Is Alkane Resources (ASX:ALK) Undervalued Following High Grade Drilling And Strong Gold Production?

Alkane Resources (ASX:ALK) has drawn fresh attention after reporting high grade drilling intercepts at both the Björkdal Gold Mine in Sweden and the True Blue deposit in Australia, along with updated gold production and sales figures.

See our latest analysis for Alkane Resources.

Recent exploration and production updates have landed while Alkane Resources’ share price has eased, with a 30 day share price return of 11.75% and a 90 day share price return of 23.2%. However, the 1 year total shareholder return of 113.85% and 3 year total shareholder return of 72.67% show that longer term holders have still seen strong gains, suggesting momentum has cooled recently after a strong run.

If you are comparing Alkane’s drilling progress with other precious metals opportunities, this could be a useful moment to scan for leading peers using our curated list of 33 elite gold producer stocks

For Alkane Resources, there is now a clear tension: recent exploration and production news on one side, and a share price that has cooled over 30 days on the other. Do current valuation metrics still match that story?

Most Popular Narrative: 83.7% Undervalued

According to RockeTeller’s widely followed narrative on Alkane Resources, a fair value of A$8.54 per share sits well above the last close at A$1.39, setting up a wide valuation gap for investors to assess.

The strongest upside comes from four things: strong gold price leverage from current production, high-grade gold-antimony exposure at Costerfield, longer-life production from Björkdal and Tomingley, and the Boda-Kaiser gold-copper project, which could become the company’s major long-term growth engine.

Read the complete narrative. Read the complete narrative.

The narrative’s valuation hangs on Alkane Resources running a multi mine platform efficiently, keeping all in sustaining costs within guidance, and eventually bringing a large copper gold project into the mix without over stretching the balance sheet. The numbers behind those assumptions shape the A$8.54 fair value. The full narrative breaks down how those moving parts fit together.

Result: Fair Value of A$8.54 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Alkane Resources still faces execution and cost risks, with complex multi mine integration and Björkdal’s higher AISC. Both factors are capable of challenging this bullish narrative.

Find out about the key risks to this Alkane Resources narrative.

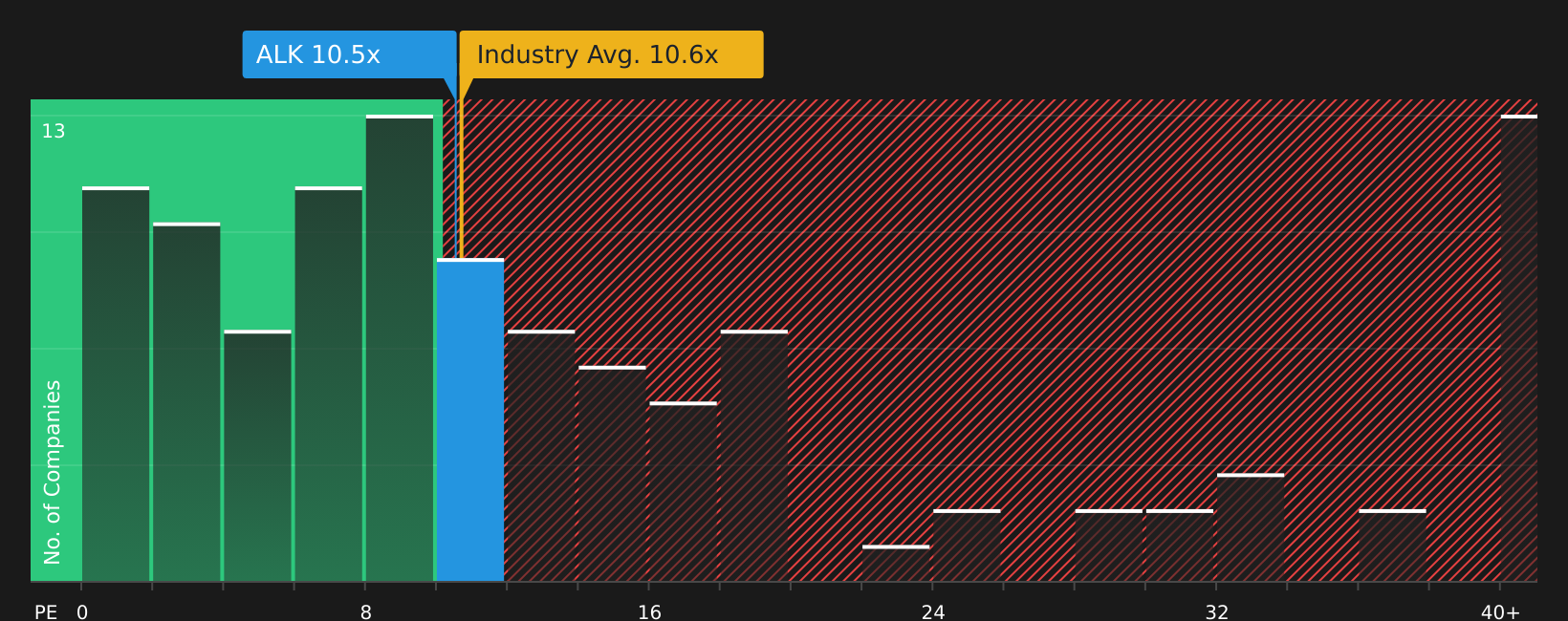

Another View: What Alkane Resources’ Earnings Multiple Is Telling You

The headline narrative around Alkane Resources hinges on a big gap between price and fair value, yet the earnings multiple sends a more cautious signal. At about 11.2x P/E, Alkane trades roughly in line with the Australian metals and mining industry at 11.2x, and above peer averages at 10.2x.

Our fair ratio of 21.7x suggests the market could eventually price Alkane closer to that higher earnings multiple, which would point to more upside. However, the current premium to peers also hints at less room for error if growth or costs disappoint. Is this a margin of safety or already a crowded trade for new buyers?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If the mixed signals around Alkane Resources leave you undecided, use the data to pressure test both the risks and the potential rewards. To see how those factors stack up side by side, review the 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond Alkane Resources?

If Alkane Resources has sharpened your focus, do not stop here. Broaden your watchlist now so you do not miss other compelling setups across the market.

- Target potential mispricings by scanning 8 high quality undervalued stocks, which pair solid fundamentals with prices that may not fully reflect their financial profiles.

- Strengthen your income focus by reviewing 6 dividend fortresses, which combine higher yields with balance sheets you can scrutinise in one place.

- Tilt toward resilience by checking 8 resilient stocks with low risk scores, which score well on financial strength and lower historical risk signals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com