Williams-Sonoma (WSM) Following Pink Palm Puff Launch Looks Fully Valued Against Fair Value

Williams-Sonoma (WSM) is drawing fresh attention after Pottery Barn Teen unveiled a collaboration with Pink Palm Puff, introducing coastal and surf inspired designs across teen rooms and back to school essentials.

See our latest analysis for Williams-Sonoma.

That launch comes as Williams-Sonoma shares trade at US$222.84, with a 90-day share price return of 16.37% and a year-to-date share price return of 18.63%. The 1-year total shareholder return sits at 37.02%, and the 3-year total shareholder return is more than 3x, which points to strong momentum despite short term noise such as recent insider selling and mixed valuation signals from different models.

If this kind of design led growth story interests you, it could be a good moment to broaden your watchlist and check out the 18 top founder-led companies.

Williams-Sonoma now trades slightly above the average analyst price target, yet sits at a discount to one cash-flow-based fair value estimate. Is the market being cautious for good reason, or overly restrained after this latest move?

Most Popular Narrative: 4.8% Overvalued

On the most followed narrative, Williams-Sonoma's fair value of $212.63 sits a little below the recent $222.84 close, which places more weight on long term earnings power than on short term price swings.

Continued investment and advances in AI powered tools and digital platforms are driving higher conversion rates, improved customer experience, and measurable productivity gains, supporting both revenue growth and expanded operating leverage at the margin level.

Read the complete narrative. Read the complete narrative.

Want to see what is baked into that fair value for Williams-Sonoma? The narrative leans heavily on steady top line growth, firm margins, and a richer earnings multiple. Curious which assumptions really move the valuation needle and how sensitive the outcome is to even small changes? The full breakdown lays out those building blocks in detail.

Result: Fair Value of $212.63 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Williams-Sonoma still faces real pressure from tariff volatility and a softer housing backdrop, both of which could challenge margins and demand assumptions that underpin this narrative.

Find out about the key risks to this Williams-Sonoma narrative.

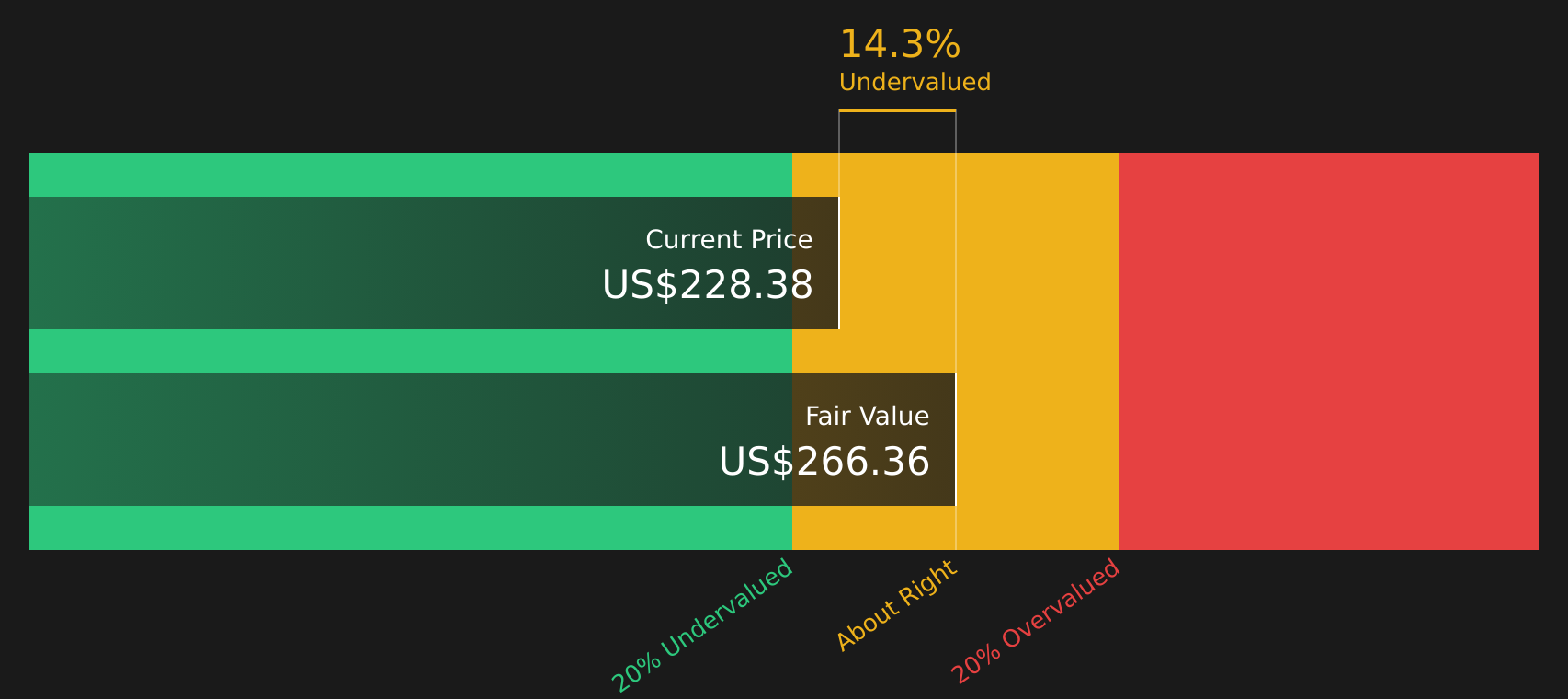

Another View: Williams-Sonoma Through a Cash Flow Lens

The earlier analyst narrative framed Williams-Sonoma as about 4.8% overvalued relative to a $212.63 fair value based on earnings expectations and multiples. Our DCF model points in the opposite direction, with a fair value of $266.34, which is 16.3% above the current $222.84 share price.

That gap highlights how different methods can send very different signals, especially when long term cash flows, discount rates, and margin paths are in focus. For your own work, the key question is which set of assumptions around earnings quality and durability feels more realistic for Williams-Sonoma.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Williams-Sonoma for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mixed signals around Williams-Sonoma, do you see a compelling opportunity or a stretched story at current levels? Act quickly by reviewing the details that support investor optimism, then weigh those positives yourself with the 3 key rewards

Looking for more investment ideas beyond Williams-Sonoma?

Before you move on, use this momentum to scan for fresh stock ideas that match your goals, so you do not miss opportunities beyond Williams-Sonoma.

- Target stronger upside potential by reviewing companies our system flags as attractively priced with solid fundamentals through the 47 high quality undervalued stocks.

- Prioritize steadier portfolios by focusing on companies that show resilient risk profiles using the 78 resilient stocks with low risk scores.

- Hunt for future standouts by checking the screener containing 20 high quality undiscovered gems before other investors catch on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com