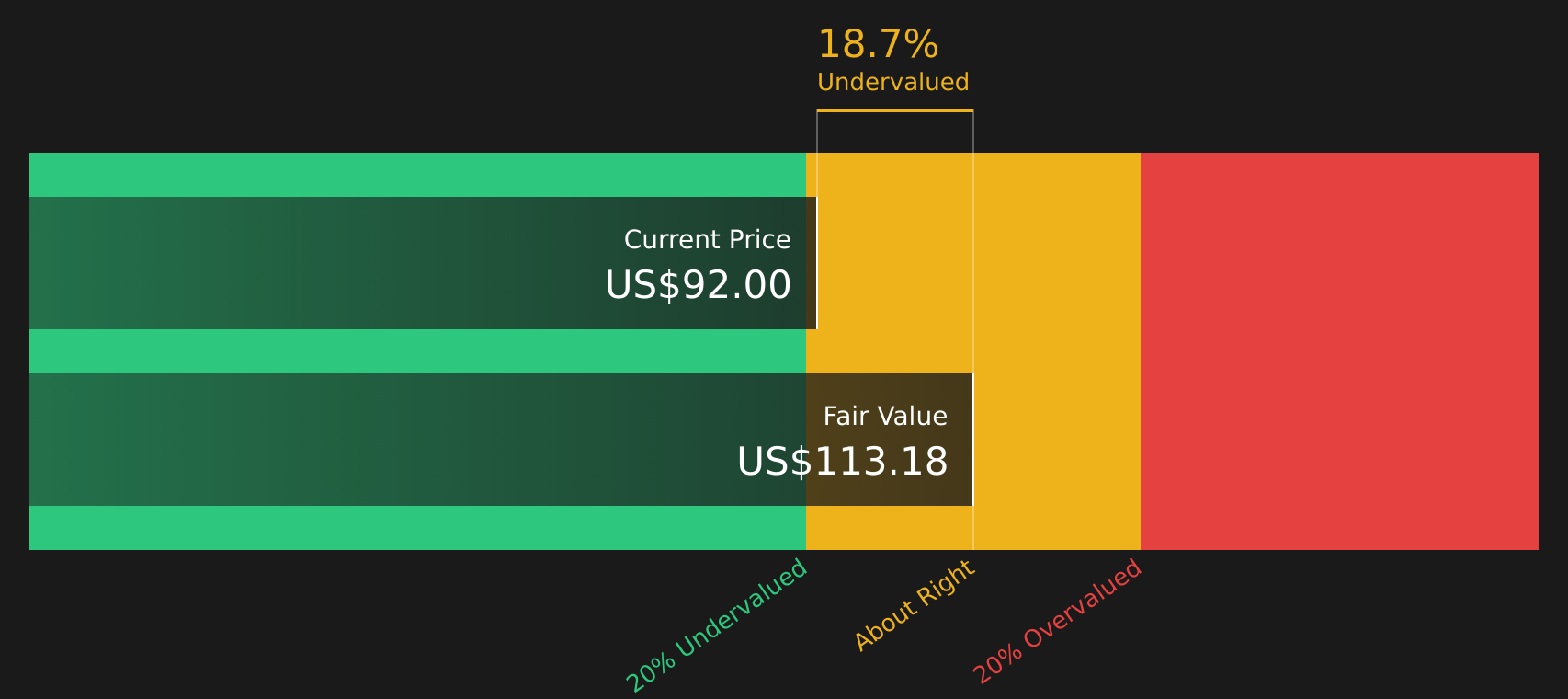

The Discounted Cash Flow (DCF) model here is built on EchoStar’s projected free cash flows to equity over two stages. EchoStar currently reports trailing twelve month free cash flow of a loss of $2.45b, yet the model assumes recovering cash generation in the coming years, leading to positive future free cash flows.

Based on those projections, the DCF points to an estimated intrinsic value of about $115 per share. Compared with the current market price, this implies the stock trades at roughly a 20.6% discount to that estimate. Deutsche Bank’s and Citi’s recent focus on the potential value of EchoStar’s SpaceX stake and spectrum assets helps explain why some investors may be comfortable looking past the current cash flow loss.

On this cash flow view, EchoStar stock appears undervalued relative to the intrinsic value implied by the DCF model.

Our Discounted Cash Flow (DCF) analysis suggests EchoStar is undervalued by 20.6%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

Is EchoStar Getting Expensive on Sales?

For EchoStar, the P/S multiple is a useful cross check because revenue is a cleaner starting point than current earnings or cash flow.

EchoStar trades on a P/S of about 1.8x, which is above the wider media industry average of around 0.9x and also higher than the peer group average of roughly 2.8x that is used in the model. The tailored fair P/S ratio for EchoStar is 1.2x, based on factors such as its margins, risk profile and size, which is meaningfully lower than where the stock is currently trading.

This gap suggests EchoStar is priced at a premium to what the model implies would be reasonable on today’s sales, even after accounting for its specific business mix and risks. Investors who are focusing on the value of assets like the SpaceX stake and spectrum may be willing to pay that premium, but on pure revenue multiples the shares already screen as relatively expensive.

On the P/S multiple, EchoStar stock currently screens as overvalued relative to the level the model flags as fair.

See what the numbers say about this price — find out in our valuation breakdown.

The EchoStar Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for EchoStar pick up where this valuation puzzle leaves off. They spell out what would need to happen to EchoStar's growth, margins and earnings for the stock to be worth significantly more or less than today's price, and they sit on the Community page. Rather than relying on a single multiple or model output, each narrative lays out the assumptions behind its fair value so you can compare them with the actual results as they are reported.

EchoStar community views are pulled wide apart, with one camp focused on upside from spectrum and satellite exposure while the other worries the stock already prices in too much hope.

Bull case: 33% undervalued

"Success in monetizing EchoStar's substantial spectrum assets, either through launching lucrative new services, entering wholesale partnerships with global carriers, or potential spectrum sales/leases, could unlock significant one-time gains or ongoing income..."

Read the full Bull Case to see why EchoStar could be undervalued

Bear case: 108% overvalued

"Let’s be real: if you just looked at EchoStar’s legacy financials, you’d run the other way..."

Read the full Bear Case to see why EchoStar could be overvalued

Do you think there's more to the story for EchoStar? Head over to our Community to see what others are saying!

The Bottom Line

EchoStar sits at an awkward but interesting point, with the Discounted Cash Flow (DCF) intrinsic value suggesting meaningful upside while current sales multiples lean towards overvalued. The split largely comes down to how you weigh future cash flow potential against what the market is already willing to pay for its revenue and assets today, after such a sharp share price move. With the broader valuation checks painting a mixed, rather than outright cheap, picture, the key question is whether EchoStar can turn its asset base and business model into the cash generation that the intrinsic value estimate assumes, or whether the market has already captured most of that optimism in the current price.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com