Do Lower 2026 Earnings Estimates Quietly Challenge Dow’s (DOW) Operational Turnaround Narrative?

- Dow Inc. recently saw analysts revise their consensus earnings forecast lower for the June 2026 quarter, even as expectations still point to higher revenue and earnings compared with the same period a year earlier.

- This combination of anticipated year-over-year improvement and a more cautious earnings outlook highlights growing uncertainty around how much operational progress will actually show up in Dow’s upcoming results.

- We’ll now explore how this more cautious analyst stance ahead of earnings could influence Dow’s existing investment narrative and key assumptions.

Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

Dow Investment Narrative Recap

To own Dow today, you have to believe its cost cuts, asset reviews and capital discipline can eventually turn persistent losses into sustainable profitability, without eroding its core plastics and chemicals franchise. The recent cut to June 2026 consensus EPS, despite higher year over year earnings and revenue still being expected, mainly reinforces near term uncertainty around that profit recovery rather than changing the central catalyst or the key risk of ongoing margin pressure and weak demand.

The most relevant recent development is the 50% dividend cut to US$0.35 per share in 2026, following years of higher payouts. In the context of analysts trimming near term earnings expectations, that lower dividend underscores how dependent Dow’s story is on freeing up cash through cost reductions, asset sales and delayed Path2Zero spending, while also reminding shareholders that pressure on cash flow remains an active risk rather than a past issue.

Yet this more cautious tone could matter most for investors who may be underestimating how prolonged margin pressure from higher input costs and uneven demand might become...

Read the full narrative on Dow (it's free!)

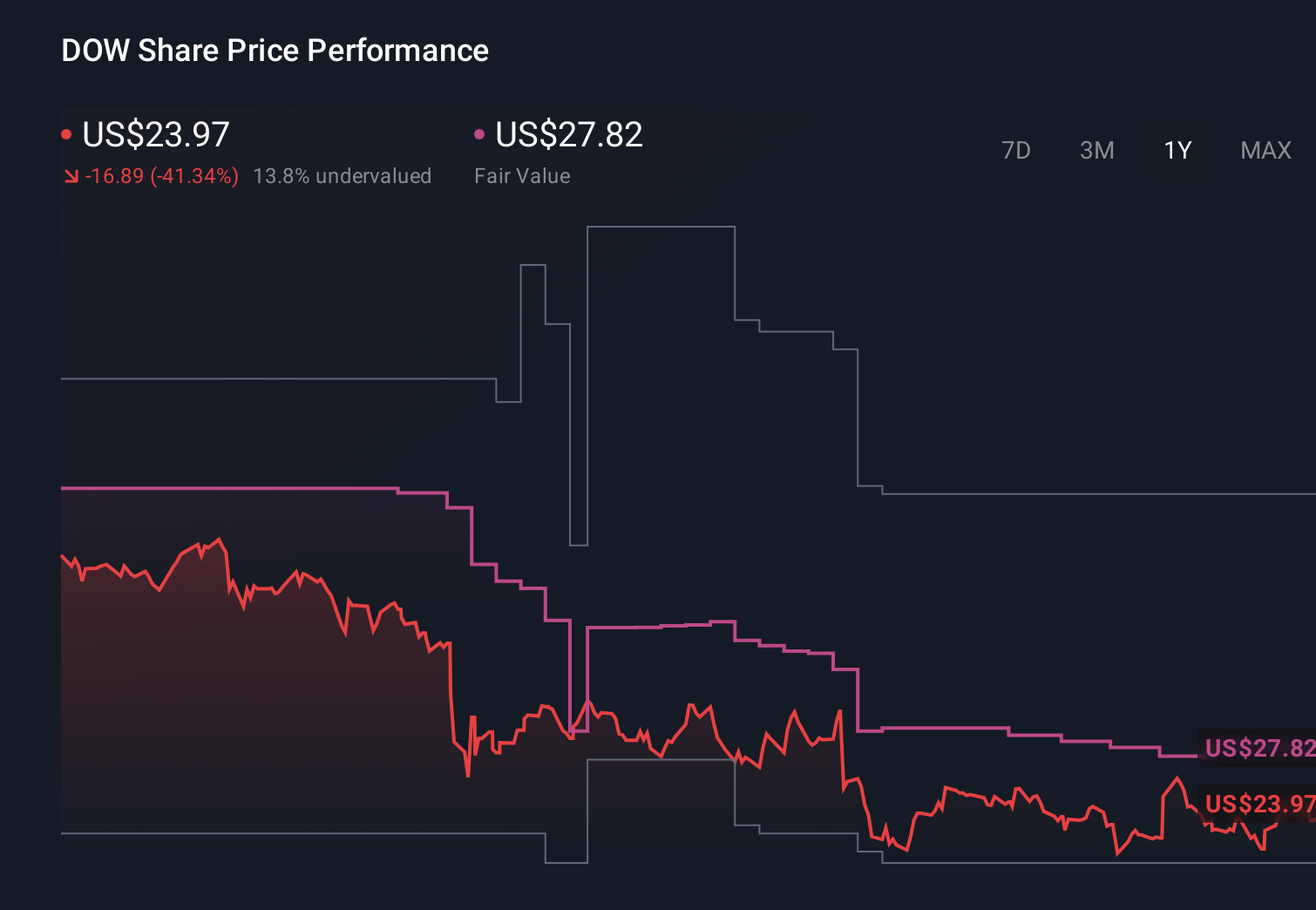

Dow's narrative projects $45.0 billion revenue and $1.6 billion earnings by 2029. This requires 4.6% yearly revenue growth and a $4.5 billion earnings increase from -$2.9 billion today.

Uncover how Dow's forecasts yield a $42.62 fair value, a 45% upside to its current price.

Exploring Other Perspectives

Before this EPS downgrade, the most optimistic analysts were projecting Dow’s earnings to swing from about negative US$2.9 billion to roughly US$2.0 billion, yet these upbeat views sit in sharp contrast with the risk that prolonged structural oversupply could keep compressing prices and margins.

Explore 5 other fair value estimates on Dow - why the stock might be worth as much as 64% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Dow research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Dow research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Dow's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com