Danieli & C. Officine Meccaniche (BIT:DAN) Wins A Steel Plant Contract, Is The Stock Fairly Valued?

Henan Jiyuan Iron and Steel’s decision to award Danieli & C. Officine Meccaniche (BIT:DAN) a contract for a jumbo round continuous casting machine puts the company’s steel plant equipment capabilities in focus for investors.

See our latest analysis for Danieli & C. Officine Meccaniche.

Against this contract win, Danieli & C. Officine Meccaniche’s share price is €69.0, with the stock down 7.63% on a 1 month share price basis but still up 33.72% year to date. The 1 year total shareholder return of 98.77% and 3 year total shareholder return of 234.15% point to strong longer term momentum.

If this kind of industrial order story interests you, it could be worth widening your search beyond a single stock using the 33 robotics and automation stocks

After Danieli & C. Officine Meccaniche’s sharp run and the recent pullback, it is fair to ask whether most of the rerating is already in the price or if the latest contract win still leaves meaningful upside ahead as valuation comes into focus.

Price-to-Earnings of 21.9x: Is it justified?

On a P/E of 21.9x, Danieli & C. Officine Meccaniche looks slightly expensive against parts of its machinery peer group, even after the recent share price pullback to €69.0.

The P/E ratio compares the current share price with earnings per share. For a company like Danieli & C. Officine Meccaniche, it effectively reflects what investors are willing to pay today for each euro of current earnings in its plant making and steel making operations.

According to the statements, Danieli & C. Officine Meccaniche is considered good value versus an estimated fair P/E of 23x. This suggests there may be some room for the valuation multiple to align more closely with that reference level over time. At the same time, the stock is described as expensive versus the wider European machinery industry average P/E of 21.2x, yet still below a peer group average of 26.6x. This highlights how the market is pricing its earnings at a premium to the sector average but at a discount to closer peers.

Explore the SWS fair ratio for Danieli & C. Officine Meccaniche.

Result: Price-to-Earnings of 21.9x (ABOUT RIGHT)

However, Danieli & C. Officine Meccaniche still faces risks if large plant orders slow or if machinery peers see valuation multiples compress further.

Find out about the key risks to this Danieli & C. Officine Meccaniche narrative.

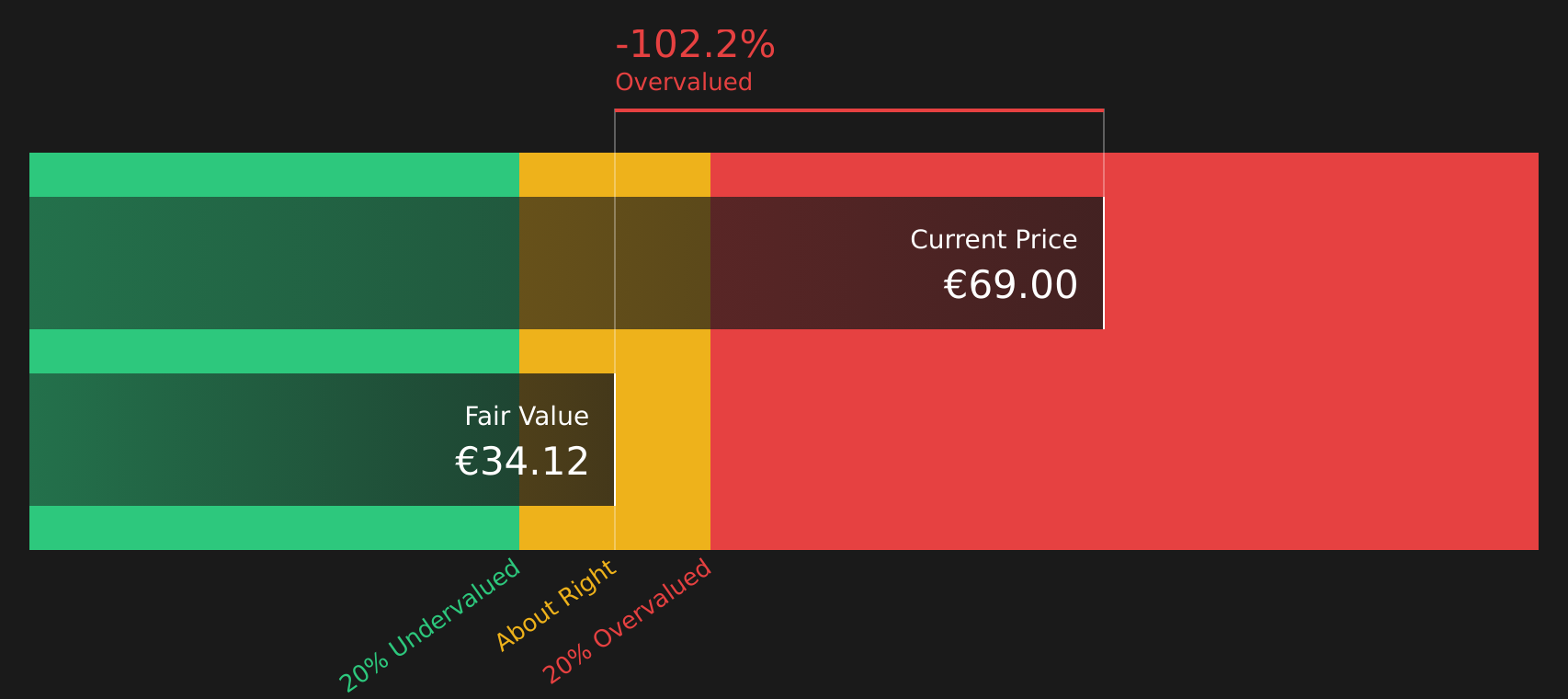

Another View: SWS DCF model paints a different picture

While the 21.9x P/E for Danieli & C. Officine Meccaniche looks roughly in line with its fair ratio of 23x, the SWS DCF model points in a very different direction. At a share price of €69, Danieli & C. Officine Meccaniche is trading well above an estimated future cash flow value of €34.11. This frames the recent rally as carrying clear valuation risk rather than obvious upside.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Danieli & C. Officine Meccaniche for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 221 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly mixed around Danieli & C. Officine Meccaniche’s valuation, it makes sense to move quickly, review the underlying data, and form your own view while also weighing the 1 key reward

Looking for more investment ideas beyond Danieli & C. Officine Meccaniche?

If Danieli & C. Officine Meccaniche has your attention, do not stop here. The right screener can surface stocks you would probably never spot on your own.

- Target potential mispricings by scanning a focused set of 221 high quality undervalued stocks that combine fair prices with compelling fundamentals.

- Strengthen your defensive side by reviewing 294 resilient stocks with low risk scores that score well on resilience, so sudden shocks are less likely to catch you off guard.

- Spot fresh opportunities early by checking a screener containing 506 high quality undiscovered gems that the market may not be paying close attention to yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com