Marathon Petroleum (MPC) Stock Could Be 17% Undervalued As Earnings Near

Marathon Petroleum stock has delivered a very large 5 year return while its valuation checks are pulling in different directions, with a Discounted Cash Flow (DCF) estimate pointing to upside and market multiples suggesting the shares are priced richly.

- Over 5 years, Marathon Petroleum has returned about 5.5x an initial investment, which puts extra focus on whether the current share price already reflects the good news.

- Upcoming earnings expectations and the company’s scale as a leading U.S. refiner can support the intrinsic value case, while operational, regulatory and geopolitical risks around its refining and logistics footprint may limit how much investors are willing to pay.

- On Simply Wall St’s checks, Marathon Petroleum screens as undervalued in only 1 of 6 areas, which leans more toward “not a clear bargain” once the broader valuation picture is considered.

The issue now is whether the DCF based intrinsic value or the richer earnings multiple view is the better guide to where Marathon Petroleum stock should trade from here.

Is Marathon Petroleum a Bargain on Cash Flow?

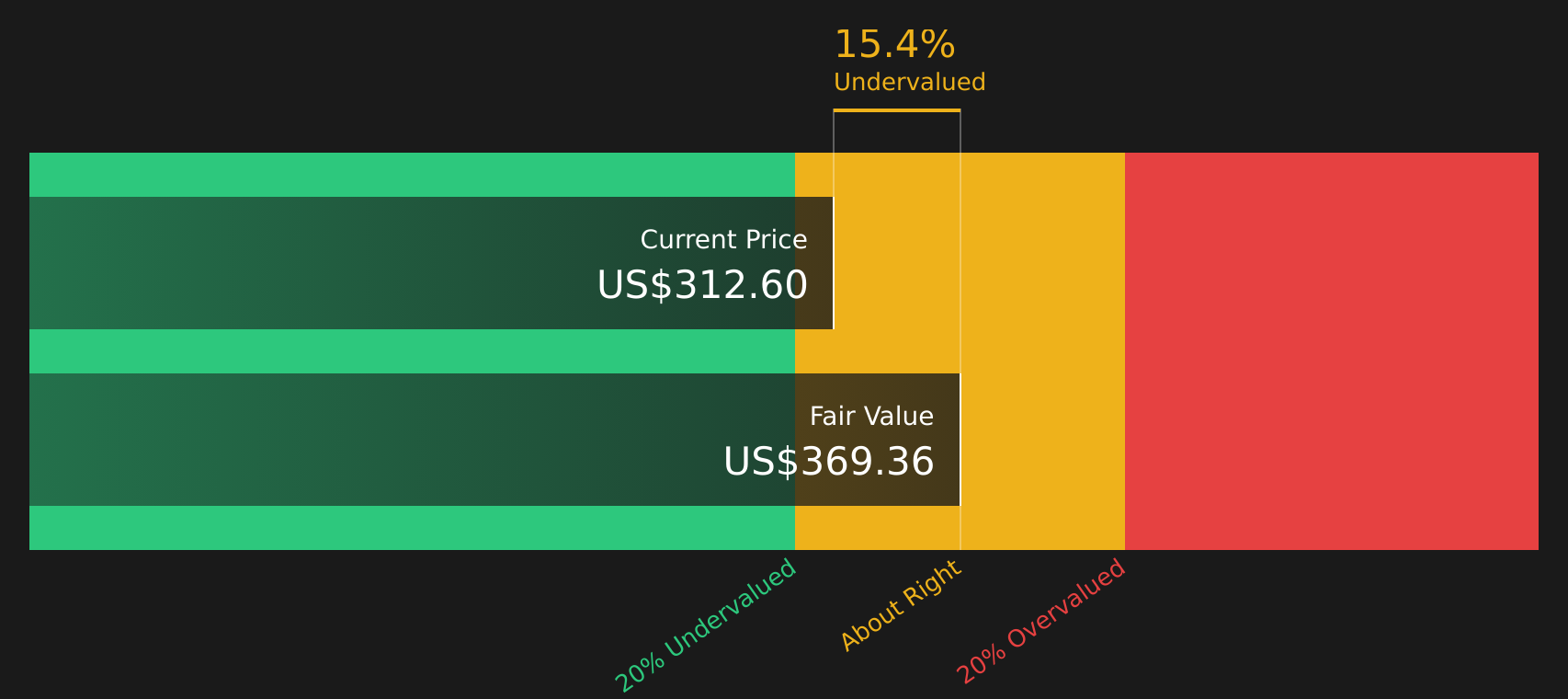

The Discounted Cash Flow (DCF) approach estimates what Marathon Petroleum is worth based on the cash it can generate for shareholders. On this model, the company’s latest twelve month free cash flow is about $6.7b, and the projections assume cash flows that generally settle into a declining pattern over time rather than aggressive growth.

Those cash flows translate into an estimated intrinsic value of about $369 per share, which implies the stock screens roughly 17.2% undervalued against the current market price. The upcoming Q2 earnings release, with expectations for higher EPS, may help explain why some investors are already pricing in strong performance. At the same time, the cash flow based value still sits higher than where Marathon Petroleum currently trades.

Overall, the Discounted Cash Flow workup suggests Marathon Petroleum stock appears undervalued relative to the cash it is expected to generate.

Our Discounted Cash Flow (DCF) analysis suggests Marathon Petroleum is undervalued by 17.2%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

Is Marathon Petroleum Getting Expensive on Earnings?

The P/E ratio is a useful cross check for Marathon Petroleum because earnings are a key driver for a mature refiner and logistics operator. The stock currently trades at about 19.3x earnings, which is higher than the Oil and Gas industry average of roughly 13.6x and also above the peer group average of about 18.0x.

On Simply Wall St’s model, a P/E of about 17.2x would be more in line with what you might expect for Marathon Petroleum once its growth profile, margins, size and risk factors are blended together. The current P/E sits above that fair ratio, which indicates that the shares are priced richer than the framework suggests is warranted on earnings alone.

On this P/E comparison, Marathon Petroleum stock appears overvalued relative to what its earnings profile would typically justify.

See what the numbers say about this price — find out in our valuation breakdown.

The Marathon Petroleum Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Marathon Petroleum pick up where this valuation puzzle leaves off by spelling out which assumptions on growth, margins and earnings would need to hold for Marathon Petroleum's stock to be worth materially more or less than today's price, and they sit on the company’s Community page. Each Narrative treats its fair value as a thesis you can track over time, so you can see how the underlying business case holds up as new information arrives.

Community views on Marathon Petroleum sit far apart, with one group leaning into the long build out story and another questioning how durable current conditions really are.

Bull case: roughly fairly valued

"Refining investments at Galveston Bay, Garyville, Robinson and El Paso are aimed at converting lower value inputs into higher value products and improving reliability…"

Read the full Bull Case to see why Marathon Petroleum could be undervalued

Bear case: 53% overvalued

"Refining investments at Garyville, Galveston Bay, Robinson and El Paso are heavily geared toward higher utilization and margin capture in a tight global refining system…"

Read the full Bear Case to see why Marathon Petroleum could be overvalued

Do you think there's more to the story for Marathon Petroleum? Head over to our Community to see what others are saying!

The Bottom Line

For Marathon Petroleum, the Discounted Cash Flow (DCF) workup points to intrinsic value above the current share price, while the P/E based view flags the stock as overvalued relative to its earnings profile. The broader valuation checks remain weak despite that single DCF signal, and the sharp move in the share price makes the earnings multiple easier to stretch than to defend. The gap between cash flow and multiples comes down to how much weight you put on long term cash generation versus today’s expectations and sentiment. The key question from here is whether current refining margins and utilization can be sustained without a material reset.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com