Reddit (RDDT) Stock Looks Rich Despite Its 30% One Year Gain

Reddit stock has delivered a 30.0% return over the past year, yet its valuation signals are pulling in different directions, with a Discounted Cash Flow (DCF) estimate pointing to substantial upside while market multiples paint a richer picture.

- Over the last 12 months, Reddit has returned 30.0%, which puts more pressure on today’s price to be supported by future cash flows rather than past gains.

- Expectations around Reddit’s ability to grow advertising and data licensing revenue tied to AI can support the intrinsic value case, while regulatory moves such as a potential under 16 social media ban in the UK may cap how much investors are willing to pay for that growth.

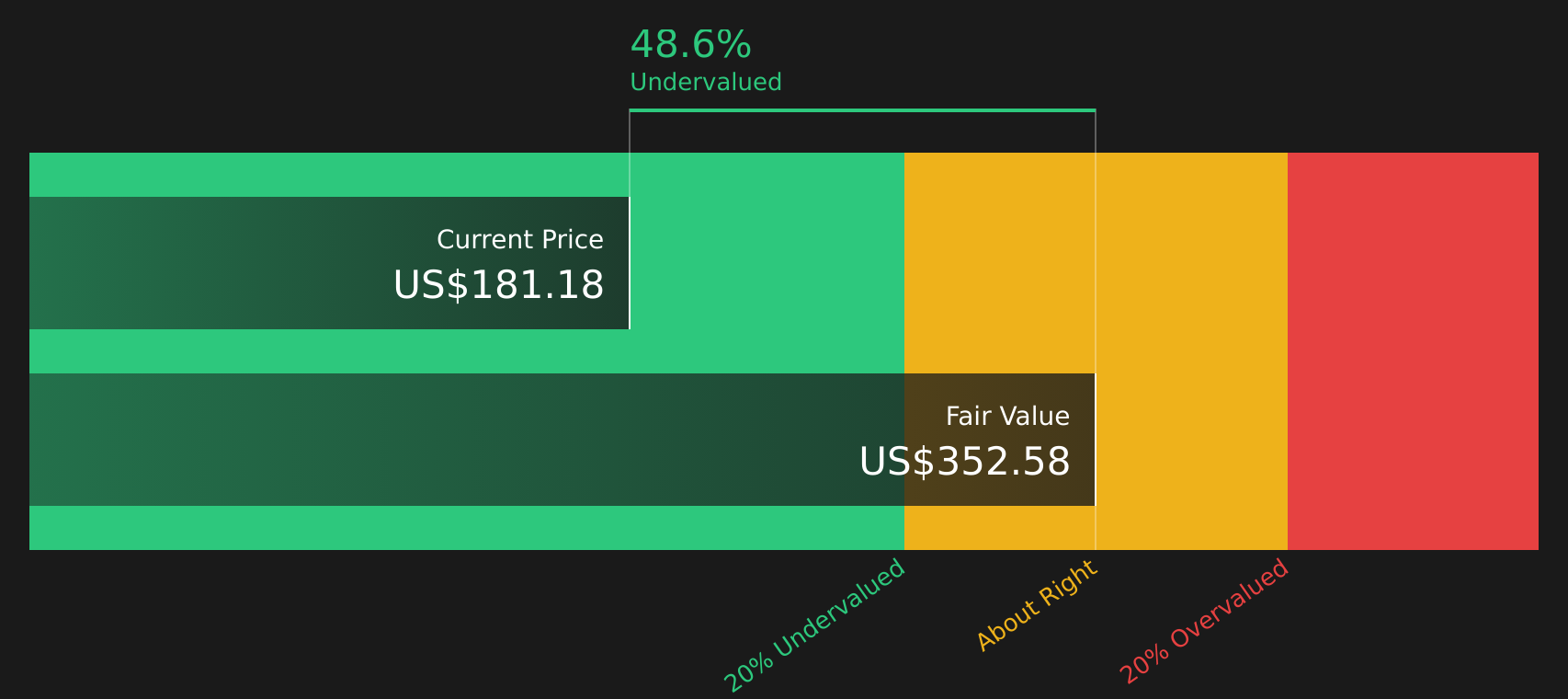

- On Simply Wall St’s broader valuation checks, Reddit only passes 2 out of 6. This leans closer to “not a clear bargain” territory even though the DCF implies the stock trades at roughly a 47.4% discount to intrinsic value.

The issue now is whether Reddit’s current share price is closer to the richer view implied by market multiples or the discount suggested by the intrinsic value estimate.

Find out why Reddit's 30.0% return over the last year is lagging behind its peers.

Is Reddit a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) approach estimates what Reddit might be worth today based on projected future cash flows. For Reddit, the model starts with latest twelve month free cash flow of about $864 million, then assumes those cash flows keep growing rather than shrinking, in line with the two stage free cash flow to equity setup.

On those inputs, the DCF points to an estimated intrinsic value of about $352 per share, which implies the stock is roughly 47.4% undervalued relative to the current price. Because Wedbush recently highlighted Reddit’s potential in AI driven advertising and data licensing, the market moves around those themes help explain why sentiment is strong even though the DCF still sits well above where the shares trade today.

On balance, the DCF workup suggests Reddit stock currently screens as undervalued against its modeled cash flows.

Our Discounted Cash Flow (DCF) analysis suggests Reddit is undervalued by 47.4%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

Does Reddit Look Pricey on Earnings?

The P/E ratio is a common way to compare Reddit’s share price with its earnings power. Reddit currently trades on about 50.4x earnings, compared with an Interactive Media and Services industry average of roughly 15.7x and a broader peer group around 31.0x, so the stock sits well above both benchmarks.

The tailored fair P/E ratio for Reddit is about 32.6x, which already factors in its profile on growth, margins, size and risks. The actual multiple still stands meaningfully higher. That gap suggests the market is paying a premium for Reddit’s earnings that exceeds what this framework would imply as reasonable.

On this P/E yardstick, Reddit stock currently screens as overvalued relative to both its sector and the fair multiple estimate.

See what the numbers say about this price — find out in our valuation breakdown.

The Reddit Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where Reddit's valuation gap leaves off by spelling out which specific assumptions on growth, margins and earnings would need to hold for the stock to be worth materially more or less than today’s price on the Community page. Each narrative ties its number to a clear view of how Reddit's growth profile, profitability and risk might evolve, giving you a reference point you can revisit as fresh information comes through.

Community narratives on Reddit stock are divided, with one leaning into user momentum and AI data, and the other focused on regulatory and engagement risks.

Bull case: 40% undervalued

"RDDT currently represents a large undervalued segment because its DAU user growth is still being undervalued…"

Read the full Bull Case to see why Reddit could be undervalued

Bear case: 25% overvalued

"Reddit's heavy reliance on user-generated content exposes it to intensifying regulatory scrutiny around data privacy and content moderation worldwide, forcing increased compliance costs and restriction of data monetization as governments introduce stricter rules, resulting in lower net margins and higher operating expenses over the long term…"

Read the full Bear Case to see why Reddit could be overvalued

Do you think there's more to the story for Reddit? Head over to our Community to see what others are saying!

The Bottom Line

For Reddit, the Discounted Cash Flow (DCF) work suggests meaningful upside based on modeled cash flows, while the P/E and other market multiples argue the stock already carries a rich valuation. That split comes down to which lens you trust more: intrinsic value grounded in long term cash generation, or market pricing that leans heavily on growth expectations and sentiment. Given the weaker broader valuation checks, the key question is whether Reddit can translate its advertising and AI related data ambitions into durable, profitable cash flows, or whether current enthusiasm and regulatory risks mean the apparent discount is closer to a value trap than a clear opportunity.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com